S-ar putea să vă placă și

- Value Chain Management Capability A Complete Guide - 2020 EditionDe la EverandValue Chain Management Capability A Complete Guide - 2020 EditionÎncă nu există evaluări

- Time Value of Money: Family Economics & Financial EducationDocument32 paginiTime Value of Money: Family Economics & Financial EducationBhagirath AshiyaÎncă nu există evaluări

- JHS SHS: Laguna College of Business and ArtsDocument47 paginiJHS SHS: Laguna College of Business and ArtsCatalina G. SerapionÎncă nu există evaluări

- Marketing Principles and StrategiesDocument17 paginiMarketing Principles and StrategiesMagdalena OrdoñezÎncă nu există evaluări

- Business FinanceDocument18 paginiBusiness FinanceFriedrich Mariveles100% (1)

- (#2) Supply-Demand and Philippine Economic ProblemsDocument16 pagini(#2) Supply-Demand and Philippine Economic ProblemsBianca Jane GaayonÎncă nu există evaluări

- Entrepreneurial Management Module New6 2Document6 paginiEntrepreneurial Management Module New6 2Class LectureÎncă nu există evaluări

- Business MathematicsDocument2 paginiBusiness MathematicsLuz Gracia OyaoÎncă nu există evaluări

- LP1 - Business SimulationDocument3 paginiLP1 - Business SimulationBryan Esguerra100% (1)

- Principles of Marketing ABM Chapter 4Document45 paginiPrinciples of Marketing ABM Chapter 4Ariel TorialesÎncă nu există evaluări

- Road To The Right Choice: Department of Education 1Document48 paginiRoad To The Right Choice: Department of Education 1Antonia GuiribaÎncă nu există evaluări

- (Applied Economics) Interactive Module Week 2Document7 pagini(Applied Economics) Interactive Module Week 2Billy Joe0% (1)

- Environmental AnalysisDocument15 paginiEnvironmental AnalysisJuncar TomeÎncă nu există evaluări

- Lesson Plan 1 - Household AccountsDocument5 paginiLesson Plan 1 - Household Accountsapi-252884016Încă nu există evaluări

- K To 12 CG - Nail Care - v1.0Document5 paginiK To 12 CG - Nail Care - v1.0Levi Lico PangilinanÎncă nu există evaluări

- Lagro High School: Schools Division Office Senior High School 5 District, Quezon CityDocument5 paginiLagro High School: Schools Division Office Senior High School 5 District, Quezon CitySteve bitoon delosreyesÎncă nu există evaluări

- Unit 1 The Capitalist Revolution 1.0Document33 paginiUnit 1 The Capitalist Revolution 1.0knowme73Încă nu există evaluări

- MODULE 1 Business FinanceDocument13 paginiMODULE 1 Business FinanceWinshei CaguladaÎncă nu există evaluări

- Chapter - 1-Introduction To Accounting and BusinessDocument49 paginiChapter - 1-Introduction To Accounting and BusinessAsaye TesfaÎncă nu există evaluări

- Objectives: A. Identify The Reasons For Keeping Business Records and B. Perform Key Bookkeeping TaskDocument11 paginiObjectives: A. Identify The Reasons For Keeping Business Records and B. Perform Key Bookkeeping TaskMarife CulabaÎncă nu există evaluări

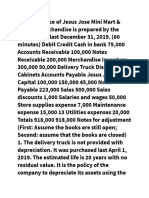

- E Trial Balance of Jesus Jose Mini MartDocument3 paginiE Trial Balance of Jesus Jose Mini Martshamsa ynnaÎncă nu există evaluări

- Business Finance For Video Module 2Document16 paginiBusiness Finance For Video Module 2Bai NiloÎncă nu există evaluări

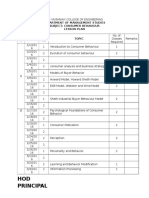

- Lesson Plan Consumer BehaviourDocument5 paginiLesson Plan Consumer BehaviourPrabhakar RaoÎncă nu există evaluări

- Contemporary Economic IssuesDocument4 paginiContemporary Economic IssuesJessa Mae AlgarmeÎncă nu există evaluări

- Applied Economics NotesDocument5 paginiApplied Economics NotesKhixel Jane PabroÎncă nu există evaluări

- Chapter 2 - Review of FSDocument32 paginiChapter 2 - Review of FSCrischelle PascuaÎncă nu există evaluări

- Liquidity RatiosDocument7 paginiLiquidity RatiosChirrelyn Necesario SunioÎncă nu există evaluări

- A e - Q2-M2Document21 paginiA e - Q2-M2Vince Nylser BorbonÎncă nu există evaluări

- Entrepreneurship IntroductionDocument12 paginiEntrepreneurship IntroductionMimi Adriatico JaranillaÎncă nu există evaluări

- ENTREPmoduleDocument6 paginiENTREPmoduleElla MaxineÎncă nu există evaluări

- Handouts Acctg 1Document14 paginiHandouts Acctg 1technician laoÎncă nu există evaluări

- Business Finance Week 1-2Document15 paginiBusiness Finance Week 1-2Emariel CuarioÎncă nu există evaluări

