S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Appendix To Appellant/Petitioner's Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Document47 paginiAppendix To Appellant/Petitioner's Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Chapter 11 DocketsÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Republic Late Filed Rejection Damages OpinionDocument13 paginiRepublic Late Filed Rejection Damages OpinionChapter 11 Dockets100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- SEC Vs MUSKDocument23 paginiSEC Vs MUSKZerohedge100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Appellant/Petitioner's Reply Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Document28 paginiAppellant/Petitioner's Reply Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Chapter 11 DocketsÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Appellees/Debtors' Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Document69 paginiAppellees/Debtors' Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Chapter 11 DocketsÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Wochos V Tesla OpinionDocument13 paginiWochos V Tesla OpinionChapter 11 DocketsÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Ultra Resources, Inc. Opinion Regarding Make Whole PremiumDocument22 paginiUltra Resources, Inc. Opinion Regarding Make Whole PremiumChapter 11 DocketsÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Roman Catholic Bishop of Great Falls MTDocument57 paginiRoman Catholic Bishop of Great Falls MTChapter 11 DocketsÎncă nu există evaluări

- Zohar 2017 ComplaintDocument84 paginiZohar 2017 ComplaintChapter 11 DocketsÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Appellant/Petitioner's Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Document38 paginiAppellant/Petitioner's Brief (In Re: Ocean Rig UDW Inc., Second Circuit Court of Appeals Case No. 18-1374)Chapter 11 DocketsÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- PopExpert PetitionDocument79 paginiPopExpert PetitionChapter 11 DocketsÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Quirky Auction NoticeDocument2 paginiQuirky Auction NoticeChapter 11 DocketsÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Energy Future Interest OpinionDocument38 paginiEnergy Future Interest OpinionChapter 11 DocketsÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- NQ Letter 1Document3 paginiNQ Letter 1Chapter 11 DocketsÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Kalobios Pharmaceuticals IncDocument81 paginiKalobios Pharmaceuticals IncChapter 11 DocketsÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- National Bank of Anguilla DeclDocument10 paginiNational Bank of Anguilla DeclChapter 11 DocketsÎncă nu există evaluări

- City Sports GIft Card Claim Priority OpinionDocument25 paginiCity Sports GIft Card Claim Priority OpinionChapter 11 DocketsÎncă nu există evaluări

- Home JoyDocument30 paginiHome JoyChapter 11 DocketsÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- NQ LetterDocument2 paginiNQ LetterChapter 11 DocketsÎncă nu există evaluări

- District of Delaware 'O " !' ' ' 1 1°, : American A Arel IncDocument5 paginiDistrict of Delaware 'O " !' ' ' 1 1°, : American A Arel IncChapter 11 DocketsÎncă nu există evaluări

- United States Bankruptcy Court Voluntary Petition: Southern District of TexasDocument4 paginiUnited States Bankruptcy Court Voluntary Petition: Southern District of TexasChapter 11 DocketsÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Zohar AnswerDocument18 paginiZohar AnswerChapter 11 DocketsÎncă nu există evaluări

- APP CredDocument7 paginiAPP CredChapter 11 DocketsÎncă nu există evaluări

- APP ResDocument7 paginiAPP ResChapter 11 DocketsÎncă nu există evaluări

- GT Advanced KEIP Denial OpinionDocument24 paginiGT Advanced KEIP Denial OpinionChapter 11 DocketsÎncă nu există evaluări

- Special Report On Retailer Creditor Recoveries in Large Chapter 11 CasesDocument1 paginăSpecial Report On Retailer Creditor Recoveries in Large Chapter 11 CasesChapter 11 DocketsÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Licking River Mining Employment OpinionDocument22 paginiLicking River Mining Employment OpinionChapter 11 DocketsÎncă nu există evaluări

- Fletcher Appeal of Disgorgement DenialDocument21 paginiFletcher Appeal of Disgorgement DenialChapter 11 DocketsÎncă nu există evaluări

- Farb PetitionDocument12 paginiFarb PetitionChapter 11 DocketsÎncă nu există evaluări

- Market Research WorksheetDocument7 paginiMarket Research WorksheetNabila Nailatus SakinaÎncă nu există evaluări

- 5945-Article Text-17391-1-10-20181019 PDFDocument32 pagini5945-Article Text-17391-1-10-20181019 PDFfk tubeÎncă nu există evaluări

- Maharashtra National Law University, Mumbai: Submitted By-Shobhit Shukla Date of Submission - 8 Submitted ToDocument6 paginiMaharashtra National Law University, Mumbai: Submitted By-Shobhit Shukla Date of Submission - 8 Submitted ToShobhit ShuklaÎncă nu există evaluări

- EprgDocument13 paginiEprgRajveer RathoreÎncă nu există evaluări

- NCR NegoSale Batch 15134 090522Document35 paginiNCR NegoSale Batch 15134 090522April Jay BederioÎncă nu există evaluări

- A Futures Contract Based On Brent Crude OilDocument4 paginiA Futures Contract Based On Brent Crude OilJean-Louis KouassiÎncă nu există evaluări

