S-ar putea să vă placă și

- Accnts 2021-22Document24 paginiAccnts 2021-22Hari RamÎncă nu există evaluări

- Accounting NotesDocument66 paginiAccounting NotesShashank Gadia71% (17)

- Basic Acc QuesDocument10 paginiBasic Acc QuesAli IqbalÎncă nu există evaluări

- What Are The Different Types of Subsidiary Books Usually Maintained by A Firm?Document11 paginiWhat Are The Different Types of Subsidiary Books Usually Maintained by A Firm?sweet19girlÎncă nu există evaluări

- Accounting AssignmentDocument22 paginiAccounting AssignmentEveryday LearnÎncă nu există evaluări

- Angelina - Kwofie - 301121003 Buac-171Document7 paginiAngelina - Kwofie - 301121003 Buac-171Yano NettleÎncă nu există evaluări

- Chapter6 - Trial balance and Preparation of Final Accounts яDocument13 paginiChapter6 - Trial balance and Preparation of Final Accounts яshreya taluja100% (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?De la EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Evaluare: 5 din 5 stele5/5 (1)

- Chapter 4 AccountingDocument22 paginiChapter 4 AccountingChan Man SeongÎncă nu există evaluări

- JournalDocument9 paginiJournalchippÎncă nu există evaluări

- InventoryDocument9 paginiInventorychippÎncă nu există evaluări

- Accounting Interview QuestionsDocument43 paginiAccounting Interview QuestionsArif ullahÎncă nu există evaluări

- Management Accounting Jargons/ Key TerminologiesDocument11 paginiManagement Accounting Jargons/ Key Terminologiesnimbus2050Încă nu există evaluări

- General-Journals and LedgersDocument13 paginiGeneral-Journals and LedgersRaviSankarÎncă nu există evaluări

- Basics of Cost AccountingDocument21 paginiBasics of Cost AccountingRose DallyÎncă nu există evaluări

- The BeginnerDocument4 paginiThe BeginnerSyra CeladaÎncă nu există evaluări

- Powerpoint Journal Ledger and Trial BalanceDocument40 paginiPowerpoint Journal Ledger and Trial BalanceChris Iero-Way100% (1)

- Interview Question of AccountingDocument6 paginiInterview Question of AccountingSahana GÎncă nu există evaluări

- Chapter: 1 Meaning, Objectives and Basic Accounting TermsDocument19 paginiChapter: 1 Meaning, Objectives and Basic Accounting TermsGudlipÎncă nu există evaluări

- Accounting Terms - Basic DefinitionsDocument7 paginiAccounting Terms - Basic DefinitionsSourav JaiswalÎncă nu există evaluări

- All Basic Terms of AccountingDocument20 paginiAll Basic Terms of AccountingpoornapavanÎncă nu există evaluări

- Break-Even Point:c: CC CC CCCCCCCCC CCC CCCCCCCCC C C CCC C CCCC CCCCC C CCCCC CCCCCCCCC C CCCDocument8 paginiBreak-Even Point:c: CC CC CCCCCCCCC CCC CCCCCCCCC C C CCC C CCCC CCCCC C CCCCC CCCCCCCCC C CCCchanduanu2007Încă nu există evaluări

- What Is Debit Note and Credit Note? What Is The Difference Between Them?Document5 paginiWhat Is Debit Note and Credit Note? What Is The Difference Between Them?Zakariya ThoubaÎncă nu există evaluări

- Mba Faaunit - IIDocument15 paginiMba Faaunit - IINaresh GuduruÎncă nu există evaluări

- Glossary of Accounting TermsDocument8 paginiGlossary of Accounting TermsFauTahudAmparoÎncă nu există evaluări

- Lesson 1: Basics of AccountingDocument8 paginiLesson 1: Basics of AccountingkharemixÎncă nu există evaluări

- Trial Balance & Accounting ConceptsDocument32 paginiTrial Balance & Accounting ConceptsPaul Ayoma100% (1)

- Financial Accounting & AnalysisDocument11 paginiFinancial Accounting & Analysisheet jainÎncă nu există evaluări

- Safari - 7 Jul 2022 at 3:41 PMDocument1 paginăSafari - 7 Jul 2022 at 3:41 PMKristy Veyna BautistaÎncă nu există evaluări

