S-ar putea să vă placă și

- CH 6 (WWW - Jamaa Bzu - Com)Document8 paginiCH 6 (WWW - Jamaa Bzu - Com)Bayan Sharif100% (2)

- Audit of Liabilities: Audit Program For Accounts Payable Audit ObjectivesDocument18 paginiAudit of Liabilities: Audit Program For Accounts Payable Audit ObjectivesSarah PuspawatiÎncă nu există evaluări

- This Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)Document8 paginiThis Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)NCT100% (1)

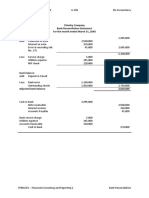

- Module 2 Bank Reconciliation Proof of CashDocument2 paginiModule 2 Bank Reconciliation Proof of CashziÎncă nu există evaluări

- Accounting Problems and SolutionsDocument17 paginiAccounting Problems and SolutionsLoyalNamanAko LLÎncă nu există evaluări

- This Study Resource Was: Problem IDocument8 paginiThis Study Resource Was: Problem IMs VampireÎncă nu există evaluări

- Lower-of-Cost-or-Market Valuation IssuesDocument31 paginiLower-of-Cost-or-Market Valuation Issuesalice123h21Încă nu există evaluări

- Partnership Operations ProblemsDocument2 paginiPartnership Operations ProblemsAilene MendozaÎncă nu există evaluări

- Darantan, KC T. - FAR Module 6Document3 paginiDarantan, KC T. - FAR Module 6Li LiÎncă nu există evaluări

- C3 - Matching and Adjusting ProcessDocument12 paginiC3 - Matching and Adjusting ProcessIvy Jean Ybera-PapasinÎncă nu există evaluări

- End Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying AbilityDocument4 paginiEnd Beginning of Year of Year: Liquidity of Short-Term Assets Related Debt-Paying Abilityawaischeema100% (1)

- Quali - ReviewDocument32 paginiQuali - ReviewLA M AEÎncă nu există evaluări

- Basic accounting for defined benefit plansDocument23 paginiBasic accounting for defined benefit plansKristine Diane CABAnASÎncă nu există evaluări

- Depletion Notes: Disclaimer: Not EntirelyDocument3 paginiDepletion Notes: Disclaimer: Not EntirelyRes GosanÎncă nu există evaluări

- Reviewer Controlling Cash Part 1Document6 paginiReviewer Controlling Cash Part 1Mikey Irwin0% (2)

- Lecture Note - Receivables Sy 2014-2015Document10 paginiLecture Note - Receivables Sy 2014-2015LeneÎncă nu există evaluări

- Quiz 1 Midterm InventoriesDocument6 paginiQuiz 1 Midterm InventoriesSophia TenorioÎncă nu există evaluări

- Cleaners WorksheetDocument1 paginăCleaners WorksheetSeijuro AkashiÎncă nu există evaluări

- Chapter 7: Receivables: Principles of AccountingDocument50 paginiChapter 7: Receivables: Principles of AccountingRohail Javed100% (1)

- 2 3 2017 ReceivablesDocument4 pagini2 3 2017 ReceivablesMr. CopernicusÎncă nu există evaluări

- UCP: CVP Analysis and ExercisesDocument10 paginiUCP: CVP Analysis and ExercisesDin Rose GonzalesÎncă nu există evaluări

- Bsat 2019Document23 paginiBsat 2019rowena adobasÎncă nu există evaluări

- 1n2 QuestionDocument3 pagini1n2 QuestionJohn_Byron_Ign_270100% (1)

- Problem 18 - 18 18 - 31 and 18 - 32Document5 paginiProblem 18 - 18 18 - 31 and 18 - 32anon_459698449Încă nu există evaluări

- Cup - Basic ParcorDocument8 paginiCup - Basic ParcorJerauld BucolÎncă nu există evaluări

- 5A Review of Accounting Process PDFDocument7 pagini5A Review of Accounting Process PDFAldrin Jay SalcedoÎncă nu există evaluări

- Master Budget BreakdownDocument45 paginiMaster Budget BreakdownJay Mark AbellarÎncă nu există evaluări

- Notes in Acstr14Document3 paginiNotes in Acstr14Gray JavierÎncă nu există evaluări

- Three Methods of Estimating Doubtful AccountsDocument8 paginiThree Methods of Estimating Doubtful AccountsJay Lou PayotÎncă nu există evaluări

- Isabela State University: MA 112 - Conceptual Framework & Accounting Standards - Chapter 1Document18 paginiIsabela State University: MA 112 - Conceptual Framework & Accounting Standards - Chapter 1Chraze GBÎncă nu există evaluări

- Bam 040 ReviewerDocument7 paginiBam 040 ReviewerAndrea Vila VelascoÎncă nu există evaluări

