S-ar putea să vă placă și

- A Summary of The Conference On Consumer Transactions and CreditDocument5 paginiA Summary of The Conference On Consumer Transactions and CreditFlaviub23Încă nu există evaluări

- Loan Rate Stickiness Theory and EvidenceDocument46 paginiLoan Rate Stickiness Theory and EvidencerunawayyyÎncă nu există evaluări

- Literature Review On Bank LendingDocument8 paginiLiterature Review On Bank Lendingc5td1cmc100% (1)

- WH Credit Card DataDocument39 paginiWH Credit Card DataFlaviub23Încă nu există evaluări

- SSRN Id3405897 PDFDocument62 paginiSSRN Id3405897 PDFAnurag BhosaleÎncă nu există evaluări

- Credit LinesDocument43 paginiCredit Linespdastous1Încă nu există evaluări

- Hedging ChannelsDocument33 paginiHedging ChannelsTanushree RoyÎncă nu există evaluări

- The Time-Varying Price of Financial Intermediation in The Mortgage MarketDocument65 paginiThe Time-Varying Price of Financial Intermediation in The Mortgage MarketLuana SavoretoÎncă nu există evaluări

- John Berlau - The 400 Percent LoanDocument7 paginiJohn Berlau - The 400 Percent LoanCompetitive Enterprise InstituteÎncă nu există evaluări

- Information Disclosure, Cognitive Biases, and Payday BorrowingDocument29 paginiInformation Disclosure, Cognitive Biases, and Payday BorrowingAinoa Rodriguez BeasainÎncă nu există evaluări

- Consumer Response To Changes in Credit Supply: Evidence From Credit Card DataDocument37 paginiConsumer Response To Changes in Credit Supply: Evidence From Credit Card DataArunabh ChoudhuryÎncă nu există evaluări

- Household Financial Constraints and Risk Profile Impact on Mortgage RatesDocument25 paginiHousehold Financial Constraints and Risk Profile Impact on Mortgage Ratesmkashif041Încă nu există evaluări

- Sank ArdeDocument47 paginiSank Ardejay.kumÎncă nu există evaluări

- Dissertation Report On Working Capital ManagementDocument33 paginiDissertation Report On Working Capital ManagementAnirudh SinghaÎncă nu există evaluări

- New YorkDocument50 paginiNew YorkAdminAliÎncă nu există evaluări

- St. Gallen, Switzerland, August 22-28, 2010Document32 paginiSt. Gallen, Switzerland, August 22-28, 2010vaibhav2020Încă nu există evaluări

- FRIED & HOWITT, Credit Rationing and Implicit Contract TheoryDocument18 paginiFRIED & HOWITT, Credit Rationing and Implicit Contract TheoryAnonymous ykRTOEÎncă nu există evaluări

- 65c6914e - Hinh Khieu외2인Document46 pagini65c6914e - Hinh Khieu외2인brendan lanzaÎncă nu există evaluări

- Final Report Data Analysis Example 1 TemplateDocument9 paginiFinal Report Data Analysis Example 1 Template周姿馨Încă nu există evaluări

- Beauty Is in The Eye of The Beholder: The Effect of Corporate Tax Avoidance On The Cost of Bank LoansDocument70 paginiBeauty Is in The Eye of The Beholder: The Effect of Corporate Tax Avoidance On The Cost of Bank LoansSELFIARLYNJFÎncă nu există evaluări

- How Interest Rate Shocks Impact Credit SpreadsDocument33 paginiHow Interest Rate Shocks Impact Credit SpreadsjantaÎncă nu există evaluări

- The Psychological Cost of Debt: Evidence from Housing Mortgages in PakistanDocument47 paginiThe Psychological Cost of Debt: Evidence from Housing Mortgages in PakistanMuhammad IlyasÎncă nu există evaluări

- Trade Credit, Cash Holdings, and Financial DeepeningDocument16 paginiTrade Credit, Cash Holdings, and Financial Deepeningangelcomputer2Încă nu există evaluări

- Are Public Firms in Argentina Credit Restricted?Document25 paginiAre Public Firms in Argentina Credit Restricted?Darío López ZadicoffÎncă nu există evaluări

- Thesis Credit Rating AgenciesDocument4 paginiThesis Credit Rating AgenciesWhoCanWriteMyPaperForMeUK100% (2)

