S-ar putea să vă placă și

- MotivationDocument22 paginiMotivationNiraj NaikÎncă nu există evaluări

- A Comparison of Car Buying Behavior BetweenDocument15 paginiA Comparison of Car Buying Behavior BetweenNiraj NaikÎncă nu există evaluări

- Submitted By:: A Project Report On "Ongc and Relinace Industires"Document23 paginiSubmitted By:: A Project Report On "Ongc and Relinace Industires"Niraj NaikÎncă nu există evaluări

- Aggregate Demand and Aggregate SupplyDocument33 paginiAggregate Demand and Aggregate SupplyNiraj NaikÎncă nu există evaluări

- Microbrew Bar B PlanDocument19 paginiMicrobrew Bar B PlanNiraj Naik100% (1)

- Watch Industry: Prepared by Niraj Naik Khanjan Munshi Amit Patel Khushbu MehtaDocument25 paginiWatch Industry: Prepared by Niraj Naik Khanjan Munshi Amit Patel Khushbu MehtaNiraj Naik100% (1)

- Amusement Park Business PlanDocument48 paginiAmusement Park Business PlanNiraj Naik67% (3)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Hitachi Air-Cooled Chiller Installation, Operation and Maintenance ManualDocument52 paginiHitachi Air-Cooled Chiller Installation, Operation and Maintenance Manualmgs nurmansyahÎncă nu există evaluări

- Data Transmission Specifications 3S4YR-MVFW (DL) - 051S Series Hybrid Card Reader/Writer Rev. A0 Rev. A1 Rev. A2 Jul. 10, 1998 Jun. 7, 1999 Jan. 15, 2001 GB-H-98058 (A2)Document43 paginiData Transmission Specifications 3S4YR-MVFW (DL) - 051S Series Hybrid Card Reader/Writer Rev. A0 Rev. A1 Rev. A2 Jul. 10, 1998 Jun. 7, 1999 Jan. 15, 2001 GB-H-98058 (A2)newbit1Încă nu există evaluări

- GCC Jaguariv UserguideDocument120 paginiGCC Jaguariv UserguideDiana ArghirÎncă nu există evaluări

- Assembly-Line Balancing: A Valuable Tool For Increasing EfficiencyDocument20 paginiAssembly-Line Balancing: A Valuable Tool For Increasing Efficiencyaqsa imranÎncă nu există evaluări

- The Roles, Artifacts, Ceremonies and Benefits of Agile Scrum (38Document14 paginiThe Roles, Artifacts, Ceremonies and Benefits of Agile Scrum (38Romali DasÎncă nu există evaluări

- Technical ProgramScheduleDocument6 paginiTechnical ProgramScheduleBiswajitRoyÎncă nu există evaluări

- C++ NotesDocument202 paginiC++ NotesdklfoodproductsÎncă nu există evaluări

- MS Agreement Product SheetDocument2 paginiMS Agreement Product SheetAbdeldjalil AchourÎncă nu există evaluări

- UniversalDocument8 paginiUniversalMateus LoufaresÎncă nu există evaluări

- Bar Graphs and AdviceddDocument9 paginiBar Graphs and AdviceddmccabeandmrsmillerÎncă nu există evaluări

- 29TC679FDocument29 pagini29TC679FGustavo ChavezÎncă nu există evaluări

- PQ Paper JNTUKDocument4 paginiPQ Paper JNTUKsundeep sÎncă nu există evaluări

- Scholarship Management System: Team Members: BM10518, BM10527, BM10545 Class: II-MCADocument30 paginiScholarship Management System: Team Members: BM10518, BM10527, BM10545 Class: II-MCAJoe Nishanth100% (3)

- Evinrude Carburetor Group Parts For 1966 18hp 18602 Outboard MotorDocument8 paginiEvinrude Carburetor Group Parts For 1966 18hp 18602 Outboard MotorWouter GrootÎncă nu există evaluări

- User Manual: EPC PM 2100Document52 paginiUser Manual: EPC PM 2100Ghoual MohamedÎncă nu există evaluări

- Monoprice Delta Mini Manual, Version 1Document20 paginiMonoprice Delta Mini Manual, Version 1Ted ThompsonÎncă nu există evaluări

- Stand-Alone Microgrid With 100% Renewable Energy: A Case Study With Hybrid Solar PV-Battery-HydrogenDocument17 paginiStand-Alone Microgrid With 100% Renewable Energy: A Case Study With Hybrid Solar PV-Battery-HydrogenShashi KumarÎncă nu există evaluări

- DocuCentre II 7000 6000 BrochureDocument4 paginiDocuCentre II 7000 6000 BrochureRumen StoychevÎncă nu există evaluări

- OSCP Personal Cheatsheet: September 18Th, 2020Document73 paginiOSCP Personal Cheatsheet: September 18Th, 2020mahesh yadavÎncă nu există evaluări

- Tariff Finder - SampleDocument4 paginiTariff Finder - SampleTrinca DiplomaÎncă nu există evaluări

- Web Lab FileDocument34 paginiWeb Lab Filesaloniaggarwal0304Încă nu există evaluări

- Twido Modbus EN PDFDocument63 paginiTwido Modbus EN PDFWilly Chayña LeonÎncă nu există evaluări

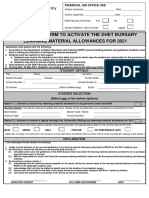

- NSFAS Laptop FormDocument2 paginiNSFAS Laptop FormKagiso China'män NtsaneÎncă nu există evaluări

- 2nd Final Version Bryan-Top-5-media-websites-24.08.2016Document210 pagini2nd Final Version Bryan-Top-5-media-websites-24.08.2016Biljana MitanovskaÎncă nu există evaluări

- Con BFM Connecting SleevesDocument2 paginiCon BFM Connecting SleevesRhiieeÎncă nu există evaluări

- Blue BrainDocument35 paginiBlue BrainMansi ParidaÎncă nu există evaluări

- Socitec - HH16Document2 paginiSocitec - HH16Andrzej RogalaÎncă nu există evaluări

- BrouchureDocument2 paginiBrouchureHARSHA VARDHINI M 20ISR020Încă nu există evaluări

- SPD39T 39B6X Service Manual-01-0226 PDFDocument63 paginiSPD39T 39B6X Service Manual-01-0226 PDFAlejandroVCMXÎncă nu există evaluări

- Program Design and Algorithm AnalysisDocument50 paginiProgram Design and Algorithm AnalysisKaran RoyÎncă nu există evaluări