- Accounting For Factory OverheadDocument27 paginiAccounting For Factory Overheadspectrum_480% (1)

- Bank Reconciliation PDFDocument3 paginiBank Reconciliation PDFJerald Jay CatacutanÎncă nu există evaluări

- My Company Unadjusted Trial Balance December 31, 2018 Debit CreditDocument9 paginiMy Company Unadjusted Trial Balance December 31, 2018 Debit CreditRey Joyce AbuelÎncă nu există evaluări

- Inventory Costing and Capacity Analysis: True/FalseDocument56 paginiInventory Costing and Capacity Analysis: True/FalseambiÎncă nu există evaluări

- PQ3 BondsDocument2 paginiPQ3 BondsElla Mae MagbatoÎncă nu există evaluări

- Variable costing key conceptsDocument21 paginiVariable costing key conceptsMary Rose GonzalesÎncă nu există evaluări

- StratCost Quiz 2Document6 paginiStratCost Quiz 2ElleÎncă nu există evaluări

- Question Text: Retained Earnings Retained Earnings Retained Earnings Retained EarningsDocument32 paginiQuestion Text: Retained Earnings Retained Earnings Retained Earnings Retained EarningsYou're WelcomeÎncă nu există evaluări

- Tugas Ch.20Document9 paginiTugas Ch.20Chupa HesÎncă nu există evaluări

- Firms cannot achieve competitive advantage without acting ethicallyDocument3 paginiFirms cannot achieve competitive advantage without acting ethicallyElla Amor TagsipÎncă nu există evaluări

- Risk Management Strategies for Del Monte PhilippinesDocument9 paginiRisk Management Strategies for Del Monte PhilippinesPricia AbellaÎncă nu există evaluări

- Topacio Rizza C. Activity 6-1Document12 paginiTopacio Rizza C. Activity 6-1santosashleymay7Încă nu există evaluări

- 2.6. Retained EarningsDocument5 pagini2.6. Retained EarningsKPoPNyx Edits100% (1)

- Problem Solving 1-4Document9 paginiProblem Solving 1-4Mary Ann PerezÎncă nu există evaluări

- Chapter 4 Underlying AssumptionsDocument7 paginiChapter 4 Underlying AssumptionsMicsjadeCastilloÎncă nu există evaluări

- CH 10Document39 paginiCH 10anjo hosmerÎncă nu există evaluări

- JPIA-MCL Academic-EventsDocument17 paginiJPIA-MCL Academic-EventsJana BercasioÎncă nu există evaluări

- Chapter 9 Depreciation, Amortization and DepletionDocument11 paginiChapter 9 Depreciation, Amortization and DepletionKrissa Mae Longos100% (1)

- Quiz - Acts PayableDocument2 paginiQuiz - Acts PayableAna Mae HernandezÎncă nu există evaluări

- Group Quiz InstructionsDocument9 paginiGroup Quiz InstructionsRaidenhile mae VicenteÎncă nu există evaluări

- Invest in Equity SecuritiesDocument3 paginiInvest in Equity SecuritiesGIRLÎncă nu există evaluări

- Assignment On SC and VADocument12 paginiAssignment On SC and VAVixen Aaron EnriquezÎncă nu există evaluări

- Improving Expenditure Cycle EfficiencyDocument21 paginiImproving Expenditure Cycle EfficiencyJuan Rafael FernandezÎncă nu există evaluări

- Vallix QuestionnairesDocument14 paginiVallix QuestionnairesKathleen LucasÎncă nu există evaluări

- Standard Costs and The Balanced ScorecardDocument32 paginiStandard Costs and The Balanced ScorecardfaheemÎncă nu există evaluări

- Objectives and users of financial reportingDocument2 paginiObjectives and users of financial reportingChery Sheil Valenzuela0% (2)

- Accounting - Inventory Test BankDocument3 paginiAccounting - Inventory Test BankAyesha RGÎncă nu există evaluări

- Accounting Q&ADocument50 paginiAccounting Q&AKumaar Guhan50% (2)

- Factors that shape accounting systemsDocument13 paginiFactors that shape accounting systemsJillian LaluanÎncă nu există evaluări

- Ch3 (WWW - Jamaa Bzu - Com)Document7 paginiCh3 (WWW - Jamaa Bzu - Com)Bayan SharifÎncă nu există evaluări

- CH 2 (WWW - Jamaa Bzu - Com)Document6 paginiCH 2 (WWW - Jamaa Bzu - Com)Bayan Sharif100% (1)

- Multiple Choice Questions Chapter 1Document6 paginiMultiple Choice Questions Chapter 1Bayan Sharif0% (1)

- CH 2 (WWW - Jamaa Bzu - Com)Document6 paginiCH 2 (WWW - Jamaa Bzu - Com)Bayan Sharif100% (1)