- Home Loan Application Stages and HDFC ProcessingDocument60 paginiHome Loan Application Stages and HDFC Processingranup_2007Încă nu există evaluări

- Discussion Paper On Credit Information SharingDocument19 paginiDiscussion Paper On Credit Information SharingChuka SHÎncă nu există evaluări

- Sp03gu01 PDFDocument27 paginiSp03gu01 PDFBhatacherjee AnvieÎncă nu există evaluări

- How Unconscious Bias Impacts Accounting AuditsDocument7 paginiHow Unconscious Bias Impacts Accounting AuditsYoulah Mae Ybañez-PactolÎncă nu există evaluări

- The Impact of Credit Cards on Spending: A Field ExperimentDocument28 paginiThe Impact of Credit Cards on Spending: A Field ExperimentJogini LethwalaÎncă nu există evaluări

- HDQ 869Document12 paginiHDQ 869Ayoniseh CarolÎncă nu există evaluări

- SSRN Id3467316Document45 paginiSSRN Id3467316Gwyneth Mae GallardoÎncă nu există evaluări

- Informal Sector and Economic Growth: The Supply of Credit ChannelDocument24 paginiInformal Sector and Economic Growth: The Supply of Credit ChannelPride Tutorials Manikbagh RoadÎncă nu există evaluări

- wp2007 23Document74 paginiwp2007 23TBP_Think_TankÎncă nu există evaluări

- When Words SweatDocument83 paginiWhen Words SweatExacapeÎncă nu există evaluări

- Mortgage DissertationDocument8 paginiMortgage DissertationCollegePapersForSaleCanada100% (1)

- The Journal of Finance - 2016 - GURUN - Advertising Expensive MortgagesDocument46 paginiThe Journal of Finance - 2016 - GURUN - Advertising Expensive MortgagesHuijiezÎncă nu există evaluări

- Determinants of Lending Behaviour of Commercial BanksDocument3 paginiDeterminants of Lending Behaviour of Commercial BanksMichelle MilanesÎncă nu există evaluări

- Credit Line Usage, Checking Account Activity, and Default Risk of Bank BorrowersDocument52 paginiCredit Line Usage, Checking Account Activity, and Default Risk of Bank BorrowersSarah LebaÎncă nu există evaluări

- Repayment: 3.1 Empirical EvidenceDocument6 paginiRepayment: 3.1 Empirical EvidenceSohil DhruvÎncă nu există evaluări

- Where Does It Go? Spending by The Financially ConstrainedDocument40 paginiWhere Does It Go? Spending by The Financially ConstrainedHaFfiza IezaÎncă nu există evaluări

- Payday Loan Customers Analyzed to Guide PolicymakersDocument18 paginiPayday Loan Customers Analyzed to Guide PolicymakersChinCeleryÎncă nu există evaluări

- Paper 3Document14 paginiPaper 3arathirockingstarÎncă nu există evaluări

- Borrower Risk and The Price and Nonprice Terms of Bank LoansDocument37 paginiBorrower Risk and The Price and Nonprice Terms of Bank LoansAtaul HoqueÎncă nu există evaluări

- Using Repayment Data To Test Across Models of Joint Liability LendingDocument41 paginiUsing Repayment Data To Test Across Models of Joint Liability LendingrollinpeguyÎncă nu există evaluări

- Credit Card Debt and Payment Use: Charles Sprenger and Joanna StavinsDocument29 paginiCredit Card Debt and Payment Use: Charles Sprenger and Joanna StavinsAbhijeet BoseÎncă nu există evaluări

- Peter Klibowitz Masters 10Document41 paginiPeter Klibowitz Masters 10api-91993977Încă nu există evaluări

- ProQuestDocuments 2022 09 07Document17 paginiProQuestDocuments 2022 09 07Fathi HaidarÎncă nu există evaluări

- Sunderam Money Creation and The SBSDocument51 paginiSunderam Money Creation and The SBSMariano Cruz NavarroÎncă nu există evaluări

- Financial Distress and Relationship Bankpap Jan7 2002Document42 paginiFinancial Distress and Relationship Bankpap Jan7 2002osvaldcobo9493Încă nu există evaluări

- Trade Credit and ShortDocument14 paginiTrade Credit and ShortRajkumar KandasamyÎncă nu există evaluări

- Do Measures of Financial Constraints Measure Financial ConstraintsDocument56 paginiDo Measures of Financial Constraints Measure Financial ConstraintsvinibarcelosÎncă nu există evaluări