- Notes Ni HazelDocument38 paginiNotes Ni HazelJulia GorgonioÎncă nu există evaluări

- Accounting Equation Worksheet StudentDocument2 paginiAccounting Equation Worksheet StudentAlexis CarranzaÎncă nu există evaluări

- Module 1 Week 12 Business FinanceDocument12 paginiModule 1 Week 12 Business FinanceRocelyn ManatadÎncă nu există evaluări

- Economics Definition For A Progressive PhilippinesDocument19 paginiEconomics Definition For A Progressive PhilippinesJeff RamosÎncă nu există evaluări

- Bookkeeping NC III Accounting Recording Process: JournalizingDocument3 paginiBookkeeping NC III Accounting Recording Process: JournalizingLav Casal CorpuzÎncă nu există evaluări

- BSBA New Books 2018Document11 paginiBSBA New Books 2018xxxx0% (1)

- MAN385.23 - Entrepreneurial Management - Graebner - 04470Document15 paginiMAN385.23 - Entrepreneurial Management - Graebner - 04470Dimitra TaslimÎncă nu există evaluări

- Ae11 Module-Managerial EconomicsDocument65 paginiAe11 Module-Managerial EconomicsJynilou Pinote100% (1)

- Use Appropriate Analysis Framework and Methodology in (ABM - BES12-Ia-c-2)Document8 paginiUse Appropriate Analysis Framework and Methodology in (ABM - BES12-Ia-c-2)Aimee Lasaca100% (1)

- Business Finance Introduction To Financial Management 05Document24 paginiBusiness Finance Introduction To Financial Management 05Melvin J. ReyesÎncă nu există evaluări

- SECTION - GROUP No. - BUSINESS NAME - Business Plan Presentation RubricDocument2 paginiSECTION - GROUP No. - BUSINESS NAME - Business Plan Presentation RubricAllen GonzagaÎncă nu există evaluări

- CH 3 Demand, Supply and Market EquilibriumDocument45 paginiCH 3 Demand, Supply and Market EquilibriumBhargav D.S.Încă nu există evaluări

- Chapter 6 Introduction To InvestmentsDocument25 paginiChapter 6 Introduction To InvestmentsAyen Kaye IbisÎncă nu există evaluări

- LESSON 3 Marketing Opportunity AnalysisDocument24 paginiLESSON 3 Marketing Opportunity AnalysisSabel Cimafranca RegalaÎncă nu există evaluări

- Are The Airlines Profiting From Your Family?: Article By: Chuck GallagherDocument5 paginiAre The Airlines Profiting From Your Family?: Article By: Chuck GallagherMarie Z. LimÎncă nu există evaluări

- Cidam - OmDocument7 paginiCidam - OmYvette Marie Yaneza NicolasÎncă nu există evaluări

- FABM 2 Module 4 Exercises Statement of Cash FlowDocument3 paginiFABM 2 Module 4 Exercises Statement of Cash FlowJennifer NayveÎncă nu există evaluări

- Entrepreneurship Report 1Document30 paginiEntrepreneurship Report 1Fretchie Anne LauroÎncă nu există evaluări

- Accounting Process-QuestionnairesDocument7 paginiAccounting Process-QuestionnairesJennifer ArcadioÎncă nu există evaluări

- Business Finance: Review of Financial Statement Preparation, Analysis and InterpretationDocument33 paginiBusiness Finance: Review of Financial Statement Preparation, Analysis and InterpretationMelissa BattadÎncă nu există evaluări

- Chapter 1, 2 and 3Document34 paginiChapter 1, 2 and 3meriiÎncă nu există evaluări

- Kalinga Colleges of Science and Technolgy Moldero St. P5 Bulanao, Tabuk City, Kalinga 3800 College of Criminology Third YearDocument3 paginiKalinga Colleges of Science and Technolgy Moldero St. P5 Bulanao, Tabuk City, Kalinga 3800 College of Criminology Third YearJaden Fate SalidaÎncă nu există evaluări

- Business Mathematics - Module 5 - Mark On Mark Up and MarkdownDocument15 paginiBusiness Mathematics - Module 5 - Mark On Mark Up and MarkdownRenmel Joseph PurisimaÎncă nu există evaluări

- Introducing Organizational BehaviorDocument30 paginiIntroducing Organizational BehaviorOvaIs MoInÎncă nu există evaluări

- Business Finance - LAS - q1 - w1 Introduction To Financial Management PDFDocument9 paginiBusiness Finance - LAS - q1 - w1 Introduction To Financial Management PDFJustineÎncă nu există evaluări

- Managerial Accounting Course OutlineDocument4 paginiManagerial Accounting Course OutlineASMARA HABIB100% (1)

- BDI3C Evaluation Rubric For Entrepreneurial Venture PlanDocument3 paginiBDI3C Evaluation Rubric For Entrepreneurial Venture PlanRenante DeseoÎncă nu există evaluări

- BankingDocument2 paginiBankingapi-234284411Încă nu există evaluări

- 3 Transcription and Translation SpedDocument22 pagini3 Transcription and Translation Spedapi-234284411Încă nu există evaluări