- Multiple Choice Questions Chapter 1Document6 paginiMultiple Choice Questions Chapter 1Bayan Sharif0% (1)

- MAS Annual Report 2010 - 2011Document119 paginiMAS Annual Report 2010 - 2011Ayako S. WatanabeÎncă nu există evaluări

- Problems: Solution: Philip MorrisDocument21 paginiProblems: Solution: Philip MorrisElen LimÎncă nu există evaluări

- E Stamp ArticleDocument2 paginiE Stamp ArticleShubh BanshalÎncă nu există evaluări

- Spring 2006Document40 paginiSpring 2006ed bookerÎncă nu există evaluări

- Chapter 2 How To Calculate Present ValuesDocument40 paginiChapter 2 How To Calculate Present ValuesAtheer Al-AnsariÎncă nu există evaluări

- Asli Pracheen Ravan Samhita PDFDocument2 paginiAsli Pracheen Ravan Samhita PDFgirish SharmaÎncă nu există evaluări

- Tutorial - Week12.starting A BusinessDocument4 paginiTutorial - Week12.starting A BusinessAnonymous LDvhURRXmÎncă nu există evaluări

- Act 248 Innkeepers Act 1952Document10 paginiAct 248 Innkeepers Act 1952Adam Haida & CoÎncă nu există evaluări

- T3-Sample Answers-Consideration PDFDocument10 paginiT3-Sample Answers-Consideration PDF--bolabolaÎncă nu există evaluări

- Islamic FINTECH + CoverDocument26 paginiIslamic FINTECH + CoverM Abi AbdillahÎncă nu există evaluări

- Chamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesDocument30 paginiChamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesUmarÎncă nu există evaluări

- Cash Budget:: Hampton Freeze Inc. Cash Budget For The Year Ended December 31, 2009Document11 paginiCash Budget:: Hampton Freeze Inc. Cash Budget For The Year Ended December 31, 2009renakwokÎncă nu există evaluări

- Company Report - Venus Remedies LTDDocument36 paginiCompany Report - Venus Remedies LTDseema1707Încă nu există evaluări

- Non-current Liabilities - Bonds Payable Classification and MeasurementDocument4 paginiNon-current Liabilities - Bonds Payable Classification and MeasurementhIgh QuaLIty SVTÎncă nu există evaluări

- Overview of Working Capital Management and Cash ManagementDocument48 paginiOverview of Working Capital Management and Cash ManagementChrisÎncă nu există evaluări

- FS FactoringDocument17 paginiFS FactoringJai DeepÎncă nu există evaluări

- Analysis On The Proposed Property Tax AssessmentDocument32 paginiAnalysis On The Proposed Property Tax AssessmentAB AgostoÎncă nu există evaluări

- Fria MCQDocument13 paginiFria MCQJemima LalaweÎncă nu există evaluări

- Fabm2: Quarter 1 Module 1.2 New Normal ABM For Grade 12Document19 paginiFabm2: Quarter 1 Module 1.2 New Normal ABM For Grade 12Janna Gunio0% (1)

- Global Transition of HR Practices During COVID-19Document5 paginiGlobal Transition of HR Practices During COVID-19Md. Saifullah TariqueÎncă nu există evaluări

- Ratio Analysis Pankaj 180000502015Document64 paginiRatio Analysis Pankaj 180000502015PankajÎncă nu există evaluări

- Export Policy 2015-18 aims to boost Bangladesh exportsDocument29 paginiExport Policy 2015-18 aims to boost Bangladesh exportsFaysal AhmedÎncă nu există evaluări

- Enterprise Risk Management - Beyond TheoryDocument34 paginiEnterprise Risk Management - Beyond Theoryjcl_da_costa6894100% (4)

- Draft Dispossessory Appeal OptionsDocument12 paginiDraft Dispossessory Appeal Optionswekesamadzimoyo1Încă nu există evaluări

- Hindusthan Microfinance provides loans to Mumbai's poorDocument25 paginiHindusthan Microfinance provides loans to Mumbai's poorsunnyÎncă nu există evaluări

- Solution Manual For Financial Management 13th Edition by TitmanDocument3 paginiSolution Manual For Financial Management 13th Edition by Titmanazif kurnia100% (1)

- What is Operations ResearchDocument10 paginiWhat is Operations ResearchSHILPA GOPINATHANÎncă nu există evaluări

- Credit Card Response Rates and ProfitsDocument6 paginiCredit Card Response Rates and ProfitskkiiiddÎncă nu există evaluări

- Principle of Halal PurchasingDocument13 paginiPrinciple of Halal Purchasing680105100% (1)

- 03 BIWS Equity Value Enterprise ValueDocument6 pagini03 BIWS Equity Value Enterprise ValuecarminatÎncă nu există evaluări