- Credit Scores and Loan Portfolio Risk in Small Banks: Don't Quote Without The Permission of The AuthorDocument14 paginiCredit Scores and Loan Portfolio Risk in Small Banks: Don't Quote Without The Permission of The Authorits4krishna3776Încă nu există evaluări

- Machine Learning Models Forecast Bond PricesDocument17 paginiMachine Learning Models Forecast Bond PricesVichara PoolsÎncă nu există evaluări

- Deter Min An Lending PredictionDocument32 paginiDeter Min An Lending PredictionLumphia SemarangÎncă nu există evaluări

- Brso97lm PDFDocument14 paginiBrso97lm PDFAyoub BelgachaÎncă nu există evaluări

- RG JADEJA Literature ReviewDocument7 paginiRG JADEJA Literature ReviewJadeja AjayrajsinhÎncă nu există evaluări

- Measure Quality Credit Scoring Models Using Indices Like Gini, KS, LiftDocument22 paginiMeasure Quality Credit Scoring Models Using Indices Like Gini, KS, LiftAfeezÎncă nu există evaluări

- Credit Rationing in Developing Countries:: An Overview of The TheoryDocument24 paginiCredit Rationing in Developing Countries:: An Overview of The TheorymitalptÎncă nu există evaluări

- JPM Q3 EarningsDocument25 paginiJPM Q3 EarningsZerohedgeÎncă nu există evaluări

- People V JP Morgan ComplaintDocument31 paginiPeople V JP Morgan ComplaintJames EdwardsÎncă nu există evaluări

- Single SlideDocument1 paginăSingle Slideannawitkowski88Încă nu există evaluări

- SSRN Id2023011Document54 paginiSSRN Id2023011sterkejanÎncă nu există evaluări

- OCT7BRDocument2 paginiOCT7BRannawitkowski88Încă nu există evaluări

- Research Division: Federal Reserve Bank of St. LouisDocument43 paginiResearch Division: Federal Reserve Bank of St. Louisannawitkowski88Încă nu există evaluări

- OSAM TheBigPicture 150ppi Arial-JPOS EditDocument28 paginiOSAM TheBigPicture 150ppi Arial-JPOS Editannawitkowski88Încă nu există evaluări

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 paginiExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Încă nu există evaluări

- TBP Conf Oct 2012Document27 paginiTBP Conf Oct 2012annawitkowski88Încă nu există evaluări

- Navigating The New Normal David A. RosenbergDocument73 paginiNavigating The New Normal David A. Rosenbergannawitkowski88Încă nu există evaluări

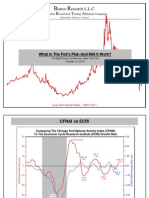

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Document44 paginiIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88Încă nu există evaluări

- Gurtin Fixed Income Presentation - TBP Conference - 10.4.12Document16 paginiGurtin Fixed Income Presentation - TBP Conference - 10.4.12annawitkowski88Încă nu există evaluări

- Exhibit 2 - Whistleblower Transcript (Redacted)Document56 paginiExhibit 2 - Whistleblower Transcript (Redacted)annawitkowski88Încă nu există evaluări

- MBIA Vs Countrywide - Schedule Summary Judgement For Primary Liability Hearing On Nov 14th and 15th, 2012Document4 paginiMBIA Vs Countrywide - Schedule Summary Judgement For Primary Liability Hearing On Nov 14th and 15th, 2012annawitkowski88Încă nu există evaluări

- Taxes and The EconomyDocument23 paginiTaxes and The Economychristian_trejbal100% (1)

- Top 1 PercentDocument1 paginăTop 1 Percentannawitkowski88Încă nu există evaluări

- Bartlett Laffer 2Document3 paginiBartlett Laffer 2annawitkowski88Încă nu există evaluări

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 paginiExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Încă nu există evaluări

- The Laffer Curve, Part 1 (7!16!12)Document3 paginiThe Laffer Curve, Part 1 (7!16!12)annawitkowski88Încă nu există evaluări

- KPMG Pcaob 2012Document31 paginiKPMG Pcaob 2012Caleb NewquistÎncă nu există evaluări

- Fed SideDocument1 paginăFed Sideannawitkowski88Încă nu există evaluări

- Federal ReserveDocument5 paginiFederal Reserveannawitkowski88Încă nu există evaluări

