S-ar putea să vă placă și

- Top 20 Corporate Finance Interview Questions (With Answers) PDFDocument19 paginiTop 20 Corporate Finance Interview Questions (With Answers) PDFDipak MahalikÎncă nu există evaluări

- The 8 Biggest Investing MythsDocument63 paginiThe 8 Biggest Investing MythsBen CarlsonÎncă nu există evaluări

- EY Funding For Growth The EY Guide To Going PublicDocument2 paginiEY Funding For Growth The EY Guide To Going PublicAayushi AroraÎncă nu există evaluări

- Gestures - 20 PG PDFDocument20 paginiGestures - 20 PG PDFDimitriu OtiliaÎncă nu există evaluări

- Gamma Scalping & Pyramiding Long StraddleDocument3 paginiGamma Scalping & Pyramiding Long StraddleMayuresh Deshpande0% (2)

- WVC Mica Research Report - 2018Document11 paginiWVC Mica Research Report - 2018Jenn MillerÎncă nu există evaluări

- Alibaba Group - From Strength To Strength - An Overview of The Business Units of The World's Largest E-Commerce CompanyDocument67 paginiAlibaba Group - From Strength To Strength - An Overview of The Business Units of The World's Largest E-Commerce CompanyKitchenConnectionÎncă nu există evaluări

- Jakarta Investment ProjectDocument63 paginiJakarta Investment ProjectLuqmanSudradjatÎncă nu există evaluări

- B Com Core Cost AccountingDocument116 paginiB Com Core Cost AccountingPRIYANKA H MEHTA100% (1)

- Capital Markets Explained: Primary & Secondary Markets, Securities, PlayersDocument5 paginiCapital Markets Explained: Primary & Secondary Markets, Securities, PlayersMaría Mercedes RedondoÎncă nu există evaluări

- Strictly Private and Confidential Road to IPODocument24 paginiStrictly Private and Confidential Road to IPOedyÎncă nu există evaluări

- Daftar Kode Dokumen IsoDocument8 paginiDaftar Kode Dokumen IsoRizky Peace CooperÎncă nu există evaluări

- Getting The Most Out of Finance Shared ServicesDocument10 paginiGetting The Most Out of Finance Shared ServicesangelwingsbondedÎncă nu există evaluări

- Salomon FRNDocument36 paginiSalomon FRNisas100% (1)

- FAQ On InvestmentDocument80 paginiFAQ On InvestmentIrka PlayingÎncă nu există evaluări

- COVID-19: Africa Economic Impact - Kenya Deep-Dive: Overall and Kenya PerspectiveDocument31 paginiCOVID-19: Africa Economic Impact - Kenya Deep-Dive: Overall and Kenya PerspectiveitzwingerÎncă nu există evaluări

- Prepare Cost SheetDocument17 paginiPrepare Cost SheetRajuSharmiÎncă nu există evaluări

- Prepare Cost SheetDocument17 paginiPrepare Cost SheetRajuSharmiÎncă nu există evaluări

- ADBHB - Eco Industrial park-Ch3CommunityDocument11 paginiADBHB - Eco Industrial park-Ch3Communitychuotlac2605Încă nu există evaluări

- Tax Due DiligenceDocument29 paginiTax Due Diligencearya1808100% (1)

- Platform Innovation Kit - User Guide 1.1Document27 paginiPlatform Innovation Kit - User Guide 1.1showtyme100% (1)

- Part B - Equitable Treatment of ShareholdersDocument12 paginiPart B - Equitable Treatment of ShareholdersYogaÎncă nu există evaluări

- SEA Exit LandscapeDocument36 paginiSEA Exit LandscapeDeddy DarmawanÎncă nu există evaluări

- Who Suffers For BeautyDocument41 paginiWho Suffers For Beautygenet100% (1)

- Starting Technology Based New Venture: Chapter TwoDocument37 paginiStarting Technology Based New Venture: Chapter TwoAnuka YituÎncă nu există evaluări

- Ch08 International StrategyDocument29 paginiCh08 International StrategySajesh VcÎncă nu există evaluări

- Goa Growth GuideDocument87 paginiGoa Growth GuidesatyatiwaryÎncă nu există evaluări

- DRN Kunker Review Revolusi Industri 4.0 dan Tantangan Pertanian Era Industri 4.0Document67 paginiDRN Kunker Review Revolusi Industri 4.0 dan Tantangan Pertanian Era Industri 4.0sinyodoangÎncă nu există evaluări

- WOOD Investor Presentation 1Q21Document61 paginiWOOD Investor Presentation 1Q21Anton Soco100% (1)

- (Teradata) Company Profile 200918 EngDocument12 pagini(Teradata) Company Profile 200918 EngIon SosroÎncă nu există evaluări

