S-ar putea să vă placă și

- Sale DeedDocument5 paginiSale DeedNitin GoyalÎncă nu există evaluări

- Income Declaration Scheme Rules, 2016: Form 1Document9 paginiIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatÎncă nu există evaluări

- Derivatives Markets in Interest Rate & Foreign Exchange RateDocument20 paginiDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfÎncă nu există evaluări

- DTL Sec 10Document14 paginiDTL Sec 10Nikhil KasatÎncă nu există evaluări

- Types of Stamps and Some Concepts of Stamp DutyDocument5 paginiTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

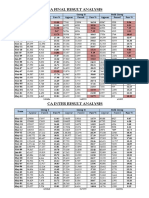

- CA Result AnalysisDocument1 paginăCA Result AnalysisNikhil KasatÎncă nu există evaluări

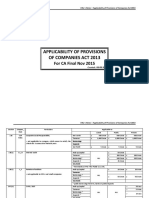

- ApplicabiliTY of ProvisionsDocument3 paginiApplicabiliTY of ProvisionsNikhil KasatÎncă nu există evaluări

- Anf 4dDocument3 paginiAnf 4dNikhil KasatÎncă nu există evaluări

- Black Money BillDocument30 paginiBlack Money BillNikhil KasatÎncă nu există evaluări

- BLack Money RulesDocument23 paginiBLack Money RulesLive LawÎncă nu există evaluări

- Delhi Dvat Registration InformationDocument4 paginiDelhi Dvat Registration InformationNikhil KasatÎncă nu există evaluări

- Banca SuranceDocument32 paginiBanca SuranceNikhil KasatÎncă nu există evaluări

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Document21 paginiSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatÎncă nu există evaluări

- Hedging With Financial DerivativesDocument30 paginiHedging With Financial DerivativesNikhil KasatÎncă nu există evaluări

- CA Final Writing Professional Ethics AnswersDocument2 paginiCA Final Writing Professional Ethics AnswersNikhil KasatÎncă nu există evaluări

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDocument10 paginiFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatÎncă nu există evaluări

- Directors Report As Per StatusDocument5 paginiDirectors Report As Per StatusNikhil KasatÎncă nu există evaluări

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDocument9 paginiAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatÎncă nu există evaluări

- Curriculum VitaeDocument13 paginiCurriculum VitaeNikhil KasatÎncă nu există evaluări

- Web Base Timesheet ApplicationDocument4 paginiWeb Base Timesheet ApplicationNikhil KasatÎncă nu există evaluări

- List of Indian As Convergence With IfrsDocument1 paginăList of Indian As Convergence With IfrsNikhil KasatÎncă nu există evaluări

- Tds On SalariesDocument55 paginiTds On SalariespunitÎncă nu există evaluări

- Ind As 2015Document2 paginiInd As 2015Nikhil KasatÎncă nu există evaluări

- C01Document23 paginiC01Silvery DoeÎncă nu există evaluări

- August Month CompliancesDocument1 paginăAugust Month CompliancesNikhil KasatÎncă nu există evaluări

- Privileges To Small CompaniesDocument2 paginiPrivileges To Small CompaniesNikhil KasatÎncă nu există evaluări

- Importance of ArticleshipDocument6 paginiImportance of ArticleshipNikhil KasatÎncă nu există evaluări

- Cusoms Valuation MaterialDocument8 paginiCusoms Valuation MaterialNikhil KasatÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Cartonboard Case Study PDFDocument4 paginiCartonboard Case Study PDFROEIGHTÎncă nu există evaluări

- Task 13 Present Tense Grammar Economic ExamplesDocument2 paginiTask 13 Present Tense Grammar Economic ExamplesOsmar Braulio Quino RamirezÎncă nu există evaluări

- Narayana MurthyDocument11 paginiNarayana MurthyMrunalkanta DasÎncă nu există evaluări

- Complete Topic 1 - Cost - Cost ClassificationDocument12 paginiComplete Topic 1 - Cost - Cost ClassificationchaiigasperÎncă nu există evaluări