- Friction and Housing Market DynamicsDocument52 paginiFriction and Housing Market DynamicsLori NobleÎncă nu există evaluări

- Taxes and The EconomyDocument23 paginiTaxes and The Economychristian_trejbal100% (1)

- FHFA OIG Report On Freddie MacDocument21 paginiFHFA OIG Report On Freddie MacForeclosure FraudÎncă nu există evaluări

- Policy Insight 63Document13 paginiPolicy Insight 63annawitkowski88Încă nu există evaluări

- Fed SideDocument1 paginăFed Sideannawitkowski88Încă nu există evaluări

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 paginiIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Încă nu există evaluări

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 paginiIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Încă nu există evaluări

- Loan Modification Program InfoDocument3 paginiLoan Modification Program InfoDeborah Tarpley HicksÎncă nu există evaluări

- Pay GuideDocument2 paginiPay GuideWilliam Walter0% (1)

- Model Bank: SWIFT Message SupportDocument26 paginiModel Bank: SWIFT Message Supportigomez100% (1)

- Banking Systems in India: S.P.Mohanty Assistant General Manager Reserve Bank of India BhubaneswarDocument22 paginiBanking Systems in India: S.P.Mohanty Assistant General Manager Reserve Bank of India BhubaneswarSanjay ParidaÎncă nu există evaluări

- Statement I: Standard Presentation of India's Balance of Payments As Per BPM6Document28 paginiStatement I: Standard Presentation of India's Balance of Payments As Per BPM6Priyanka PanigrahiÎncă nu există evaluări

- Ba 55293Document10 paginiBa 55293Abdu MohammedÎncă nu există evaluări

- Revision Banking QDocument15 paginiRevision Banking QThảo Hương PhạmÎncă nu există evaluări

- TermsDocument2 paginiTermsapi-239504098Încă nu există evaluări

- YMCA Guest WaiverDocument1 paginăYMCA Guest Waiverdesertbutterfly78100% (1)

- Company status and contact detailsDocument5 paginiCompany status and contact detailsshriya shettiwarÎncă nu există evaluări

- Chapter Two The Financial System2 - Eco551Document25 paginiChapter Two The Financial System2 - Eco551Hafiz akbarÎncă nu există evaluări

- Pefindo Beta Saham Edition October 24 2013Document12 paginiPefindo Beta Saham Edition October 24 2013Fendy ArzunataÎncă nu există evaluări

- Extra 2020 PDFDocument283 paginiExtra 2020 PDFshivankar shuklaÎncă nu există evaluări

- Exam Financial ManagementDocument10 paginiExam Financial ManagementShrief MohiÎncă nu există evaluări

- Ar Rajeshexpo 2009 2010 15092010120000Document276 paginiAr Rajeshexpo 2009 2010 15092010120000Jupe JonesÎncă nu există evaluări

- Tax Invoice: MR Tarun MR TarunDocument1 paginăTax Invoice: MR Tarun MR Taruntarun kaushalÎncă nu există evaluări

- LPMPC Products and Services - Part 1 - As of Octob 3Document8 paginiLPMPC Products and Services - Part 1 - As of Octob 3phoebekayleonaÎncă nu există evaluări

- Government of Malaysia V Government of The SDocument13 paginiGovernment of Malaysia V Government of The SSara Azhari100% (1)

- NDocument43 paginiNapi-256139910Încă nu există evaluări

- ECS Form PDFDocument1 paginăECS Form PDFbharatstar100% (1)

- Municipality of Alaminos, Laguna: GeographyDocument5 paginiMunicipality of Alaminos, Laguna: GeographyadrianÎncă nu există evaluări

- TD Discount Brokerage BrochureDocument17 paginiTD Discount Brokerage BrochureKayne JustineÎncă nu există evaluări

- Registration - Renewal of Tutorial or Coaching Institutions Application FormDocument3 paginiRegistration - Renewal of Tutorial or Coaching Institutions Application FormSTANDARD EDUCATION ACADEMY M.E.P CENTERÎncă nu există evaluări

- CHAPTER 5 Corporate GovernanceDocument5 paginiCHAPTER 5 Corporate Governancesyafira100% (1)

- United States Court of Appeals, First CircuitDocument8 paginiUnited States Court of Appeals, First CircuitScribd Government DocsÎncă nu există evaluări

