S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

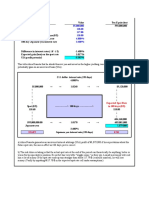

- Sunset Boards Case StudyDocument3 paginiSunset Boards Case StudyMeredith Wilkinson Ramirez100% (2)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- 2 - Ch12 CrustalDeformation Lab Responses 1 PDFDocument9 pagini2 - Ch12 CrustalDeformation Lab Responses 1 PDFShrey Mangal0% (10)

- 1Document2 pagini1Shrey Mangal0% (1)

- LIQUIDITYDocument1 paginăLIQUIDITYShrey MangalÎncă nu există evaluări

- Enterprise Zones 2Document2 paginiEnterprise Zones 2Shrey MangalÎncă nu există evaluări

- UuDocument1 paginăUuShrey MangalÎncă nu există evaluări

- Standard DistributionDocument1 paginăStandard DistributionShrey MangalÎncă nu există evaluări

- EquationDocument1 paginăEquationShrey MangalÎncă nu există evaluări

- 14Document3 pagini14Shrey MangalÎncă nu există evaluări

- AkiraDocument1 paginăAkiraShrey MangalÎncă nu există evaluări

- GroupXX Assign4Document5 paginiGroupXX Assign4Shrey MangalÎncă nu există evaluări

- Office Building, or A Warehouse. The Future States of Nature That Will Determine The Profits Payoff Table For This Decision Problem Is Given BelowDocument1 paginăOffice Building, or A Warehouse. The Future States of Nature That Will Determine The Profits Payoff Table For This Decision Problem Is Given BelowShrey MangalÎncă nu există evaluări

- HarkerDocument4 paginiHarkerShrey MangalÎncă nu există evaluări

- ANOVA results disagree with Nashville data due to small sample sizeDocument1 paginăANOVA results disagree with Nashville data due to small sample sizeShrey MangalÎncă nu există evaluări

- 5 45Document2 pagini5 45Shrey MangalÎncă nu există evaluări

- Proble M Number Solution: Answer SheetDocument11 paginiProble M Number Solution: Answer SheetShrey MangalÎncă nu există evaluări

- Chose the right answer multiple choicesDocument7 paginiChose the right answer multiple choicesShrey MangalÎncă nu există evaluări

- コピーC14 01Document3 paginiコピーC14 01Shrey MangalÎncă nu există evaluări

- Oral authorization is undocumentedDocument4 paginiOral authorization is undocumentedShrey Mangal0% (1)

- CHP 9 Case F16Document6 paginiCHP 9 Case F16Shrey MangalÎncă nu există evaluări

- Budget Variance WorksheetDocument4 paginiBudget Variance WorksheetShrey MangalÎncă nu există evaluări

- Bsbsus501a As 1Document12 paginiBsbsus501a As 1Shrey Mangal29% (7)

- Show All Work To Receive Credit On Each Problem. If No Work Is Provided, No Credit Can Be Given. Label The AnswersDocument3 paginiShow All Work To Receive Credit On Each Problem. If No Work Is Provided, No Credit Can Be Given. Label The AnswersShrey MangalÎncă nu există evaluări

- CH 13 ProbsDocument8 paginiCH 13 ProbsShrey MangalÎncă nu există evaluări

- HomeworkDocument6 paginiHomeworkShrey MangalÎncă nu există evaluări

- 1Document2 pagini1Shrey MangalÎncă nu există evaluări

- Quiz 6Document3 paginiQuiz 6Shrey MangalÎncă nu există evaluări

- Statistics QuestionDocument1 paginăStatistics QuestionShrey MangalÎncă nu există evaluări

- M1Document2 paginiM1Shrey MangalÎncă nu există evaluări

- 1Document5 pagini1Shrey MangalÎncă nu există evaluări