- Monthly Digest Dec 2013Document134 paginiMonthly Digest Dec 2013innvolÎncă nu există evaluări

- BMW Group Corporate GovernanceDocument23 paginiBMW Group Corporate GovernanceAmeya Dalal0% (1)

- MC SP Module 06 - Supply Planning Process DesignDocument44 paginiMC SP Module 06 - Supply Planning Process Designsamah sÎncă nu există evaluări

- e-RUPI - Digital Payment SolutionDocument4 paginie-RUPI - Digital Payment SolutionSWARNENDU DEYÎncă nu există evaluări

- Journal of Financial Economics: Progress PaperDocument17 paginiJournal of Financial Economics: Progress PapersaidÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Sugar Crisis in Egypt, 2016: Important InfoDocument3 paginiSugar Crisis in Egypt, 2016: Important InfoyoussraselimÎncă nu există evaluări

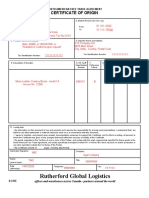

- Rutherford Global Logistics: Certificate of OriginDocument1 paginăRutherford Global Logistics: Certificate of OriginAnkita SinhaÎncă nu există evaluări

- Economic Incentive SystemsDocument23 paginiEconomic Incentive SystemsMark Arboleda GumamelaÎncă nu există evaluări

- Tawarruq PDFDocument20 paginiTawarruq PDFAbdifatah OsmanÎncă nu există evaluări

- Mohammed Ariful Islam Saimon Chowdhury: BankerDocument2 paginiMohammed Ariful Islam Saimon Chowdhury: BankerAriful SaimonÎncă nu există evaluări

- Financial Markets and Services NotesDocument94 paginiFinancial Markets and Services NotesShravan Richie100% (7)

- FX Risk ManagementDocument32 paginiFX Risk Managementapi-3755971100% (1)

- Shandong Longheng International Trade Co.,Ltd: Commercial InvoiceDocument2 paginiShandong Longheng International Trade Co.,Ltd: Commercial InvoiceJose LahozÎncă nu există evaluări

- Cryptocurrency and The Future of FinanceDocument9 paginiCryptocurrency and The Future of FinanceJawad NadeemÎncă nu există evaluări

- The History of The Philippine Currency: Republic Central CollegesDocument8 paginiThe History of The Philippine Currency: Republic Central CollegesDaishin Kingsley SeseÎncă nu există evaluări

- Faq On Kyc Aml PDFDocument4 paginiFaq On Kyc Aml PDFSiva KumarÎncă nu există evaluări

- Werlin (2003) Poor Nations, Rich Nations - A Theory of Governance PDFDocument14 paginiWerlin (2003) Poor Nations, Rich Nations - A Theory of Governance PDFlittleconspirator100% (1)

- Pilipinas Shell Petroleum Corporation: SHLPHDocument17 paginiPilipinas Shell Petroleum Corporation: SHLPHIsis Normagne PascualÎncă nu există evaluări

- MGT657 Chapter 7Document49 paginiMGT657 Chapter 7adamÎncă nu există evaluări

- 2007 FRM Practice ExamDocument116 pagini2007 FRM Practice Examabhishekriyer100% (1)

- Bank Mergers & Acquisitions in Central Eastern EuropeDocument96 paginiBank Mergers & Acquisitions in Central Eastern Europefumata23415123451Încă nu există evaluări

- GTE Financial Capacity Matrix (S) - Title & Name (2021)Document4 paginiGTE Financial Capacity Matrix (S) - Title & Name (2021)Anupriya RoyÎncă nu există evaluări

- 07 Quiz 1-BARIACTODocument2 pagini07 Quiz 1-BARIACTOdanibariactoÎncă nu există evaluări

- Thinking, Fast and Slow: By Daniel Kahneman (Trivia-On-Book)De la EverandThinking, Fast and Slow: By Daniel Kahneman (Trivia-On-Book)Evaluare: 5 din 5 stele5/5 (2)

- A Gentleman in Moscow by Amor Towles (Trivia-On-Books)De la EverandA Gentleman in Moscow by Amor Towles (Trivia-On-Books)Evaluare: 2.5 din 5 stele2.5/5 (3)

- Sid Meier's Memoir!: A Life in Computer GamesDe la EverandSid Meier's Memoir!: A Life in Computer GamesEvaluare: 4.5 din 5 stele4.5/5 (37)

- The Psychic Workbook: A Beginner's Guide to Activities and Exercises to Unlock Your Psychic SkillsDe la EverandThe Psychic Workbook: A Beginner's Guide to Activities and Exercises to Unlock Your Psychic SkillsEvaluare: 4.5 din 5 stele4.5/5 (2)

- How to Win the Lottery: Simple Lottery Strategies for Beginners and the Very UnluckyDe la EverandHow to Win the Lottery: Simple Lottery Strategies for Beginners and the Very UnluckyÎncă nu există evaluări