S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Employee Benefits OverviewDocument6 paginiEmployee Benefits OverviewLui100% (1)

- Ballpen finder income and no-name finder no incomeDocument88 paginiBallpen finder income and no-name finder no incomereylaxa100% (1)

- Oracle HRMS Setup For SingaporeDocument33 paginiOracle HRMS Setup For SingaporeShmagsi11Încă nu există evaluări

- TSDBF Answering Affidavit (Signed) 020919-OCRDocument147 paginiTSDBF Answering Affidavit (Signed) 020919-OCRjillianÎncă nu există evaluări

- Novartis NPS Employee Awareness Presentation PDFDocument33 paginiNovartis NPS Employee Awareness Presentation PDFMohan CÎncă nu există evaluări

- Microsoft Employee Benefits GuideDocument2 paginiMicrosoft Employee Benefits Guidedali2Încă nu există evaluări

- Income Taxation-IndividualDocument118 paginiIncome Taxation-Individualjovelyn labordoÎncă nu există evaluări

- Aditya Birla Company ProfileDocument8 paginiAditya Birla Company ProfileShubham NarwadeÎncă nu există evaluări

- AUDIT PROBS-2nd MONTHLY ASSESSMENTDocument7 paginiAUDIT PROBS-2nd MONTHLY ASSESSMENTGRACELYN SOJORÎncă nu există evaluări

- Tamilnadu Govt Pongal Bonus G.O No 1 Date 03.01.2011 English VersionDocument4 paginiTamilnadu Govt Pongal Bonus G.O No 1 Date 03.01.2011 English VersionMohankumar P KÎncă nu există evaluări

- The Evolution of IncomeDocument4 paginiThe Evolution of IncomesoujnyÎncă nu există evaluări

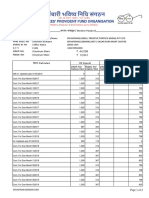

- Pension Fund Regulatory and Development AuthorityDocument11 paginiPension Fund Regulatory and Development AuthorityParitosh ChaudharyÎncă nu există evaluări

- LNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareDocument2 paginiLNL Iklcqd /: Employee Share Employer Share Employee Share Employer Shareshubham chutkeÎncă nu există evaluări

- NPS Transaction Statement SummaryDocument3 paginiNPS Transaction Statement SummaryAbburi Kumar AshokÎncă nu există evaluări

- Income Tax StatementDocument2 paginiIncome Tax StatementgdÎncă nu există evaluări

- Pay Slip: Payroll Basic DataDocument2 paginiPay Slip: Payroll Basic DataAdarsha ChandelÎncă nu există evaluări

- Form 16 TDS CertificateDocument3 paginiForm 16 TDS Certificatessanju_bhatÎncă nu există evaluări

- Normes Comptable Américaine ARB - 43Document45 paginiNormes Comptable Américaine ARB - 43Rakl LoÎncă nu există evaluări

- Provident Fund DataDocument4 paginiProvident Fund DataAishwarya SharmaÎncă nu există evaluări

- Apply Sure Start Maternity Grant HelpDocument11 paginiApply Sure Start Maternity Grant HelpKenya GrigoreÎncă nu există evaluări

- Aging and Financial Markets.Document12 paginiAging and Financial Markets.Angela JaspeÎncă nu există evaluări

- Tutorial 2 - Mathematics of Finance PDFDocument3 paginiTutorial 2 - Mathematics of Finance PDFИбрагим ИбрагимовÎncă nu există evaluări

- Edwards V Skyways LTDDocument2 paginiEdwards V Skyways LTDWan Farzana100% (1)

- Maxwell ScandalDocument4 paginiMaxwell ScandalShoaib SharifÎncă nu există evaluări

- 57 Promenade Pty LTD: BISM7202 Assignment - Semester 1, 2020 Assignment TemplateDocument34 pagini57 Promenade Pty LTD: BISM7202 Assignment - Semester 1, 2020 Assignment Templateharoon nasirÎncă nu există evaluări

- What Is A 401Document6 paginiWhat Is A 401KidMonkey2299Încă nu există evaluări

- Engineering EconomicsDocument14 paginiEngineering EconomicsGeraldÎncă nu există evaluări

- Business Taxation Notes Income Tax NotesDocument303 paginiBusiness Taxation Notes Income Tax NotesIkra MalikÎncă nu există evaluări

- A Report On Financial Statement of Hindustan ConstructionDocument18 paginiA Report On Financial Statement of Hindustan ConstructionNaag RajÎncă nu există evaluări

- Solvency 2Document8 paginiSolvency 2Daniel MateiÎncă nu există evaluări