- Financial Accounting (Mgt-101) VUDocument311 paginiFinancial Accounting (Mgt-101) VUgoriÎncă nu există evaluări

- Shivam Pandey Accounts Assignment No. 2Document8 paginiShivam Pandey Accounts Assignment No. 2Madhaw ShuklaÎncă nu există evaluări

- Accounting Equation and Business TransactionsDocument5 paginiAccounting Equation and Business TransactionsJoseph OndariÎncă nu există evaluări

- Bookkeeping Module 1Document11 paginiBookkeeping Module 1Cindy TorresÎncă nu există evaluări

- Fa Unit 2Document28 paginiFa Unit 2VTÎncă nu există evaluări

- Tally ERP 9 - TutorialDocument1.192 paginiTally ERP 9 - TutorialChandan Mundhra85% (68)

- Tally ERP 9.0 Material Basics of Accounting 01Document10 paginiTally ERP 9.0 Material Basics of Accounting 01Raghavendra yadav KM100% (1)

- Bookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthDe la EverandBookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthÎncă nu există evaluări

- Dip Fin TallyDocument73 paginiDip Fin Tallyceasor007100% (1)

- Accounting BasicsDocument30 paginiAccounting BasicsAsciel Hizon MorcoÎncă nu există evaluări

- Accounting Interview Questions: What Is Minority Interest?Document16 paginiAccounting Interview Questions: What Is Minority Interest?vemula_ramakoti94840% (1)

- QuesDocument4 paginiQuesSreejith NairÎncă nu există evaluări

- Chapter 7: Business Accounting: What Are Accounts and Why Are They Necessary?Document8 paginiChapter 7: Business Accounting: What Are Accounts and Why Are They Necessary?Web BooksÎncă nu există evaluări

- The Essentials of Accounting BasicsDocument21 paginiThe Essentials of Accounting Basicsbarber bobÎncă nu există evaluări

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyDe la EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyÎncă nu există evaluări

- Accounting CycleDocument4 paginiAccounting Cycleddoc.mimiÎncă nu există evaluări

- Wiley Notes Chapter 2Document7 paginiWiley Notes Chapter 2hasanÎncă nu există evaluări

- Assignment 03Document9 paginiAssignment 03duhkhabilasa4Încă nu există evaluări

- Unit-5 of Accounting For ManagerDocument70 paginiUnit-5 of Accounting For Managerklrahulprasad112Încă nu există evaluări

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursDe la EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursÎncă nu există evaluări

- Bookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)De la EverandBookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)Încă nu există evaluări

- Summary of Tycho Press's Accounting for Small Business OwnersDe la EverandSummary of Tycho Press's Accounting for Small Business OwnersÎncă nu există evaluări

- Summary of Richard A. Lambert's Financial Literacy for ManagersDe la EverandSummary of Richard A. Lambert's Financial Literacy for ManagersÎncă nu există evaluări

- Teeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!De la EverandTeeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Evaluare: 2 din 5 stele2/5 (1)

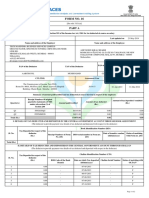

- Form No. 16A: From ToDocument2 paginiForm No. 16A: From ToRomendro ThokchomÎncă nu există evaluări

- FGHFDocument4 paginiFGHFRomendro ThokchomÎncă nu există evaluări

- PMEGP GuidelinesDocument23 paginiPMEGP Guidelinesshreeshlko100% (1)

- 1 Ma (MC&JR)Document13 pagini1 Ma (MC&JR)Romendro ThokchomÎncă nu există evaluări

- 1 Ma (MC&JR)Document13 pagini1 Ma (MC&JR)Romendro ThokchomÎncă nu există evaluări

- Name-Himadri Debnath No:: ResumeDocument3 paginiName-Himadri Debnath No:: ResumeRomendro ThokchomÎncă nu există evaluări

- Qualified Written RequestDocument2 paginiQualified Written Request3rdforceent100% (1)

- Investment & Risk ManagementDocument5 paginiInvestment & Risk ManagementE-sabat RizviÎncă nu există evaluări

- Form No. 16: Part ADocument2 paginiForm No. 16: Part AasifÎncă nu există evaluări

