S-ar putea să vă placă și

- Complete Report White Collar CrimeDocument11 paginiComplete Report White Collar CrimeZul Aizat HamdanÎncă nu există evaluări

- Review hadiths relating to Islamic business ethics and economicsDocument8 paginiReview hadiths relating to Islamic business ethics and economicsZul Aizat HamdanÎncă nu există evaluări

- EXAMPLEDocument2 paginiEXAMPLEZul Aizat HamdanÎncă nu există evaluări

- Jan: Feb: Mar: Apr: May: Jun: Jul: Aug: Sep: Oct: Nov: DecDocument1 paginăJan: Feb: Mar: Apr: May: Jun: Jul: Aug: Sep: Oct: Nov: DecZul Aizat HamdanÎncă nu există evaluări

- Review hadiths relating to Islamic business ethics and economicsDocument8 paginiReview hadiths relating to Islamic business ethics and economicsZul Aizat HamdanÎncă nu există evaluări

- Information ViewDocument1 paginăInformation ViewZul Aizat HamdanÎncă nu există evaluări

- Maybank DataDocument6 paginiMaybank DataZul Aizat HamdanÎncă nu există evaluări

- Please Choose at Least 3 Cluster For Each CourseDocument11 paginiPlease Choose at Least 3 Cluster For Each CourseZul Aizat HamdanÎncă nu există evaluări

- MAYBANK and CIMB FactorDocument6 paginiMAYBANK and CIMB FactorZul Aizat HamdanÎncă nu există evaluări

- Company Memorandum Packet 4Document4 paginiCompany Memorandum Packet 4Zul Aizat HamdanÎncă nu există evaluări

- Cimb DataDocument6 paginiCimb DataZul Aizat HamdanÎncă nu există evaluări

- TAHAP CELIK KEWANGAN DALAM KALANGAN PELAJAR POLITEKNIK: POLITEKNIK NILAI (Responses) PDFDocument1 paginăTAHAP CELIK KEWANGAN DALAM KALANGAN PELAJAR POLITEKNIK: POLITEKNIK NILAI (Responses) PDFZul Aizat HamdanÎncă nu există evaluări

- MAYBANK and CIMB Factor LATESTDocument11 paginiMAYBANK and CIMB Factor LATESTZul Aizat HamdanÎncă nu există evaluări

- Group soccer tournament scheduleDocument16 paginiGroup soccer tournament scheduleZul Aizat HamdanÎncă nu există evaluări

- Operational RiskDocument10 paginiOperational RiskZul Aizat HamdanÎncă nu există evaluări

- Review hadiths relating to Islamic business ethics and economicsDocument8 paginiReview hadiths relating to Islamic business ethics and economicsZul Aizat HamdanÎncă nu există evaluări

- List of SourcesDocument1 paginăList of SourcesZul Aizat HamdanÎncă nu există evaluări

- TAHAP CELIK KEWANGAN DALAM KALANGAN PELAJAR POLITEKNIK: POLITEKNIK NILAI (Responses) PDFDocument1 paginăTAHAP CELIK KEWANGAN DALAM KALANGAN PELAJAR POLITEKNIK: POLITEKNIK NILAI (Responses) PDFZul Aizat HamdanÎncă nu există evaluări

- 1 - Introduction To Islamic EconomicDocument35 pagini1 - Introduction To Islamic EconomicZul Aizat HamdanÎncă nu există evaluări

- All About IjaraDocument3 paginiAll About IjaraZul Aizat HamdanÎncă nu există evaluări

- Micro EnterprisesDocument3 paginiMicro EnterprisesZul Aizat HamdanÎncă nu există evaluări

- Islamic Banking Operation-DepositDocument24 paginiIslamic Banking Operation-DepositZul Aizat HamdanÎncă nu există evaluări

- Ijara-Based Financing: Definition of Ijara (Leasing)Document13 paginiIjara-Based Financing: Definition of Ijara (Leasing)Nura HaikuÎncă nu există evaluări

- Review hadiths relating to Islamic business ethics and economicsDocument8 paginiReview hadiths relating to Islamic business ethics and economicsZul Aizat HamdanÎncă nu există evaluări

- Project Group 1 EthicsDocument2 paginiProject Group 1 EthicsZul Aizat HamdanÎncă nu există evaluări

- Project Group 1 EthicsDocument2 paginiProject Group 1 EthicsZul Aizat HamdanÎncă nu există evaluări

- 3.2: Credit AssessmentDocument1 pagină3.2: Credit AssessmentZul Aizat HamdanÎncă nu există evaluări

- 3.2: Credit AssessmentDocument1 pagină3.2: Credit AssessmentZul Aizat HamdanÎncă nu există evaluări