- Aboout Sogo SoshaDocument8 paginiAboout Sogo SoshaEko TjahjantokoÎncă nu există evaluări

- Internal Recruitment CampaignDocument3 paginiInternal Recruitment CampaignHiroko Jodi Brigitte Laura AmandaÎncă nu există evaluări

- Value Stream Mapping Design Process BisnisDocument15 paginiValue Stream Mapping Design Process BisnisTitinSupratiniÎncă nu există evaluări

- Digital Talent 101 GuideDocument20 paginiDigital Talent 101 GuideHiroko Jodi Brigitte Laura AmandaÎncă nu există evaluări

- Deloitte Uk Connecting Global Fintech Hub Federation Innotribe Innovate Finance ReportDocument116 paginiDeloitte Uk Connecting Global Fintech Hub Federation Innotribe Innovate Finance ReportCrowdfundInsider100% (9)

- 01 Cont Improvement KaizenDocument35 pagini01 Cont Improvement Kaizenayuditha100% (1)

- Corporate Finance Chapter10Document55 paginiCorporate Finance Chapter10James ManningÎncă nu există evaluări

- Capital Budgeting: Presenter's Name Presenter's Title DD Month YyyyDocument84 paginiCapital Budgeting: Presenter's Name Presenter's Title DD Month YyyyKazi HasanÎncă nu există evaluări

- DR Fathema Djan - Materi PERSI V3.1 Final - CompressedDocument40 paginiDR Fathema Djan - Materi PERSI V3.1 Final - CompressedcandraferdianhandriÎncă nu există evaluări

- Map Besar Kawasan Industri JababekaDocument2 paginiMap Besar Kawasan Industri JababekanerokrnÎncă nu există evaluări

- Selection From The Official United States Bid To Host The FIFA World CupTM in 2022.Document45 paginiSelection From The Official United States Bid To Host The FIFA World CupTM in 2022.soccer_bsdÎncă nu există evaluări

- Legal Due Diligence 2020Document14 paginiLegal Due Diligence 2020syarief rohmatÎncă nu există evaluări

- Ifsa Chapter7Document49 paginiIfsa Chapter7Noor SalmanÎncă nu există evaluări

- Triputra Agro PersadaDocument34 paginiTriputra Agro PersadaPuluÎncă nu există evaluări

- McKinsey - Perspectives On Retail & Consumer Goods PDFDocument78 paginiMcKinsey - Perspectives On Retail & Consumer Goods PDFumuttk5374Încă nu există evaluări

- The Nickel AdvantageDocument52 paginiThe Nickel AdvantagePak Cheong LeungÎncă nu există evaluări

- Mergers and AcquisitionsDocument12 paginiMergers and AcquisitionsCatherine JohnsonÎncă nu există evaluări

- WOM Finance PaperDocument37 paginiWOM Finance PaperAnnisa NurrachmanÎncă nu există evaluări

- VIETNAM: A GUIDE TO ITS CAPITAL, CURRENCY, AIRPORTS, LANGUAGE AND TOP TOURIST DESTINATIONSDocument21 paginiVIETNAM: A GUIDE TO ITS CAPITAL, CURRENCY, AIRPORTS, LANGUAGE AND TOP TOURIST DESTINATIONSCassidy ZapantaÎncă nu există evaluări

- Sandro Sirait PDFDocument72 paginiSandro Sirait PDFAbu ThaqifÎncă nu există evaluări

- Group 5 - Transformational Leadership - Assignment (Nedbank Case)Document4 paginiGroup 5 - Transformational Leadership - Assignment (Nedbank Case)Jahja100% (1)

- Kemenko Perekonomian - Pengembangan Sistem Logistik Nasional (Perpres 26 - 2012) VFDocument71 paginiKemenko Perekonomian - Pengembangan Sistem Logistik Nasional (Perpres 26 - 2012) VFAriyo BimmoÎncă nu există evaluări

- Organization of The Book: Part I: Foundations of Global StrategyDocument20 paginiOrganization of The Book: Part I: Foundations of Global StrategyDonart BerishaÎncă nu există evaluări

- Emerging Models of Corporate EnterpreneurshipDocument6 paginiEmerging Models of Corporate EnterpreneurshipRiaÎncă nu există evaluări

- Chaebols and KeiretsusDocument11 paginiChaebols and Keiretsusamya_sinha11Încă nu există evaluări

- Mergers and Acquisitions (M&as) in The Nigerian BankingDocument10 paginiMergers and Acquisitions (M&as) in The Nigerian BankingRitji DimkaÎncă nu există evaluări

- 16739803af 3c58e2a0f3 PDFDocument591 pagini16739803af 3c58e2a0f3 PDFUcok Riswandi NasutionÎncă nu există evaluări