- Act No 1120 Friar ActDocument7 paginiAct No 1120 Friar ActWuwu WuswewuÎncă nu există evaluări

- Accounting Basics Word Scramble QuestionsDocument1 paginăAccounting Basics Word Scramble Questionsthorat82Încă nu există evaluări

- IFRS IAS SummaryDocument9 paginiIFRS IAS SummaryLin AungÎncă nu există evaluări

- Personal Property Security Act V. Chattel Mortgage Chattel Mortgage (NCC ACT 1508) PPSA (R.A. 11057)Document8 paginiPersonal Property Security Act V. Chattel Mortgage Chattel Mortgage (NCC ACT 1508) PPSA (R.A. 11057)Jj JumalonÎncă nu există evaluări

- Banking Law QuizDocument18 paginiBanking Law QuizJui Aquino Provido100% (1)

- حوالاتDocument16 paginiحوالاتnehadÎncă nu există evaluări

- BCE: INC Case AnalysisDocument6 paginiBCE: INC Case AnalysisShuja Ur RahmanÎncă nu există evaluări

- 360 Global Wine Company TSIXQDocument5 pagini360 Global Wine Company TSIXQsoulpatch_85Încă nu există evaluări

- Financial Ratio Analysis of HealthsouthDocument11 paginiFinancial Ratio Analysis of Healthsouthfarha tabassumÎncă nu există evaluări

- Federal Bank - Retail Banking - AccountsDocument77 paginiFederal Bank - Retail Banking - AccountsAditya SinghÎncă nu există evaluări

- Account Executive / Sales Resume SampleDocument2 paginiAccount Executive / Sales Resume Sampleresume7.com100% (1)

- Sample Letter - Explanation For Delinquent PaymentDocument2 paginiSample Letter - Explanation For Delinquent PaymentJ Stocker100% (2)

- General AnnuityDocument22 paginiGeneral AnnuityJomel RositaÎncă nu există evaluări

- Cemap 3 Full TextDocument208 paginiCemap 3 Full TextIain100% (1)

- A Research Project On Impact of FII: On Money MarketDocument9 paginiA Research Project On Impact of FII: On Money Marketsamruddhi_khaleÎncă nu există evaluări

- Szymoniak False Claims Act Complaint - SCDocument74 paginiSzymoniak False Claims Act Complaint - SCMartin Andelman100% (2)

- CONDOMINIUM NOTES Atty. DomingoDocument2 paginiCONDOMINIUM NOTES Atty. Domingothalia alfaroÎncă nu există evaluări

- Income and Business TaxationDocument6 paginiIncome and Business Taxationomega shtÎncă nu există evaluări

- New York Lottery Winners' HandbookDocument10 paginiNew York Lottery Winners' HandbookCara Matthews100% (1)

- The Secret Trading Strategy From The 1930s That Hedge Funders DoneDocument7 paginiThe Secret Trading Strategy From The 1930s That Hedge Funders DoneivopiskovÎncă nu există evaluări

- CIMA F1 2019 NotesDocument164 paginiCIMA F1 2019 Notessolstice567567Încă nu există evaluări

- St. Lukes Case DIgest TAxDocument3 paginiSt. Lukes Case DIgest TAxKayee KatÎncă nu există evaluări

- United Paragon Mining Corporation SEC 17 Q June302020Document51 paginiUnited Paragon Mining Corporation SEC 17 Q June302020Jon DonÎncă nu există evaluări

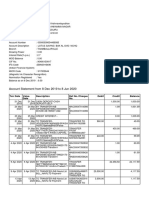

- Account Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 paginiAccount Statement From 8 Dec 2019 To 8 Jun 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMUTHYALA NEERAJAÎncă nu există evaluări

- PARTNERSHIPDocument10 paginiPARTNERSHIPArvin John MasuelaÎncă nu există evaluări

- Joint Venture 1Document11 paginiJoint Venture 1Clif Mj Jr.100% (4)

- 2008 Financial Crisis Subprime Mortgage Crisis Caused by The Unregulated Use of Derivatives U.S. Treasury Federal Reserve Economic CollapseDocument4 pagini2008 Financial Crisis Subprime Mortgage Crisis Caused by The Unregulated Use of Derivatives U.S. Treasury Federal Reserve Economic CollapseShane TabunggaoÎncă nu există evaluări