- Assessment of Income From House PropertyDocument15 paginiAssessment of Income From House PropertyManish SinghÎncă nu există evaluări

- A Study On Customer Preference Towards Brand FactoryDocument21 paginiA Study On Customer Preference Towards Brand FactoryH.Arokiaraj100% (2)

- PM5114 IVLE Lecture1Document23 paginiPM5114 IVLE Lecture1Ravi ShankarÎncă nu există evaluări

- Human Resource Management Practices at The National Thermal Power Corporation (NTPC) in IndiaDocument34 paginiHuman Resource Management Practices at The National Thermal Power Corporation (NTPC) in Indiagramana10Încă nu există evaluări

- Bank ExpressionsDocument8 paginiBank ExpressionsMónica GonzálezÎncă nu există evaluări

- International Marketing Solved MCQs (Set-1)Document6 paginiInternational Marketing Solved MCQs (Set-1)Priyanka MahajanÎncă nu există evaluări

- Financial Markets and Services NotesDocument94 paginiFinancial Markets and Services NotesShravan Richie100% (7)

- Percent Per Day Binary Options CalculatorDocument4 paginiPercent Per Day Binary Options CalculatorJohn BoydÎncă nu există evaluări

- Repeat Until Rich EbookDocument7 paginiRepeat Until Rich Ebookliviubbcel50% (2)

- Royal Decree 50 of 2023 Promulgating The System of The Social Protection FundDocument4 paginiRoyal Decree 50 of 2023 Promulgating The System of The Social Protection FundmsadiqcsÎncă nu există evaluări

- Bài Báo Thu MuaDocument10 paginiBài Báo Thu MuaMinh TânÎncă nu există evaluări

- Final Report Askari BankDocument117 paginiFinal Report Askari BankAsha JadunÎncă nu există evaluări

- Foundations of Economics 6th Edition Bade Test Bank 1Document89 paginiFoundations of Economics 6th Edition Bade Test Bank 1james100% (39)

- Business Plan Aprils Group 1Document19 paginiBusiness Plan Aprils Group 1Lealyn Alupay YagaoÎncă nu există evaluări

- Pre Qualification Form - Electrical ItemsDocument16 paginiPre Qualification Form - Electrical Itemssahuharish_gÎncă nu există evaluări

- 34 48 48 39 66 64 46 24 53 64 54 56 83 31 Total Result 442 268 710 38%Document89 pagini34 48 48 39 66 64 46 24 53 64 54 56 83 31 Total Result 442 268 710 38%Agus MaulanaÎncă nu există evaluări

- Lecture Chapter 6: Productivity and Human Capital I. Standard of Living Around The WorldDocument6 paginiLecture Chapter 6: Productivity and Human Capital I. Standard of Living Around The WorldKatherine SauerÎncă nu există evaluări

- HRP Case StudyDocument1 paginăHRP Case Studymruga_123Încă nu există evaluări

- Faq On Kyc Aml PDFDocument4 paginiFaq On Kyc Aml PDFSiva KumarÎncă nu există evaluări

- Bryan Ic3 Worksheet Module 1Document7 paginiBryan Ic3 Worksheet Module 1Bryan Riños Cahulogan IIÎncă nu există evaluări

- Water Refilling Station Business ProposalDocument4 paginiWater Refilling Station Business ProposalCarren BorasÎncă nu există evaluări

- ERP Post Implementation Challenges 3Document11 paginiERP Post Implementation Challenges 3Neelesh KumarÎncă nu există evaluări

- Hire Purchase and Credit Sale Act 2013Document35 paginiHire Purchase and Credit Sale Act 2013karlpragassenÎncă nu există evaluări

- GPS vs. TJX Financial AnalysisDocument12 paginiGPS vs. TJX Financial AnalysisBen Van NesteÎncă nu există evaluări

- Cryptocurrency and The Future of FinanceDocument9 paginiCryptocurrency and The Future of FinanceJawad NadeemÎncă nu există evaluări

- 1Document51 pagini1dakine.kdkÎncă nu există evaluări