- 2 Dna Structure and ReplicationDocument20 pagini2 Dna Structure and Replicationapi-234284411Încă nu există evaluări

- 1 Dna The Code of LifeDocument16 pagini1 Dna The Code of Lifeapi-234284411Încă nu există evaluări

- Standard 7 - Byzantine EmpireDocument6 paginiStandard 7 - Byzantine Empireapi-234284411Încă nu există evaluări

- The Sun Earth Moon SystemDocument5 paginiThe Sun Earth Moon Systemapi-234284411Încă nu există evaluări

- VMP 930 Veterinary Parasitology: Paragonimus KellicottiDocument63 paginiVMP 930 Veterinary Parasitology: Paragonimus KellicottiRenien Khim BahayaÎncă nu există evaluări

- MME 52106 - Optimization in Matlab - NN ToolboxDocument14 paginiMME 52106 - Optimization in Matlab - NN ToolboxAdarshÎncă nu există evaluări

- Mahesh R Pujar: (Volume3, Issue2)Document6 paginiMahesh R Pujar: (Volume3, Issue2)Ignited MindsÎncă nu există evaluări

- IcarosDesktop ManualDocument151 paginiIcarosDesktop ManualAsztal TavoliÎncă nu există evaluări

- Haier in India Building Presence in A Mass Market Beyond ChinaDocument14 paginiHaier in India Building Presence in A Mass Market Beyond ChinaGaurav Sharma100% (1)

- Formula:: High Low Method (High - Low) Break-Even PointDocument24 paginiFormula:: High Low Method (High - Low) Break-Even PointRedgie Mark UrsalÎncă nu există evaluări

- Trade MarkDocument2 paginiTrade MarkRohit ThoratÎncă nu există evaluări

- ADC of PIC MicrocontrollerDocument4 paginiADC of PIC Microcontrollerkillbill100% (2)

- Grid Pattern PortraitDocument8 paginiGrid Pattern PortraitEmma FravigarÎncă nu există evaluări

- Santu BabaDocument2 paginiSantu Babaamveryhot0950% (2)

- Architectural ConcreteDocument24 paginiArchitectural ConcreteSaud PathiranaÎncă nu există evaluări

- Computers in Industry: Hugh Boyes, Bil Hallaq, Joe Cunningham, Tim Watson TDocument12 paginiComputers in Industry: Hugh Boyes, Bil Hallaq, Joe Cunningham, Tim Watson TNawabMasidÎncă nu există evaluări

- 3 Diversion&CareDocument2 pagini3 Diversion&CareRyan EncomiendaÎncă nu există evaluări

- School Based INSET Interim EvaluationDocument8 paginiSchool Based INSET Interim Evaluationprinces arcangelÎncă nu există evaluări

- Cyclic MeditationDocument8 paginiCyclic MeditationSatadal GuptaÎncă nu există evaluări

- DFo 2 1Document15 paginiDFo 2 1Donna HernandezÎncă nu există evaluări

- Electronic Spin Inversion: A Danger To Your HealthDocument4 paginiElectronic Spin Inversion: A Danger To Your Healthambertje12Încă nu există evaluări

- 5 Minute Pediatric ConsultDocument5 pagini5 Minute Pediatric Consultajescool0% (4)

- Grade 9 Science Biology 1 DLPDocument13 paginiGrade 9 Science Biology 1 DLPManongdo AllanÎncă nu există evaluări

- FpsecrashlogDocument19 paginiFpsecrashlogtim lokÎncă nu există evaluări

- Statistics and Probability: Quarter 4 - (Week 6)Document8 paginiStatistics and Probability: Quarter 4 - (Week 6)Jessa May MarcosÎncă nu există evaluări

- Dakua Makadre PresentationDocument12 paginiDakua Makadre PresentationEli Briggs100% (1)

- Organization Culture Impacts On Employee Motivation: A Case Study On An Apparel Company in Sri LankaDocument4 paginiOrganization Culture Impacts On Employee Motivation: A Case Study On An Apparel Company in Sri LankaSupreet PurohitÎncă nu există evaluări

- Frellwits Swedish Hosts FileDocument10 paginiFrellwits Swedish Hosts FileAnonymous DsGzm0hQf5Încă nu există evaluări

- Disclosure To Promote The Right To InformationDocument11 paginiDisclosure To Promote The Right To InformationnmclaughÎncă nu există evaluări

- Epreuve Anglais EG@2022Document12 paginiEpreuve Anglais EG@2022Tresor SokoudjouÎncă nu există evaluări

- Assignment 4Document5 paginiAssignment 4Hafiz AhmadÎncă nu există evaluări

- Internship Report Format For Associate Degree ProgramDocument5 paginiInternship Report Format For Associate Degree ProgramBisma AmjaidÎncă nu există evaluări

- BackgroundsDocument13 paginiBackgroundsRaMinah100% (8)

- BJAS - Volume 5 - Issue Issue 1 Part (2) - Pages 275-281Document7 paginiBJAS - Volume 5 - Issue Issue 1 Part (2) - Pages 275-281Vengky UtamiÎncă nu există evaluări