- Chapter 3.2Document5 paginiChapter 3.2Zul Aizat HamdanÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Cesu BillDocument1 paginăCesu BillPunyesh KumarÎncă nu există evaluări

- Trade Online Introduction To Trade OnlineDocument7 paginiTrade Online Introduction To Trade Onlinesales MPÎncă nu există evaluări

- View Certificate PDFDocument1 paginăView Certificate PDFRaj Kumar GuleriaÎncă nu există evaluări

- International Bankers: Robber Barons?Document209 paginiInternational Bankers: Robber Barons?William Litynski100% (4)

- Outline of the Conventional Banking System and Central Bank FunctionsDocument5 paginiOutline of the Conventional Banking System and Central Bank FunctionsMohamed YazÎncă nu există evaluări

- Cash and Cash Equivalents Sample ProblemDocument8 paginiCash and Cash Equivalents Sample ProblemAllana MierÎncă nu există evaluări

- Aug To NovDocument4 paginiAug To NovRuchir OzaÎncă nu există evaluări

- LT Bill 33000441667 202003Document3 paginiLT Bill 33000441667 202003Kuchh BhiÎncă nu există evaluări

- Final Project Banking LawDocument17 paginiFinal Project Banking Lawrupali jani100% (1)

- Mr. Vikas Kumar's bank statement from Nov 2019Document2 paginiMr. Vikas Kumar's bank statement from Nov 2019vikas kumarÎncă nu există evaluări

- Banking Law B.com - Docx LatestDocument38 paginiBanking Law B.com - Docx LatestViraja GuruÎncă nu există evaluări

- Kotak Bank Statement Nov2023Document9 paginiKotak Bank Statement Nov2023peak10officialÎncă nu există evaluări

- Audit of Cash and Marketable SecuritiesDocument21 paginiAudit of Cash and Marketable Securitiesዝምታ ተሻለÎncă nu există evaluări

- Musharakah FinancingDocument23 paginiMusharakah FinancingTayyaba TariqÎncă nu există evaluări

- Icici - Apf LettersDocument2 paginiIcici - Apf LettersprabhudanielcÎncă nu există evaluări

- ECourt Digitalisasi Peradilan IndonesiaDocument30 paginiECourt Digitalisasi Peradilan IndonesiaMuhammad Raja mnÎncă nu există evaluări

- Which of The Following Does The Discount Rate RDocument5 paginiWhich of The Following Does The Discount Rate RNajmul IslamÎncă nu există evaluări

- Audit of Cash and Cash Equivalents Internal ControlsDocument7 paginiAudit of Cash and Cash Equivalents Internal ControlsRÎncă nu există evaluări

- Dishonour of Negotiable Instruments ExplainedDocument10 paginiDishonour of Negotiable Instruments ExplainedHyderÎncă nu există evaluări

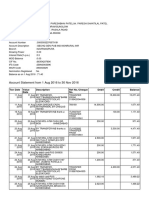

- Account Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 paginiAccount Statement From 4 Jan 2024 To 23 Jan 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancerangaswamy8194Încă nu există evaluări

- New Product DevelopmentDocument20 paginiNew Product DevelopmentAbhinav SachdevaÎncă nu există evaluări

- NCS PlusDocument3 paginiNCS PlusncsplusinccoÎncă nu există evaluări

- RTGS FUNDS TRANSFER APPLICATION FORMDocument1 paginăRTGS FUNDS TRANSFER APPLICATION FORMShadabAhmedÎncă nu există evaluări

- Research Report FinalDocument71 paginiResearch Report FinalParveen KumarÎncă nu există evaluări

- RHB Malaysian Employment Application FormDocument4 paginiRHB Malaysian Employment Application FormHawa Abu SamahÎncă nu există evaluări

- Tanzania Mortgage Market Update 2014Document7 paginiTanzania Mortgage Market Update 2014Anonymous FnM14a0Încă nu există evaluări

- DownloadDocument4 paginiDownloadSruthi RenganathÎncă nu există evaluări

- Operational DefinitionDocument6 paginiOperational DefinitionPaolo GubotÎncă nu există evaluări

- AXIS BANK Project Word FileDocument28 paginiAXIS BANK Project Word Fileअक्षय गोयलÎncă nu există evaluări

- (A) A Cheque Which Had Originally Been Crossed Is Presented To You For Payment at The Counter Bearing The Remark "Crossing Cancelled" Below The Crossing Under The Drawer's InitialsDocument10 pagini(A) A Cheque Which Had Originally Been Crossed Is Presented To You For Payment at The Counter Bearing The Remark "Crossing Cancelled" Below The Crossing Under The Drawer's InitialsSajid IslamÎncă nu există evaluări