- CHAPTER 8 - Corporate StrategyDocument5 paginiCHAPTER 8 - Corporate Strategyhaibinh_2212Încă nu există evaluări

- MBA Syllabus Breaks Down Business Strategy CourseDocument16 paginiMBA Syllabus Breaks Down Business Strategy CourseSerly SanoniÎncă nu există evaluări

- Islamic Banking: Strengths, Weakness, and Areas of GrowthDocument11 paginiIslamic Banking: Strengths, Weakness, and Areas of Growthnamin_amir100% (3)

- Lote Tree Partners Indonesia Corn Farming Investment Structure 1st Sharia ReviewDocument7 paginiLote Tree Partners Indonesia Corn Farming Investment Structure 1st Sharia ReviewBangkit ari wijayaÎncă nu există evaluări

- DSS Benefits and Implementation ChallengesDocument26 paginiDSS Benefits and Implementation Challengesueki77Încă nu există evaluări

- Role of Customer Delight - IpsosDocument12 paginiRole of Customer Delight - IpsosSugandha TanejaÎncă nu există evaluări

- STARBUCK Entry StrategyDocument13 paginiSTARBUCK Entry StrategySHAHE_NAJAF26560% (1)

- Understanding Holding CompaniesDocument20 paginiUnderstanding Holding CompaniesShubham MittalÎncă nu există evaluări

- Time Value of Money Summary SheetDocument4 paginiTime Value of Money Summary SheetnaliniymtÎncă nu există evaluări

- Lombok Market Analysis and Tourism Demand ForecastDocument187 paginiLombok Market Analysis and Tourism Demand Forecastdiko pridieÎncă nu există evaluări

- Produk Dan Operasional Financial TechnologyDocument110 paginiProduk Dan Operasional Financial TechnologyAhmad Wafa MansurÎncă nu există evaluări

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 paginiDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyKavin Ur FrndÎncă nu există evaluări

- Use of Foundry Sand in Conventional Concrete: Department of Civil Engineering PCE, Nagpur, Maharashtra, IndiaDocument6 paginiUse of Foundry Sand in Conventional Concrete: Department of Civil Engineering PCE, Nagpur, Maharashtra, IndiaPRAKÎncă nu există evaluări

- Eco TalkDocument2 paginiEco TalkPRAKÎncă nu există evaluări

- Hmsi Case Study IndiaDocument17 paginiHmsi Case Study IndiaPRAKÎncă nu există evaluări

- Feasibility of Fly Ash Brick: A Case Study of Surat & Tapi District of South Gujarat RegionDocument6 paginiFeasibility of Fly Ash Brick: A Case Study of Surat & Tapi District of South Gujarat RegionPRAKÎncă nu există evaluări

- Corporate Finance Chapter1Document29 paginiCorporate Finance Chapter1ankitakoli1995Încă nu există evaluări

- MCQ For BomDocument53 paginiMCQ For BomshashiÎncă nu există evaluări

- 2008 Simon Parker PresentationDocument25 pagini2008 Simon Parker PresentationPRAKÎncă nu există evaluări

- DerivativesPromo PDFDocument2 paginiDerivativesPromo PDFPRAKÎncă nu există evaluări

- Inventroy ValnDocument18 paginiInventroy ValnDrpranav SaraswatÎncă nu există evaluări

- Seven Great Reasons For Tebis Consulting: Process EfficiencyDocument8 paginiSeven Great Reasons For Tebis Consulting: Process EfficiencyPRAKÎncă nu există evaluări

- Body LanguageDocument12 paginiBody LanguagePRAKÎncă nu există evaluări

- Concept of MacroeconomyDocument7 paginiConcept of MacroeconomyTathagata ChakrabortiÎncă nu există evaluări

- Marchioni On Foundry Sand in Paving UnitsDocument12 paginiMarchioni On Foundry Sand in Paving UnitsPRAKÎncă nu există evaluări

- MCQ On FM PDFDocument28 paginiMCQ On FM PDFharsh snehÎncă nu există evaluări

- Paper 14362Document9 paginiPaper 14362PRAKÎncă nu există evaluări

- Excel Formula For CADocument61 paginiExcel Formula For CArameshritikaÎncă nu există evaluări

- 2008 Simon Parker PresentationDocument25 pagini2008 Simon Parker PresentationPRAKÎncă nu există evaluări

- Body Language Humor: by Don L. F. Nilsen and Alleen Pace NilsenDocument68 paginiBody Language Humor: by Don L. F. Nilsen and Alleen Pace NilsenPRAKÎncă nu există evaluări

- MCQ On FM PDFDocument28 paginiMCQ On FM PDFharsh snehÎncă nu există evaluări

- Measures of Leverage: Presenter's Name Presenter's Title DD Month YyyyDocument21 paginiMeasures of Leverage: Presenter's Name Presenter's Title DD Month YyyybingoÎncă nu există evaluări