- Bank ADocument3 paginiBank ASARY MISHEL NUÑEZ ACEVEDOÎncă nu există evaluări

- Role of Investment Banks in Economic DevelopmentDocument6 paginiRole of Investment Banks in Economic DevelopmentChirag BoraÎncă nu există evaluări

- Statement Emilija BarclaysDocument4 paginiStatement Emilija BarclaysKris TheVillainÎncă nu există evaluări

- Eugenicsandpandemics - Wordpress.2016!11!23.002 - EditorDocument8.302 paginiEugenicsandpandemics - Wordpress.2016!11!23.002 - EditorsligomcÎncă nu există evaluări

- Strategic Analysis and Strategic Planning For Commercial Banking An Analysis Based A Commercial Bank Operating in Sri Lanka 2162 6359 1000418 PDFDocument11 paginiStrategic Analysis and Strategic Planning For Commercial Banking An Analysis Based A Commercial Bank Operating in Sri Lanka 2162 6359 1000418 PDFbarthipamaruthuÎncă nu există evaluări

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsDe la EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsEvaluare: 4.5 din 5 stele4.5/5 (94)

- How an Economy Grows and Why It Crashes: Collector's EditionDe la EverandHow an Economy Grows and Why It Crashes: Collector's EditionEvaluare: 4.5 din 5 stele4.5/5 (102)

- Look Again: The Power of Noticing What Was Always ThereDe la EverandLook Again: The Power of Noticing What Was Always ThereEvaluare: 5 din 5 stele5/5 (3)

- When Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfDe la EverandWhen Helping Hurts: How to Alleviate Poverty Without Hurting the Poor . . . and YourselfEvaluare: 5 din 5 stele5/5 (36)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesDe la EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesEvaluare: 4.5 din 5 stele4.5/5 (8)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaDe la EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaÎncă nu există evaluări

- Chip War: The Quest to Dominate the World's Most Critical TechnologyDe la EverandChip War: The Quest to Dominate the World's Most Critical TechnologyEvaluare: 4.5 din 5 stele4.5/5 (227)

- Workin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherDe la EverandWorkin' Our Way Home: The Incredible True Story of a Homeless Ex-Con and a Grieving Millionaire Thrown Together to Save Each OtherÎncă nu există evaluări

- High-Risers: Cabrini-Green and the Fate of American Public HousingDe la EverandHigh-Risers: Cabrini-Green and the Fate of American Public HousingÎncă nu există evaluări

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentDe la EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentEvaluare: 4.5 din 5 stele4.5/5 (92)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationDe la EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationEvaluare: 4.5 din 5 stele4.5/5 (46)

- The Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldDe la EverandThe Genius of Israel: The Surprising Resilience of a Divided Nation in a Turbulent WorldEvaluare: 4 din 5 stele4/5 (16)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDe la EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingEvaluare: 4.5 din 5 stele4.5/5 (97)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomDe la EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomÎncă nu există evaluări

- Second Class: How the Elites Betrayed America's Working Men and WomenDe la EverandSecond Class: How the Elites Betrayed America's Working Men and WomenÎncă nu există evaluări

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDe la EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassÎncă nu există evaluări

- Against the Gods: The Remarkable Story of RiskDe la EverandAgainst the Gods: The Remarkable Story of RiskEvaluare: 4 din 5 stele4/5 (352)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetDe la EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetÎncă nu există evaluări

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsDe la EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsEvaluare: 5 din 5 stele5/5 (2)

- The New Elite: Inside the Minds of the Truly WealthyDe la EverandThe New Elite: Inside the Minds of the Truly WealthyEvaluare: 4 din 5 stele4/5 (10)

- Kaizen: The Ultimate Guide to Mastering Continuous Improvement And Transforming Your Life With Self DisciplineDe la EverandKaizen: The Ultimate Guide to Mastering Continuous Improvement And Transforming Your Life With Self DisciplineEvaluare: 4.5 din 5 stele4.5/5 (36)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailDe la EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailEvaluare: 4.5 din 5 stele4.5/5 (237)

- Hillbilly Elegy: A Memoir of a Family and Culture in CrisisDe la EverandHillbilly Elegy: A Memoir of a Family and Culture in CrisisEvaluare: 4 din 5 stele4/5 (4276)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyDe la EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyEvaluare: 4.5 din 5 stele4.5/5 (263)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)