- Body Language in The Classroom - Important PDFDocument10 paginiBody Language in The Classroom - Important PDFPRAKÎncă nu există evaluări

- Dividends and Share Repurchases: Analysis: Presenter's Name Presenter's Title DD Month YyyyDocument23 paginiDividends and Share Repurchases: Analysis: Presenter's Name Presenter's Title DD Month YyyybingoÎncă nu există evaluări

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 paginiDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyPRAKÎncă nu există evaluări

- Corporate Finance Chapter2Document84 paginiCorporate Finance Chapter2PRAKÎncă nu există evaluări

- Corporate Finance Chapter1Document29 paginiCorporate Finance Chapter1ankitakoli1995Încă nu există evaluări

- Calculate Payoffs and Prices for Options on Various UnderlyingsDocument6 paginiCalculate Payoffs and Prices for Options on Various Underlyingssufyanbutt007Încă nu există evaluări

- Stripped Market Backed SecuritiesDocument12 paginiStripped Market Backed SecuritiesDisha GanatraÎncă nu există evaluări

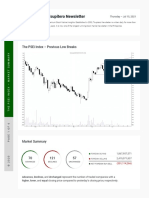

- Tsupitero Newsletter: The Psei Index - Previous Low BreaksDocument6 paginiTsupitero Newsletter: The Psei Index - Previous Low BreaksEdsel LoquillanoÎncă nu există evaluări

- CD 18178Document4 paginiCD 18178Srinu RachuriÎncă nu există evaluări

- ICICI Prudential Life Insurance ProspectusDocument616 paginiICICI Prudential Life Insurance ProspectusshamruthaÎncă nu există evaluări

- Practice Questions for AMFI TestDocument36 paginiPractice Questions for AMFI TestKajal TripathiÎncă nu există evaluări

- CorpF ReviseDocument5 paginiCorpF ReviseTrang DangÎncă nu există evaluări

- Option Pricing Using Trinomial Model With Memoization - Siteng JinDocument10 paginiOption Pricing Using Trinomial Model With Memoization - Siteng Jinapi-262753233Încă nu există evaluări

- My Project-1Document55 paginiMy Project-1Hemant Kumar AhirwarÎncă nu există evaluări

- Course Out BoomDocument8 paginiCourse Out BoomrahulkatareyÎncă nu există evaluări

- Accounting For Share Capital (2019-20)Document20 paginiAccounting For Share Capital (2019-20)niyatiagarwal25Încă nu există evaluări

- Solution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyDocument6 paginiSolution Manual For Global Investments 6 e 6th Edition Bruno Solnik Dennis McleaveyAntonioHallbnoa100% (41)

- Stocks and Their Valuation: Taufikur@ugm - Ac.idDocument43 paginiStocks and Their Valuation: Taufikur@ugm - Ac.idNeneng Wulandari100% (1)

- OptionsDocument51 paginiOptionsKaren Hoffman100% (1)

- Daily Technical Analysis Report: Main IndexDocument3 paginiDaily Technical Analysis Report: Main IndexAbdullah MantawyÎncă nu există evaluări

- Uti Us-64 ReportDocument25 paginiUti Us-64 ReportRupam PaulÎncă nu există evaluări

- Investment Banking Strategies and Key Issues: Kaan Sarıaydın 23 November 2009, Bilgi UniversityDocument57 paginiInvestment Banking Strategies and Key Issues: Kaan Sarıaydın 23 November 2009, Bilgi UniversityAshish SharmaÎncă nu există evaluări

- OIS CurvesbbgDocument26 paginiOIS CurvesbbgQKÎncă nu există evaluări

- Coursefm 1105Document26 paginiCoursefm 1105api-3723125100% (1)

- Soneri Bank Limited Balance SheetDocument3 paginiSoneri Bank Limited Balance SheetSaad Ur RehmanÎncă nu există evaluări

- Real Time Data Get From Stock Exchange Using PHPDocument6 paginiReal Time Data Get From Stock Exchange Using PHPAsad Ullah KhanÎncă nu există evaluări

- Sources and Raising of LT FinanceDocument52 paginiSources and Raising of LT FinanceAshutoshÎncă nu există evaluări

- Supplemental Information Fourth Quarter 2009Document66 paginiSupplemental Information Fourth Quarter 2009ariw99Încă nu există evaluări

- Cfin 6th Edition Besley Test BankDocument15 paginiCfin 6th Edition Besley Test Bankdrkevinlee03071984jki100% (26)

- SEBI (Delisting of Equity Shares) (Amendment) Regulations, 2015Document11 paginiSEBI (Delisting of Equity Shares) (Amendment) Regulations, 2015Shyam SunderÎncă nu există evaluări