S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Social and Economic Change by Financial InclusionDocument3 paginiSocial and Economic Change by Financial InclusionSubhash DsouzaÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- CRITICAL STUDY OF RURAL DEVELOPMENT THRUOGH CO-OPERATIVE MOVEMENT - A CASE STUDY OF CO-OPERATIVES IN VASAI TALUKA CRITICAL STUDY OF RURAL DEVELOPMENT THRUOGH CO-OPERATIVE MOVEMENT - A CASE STUDY OF CO-OPERATIVES IN VASAI TALUKADocument12 paginiCRITICAL STUDY OF RURAL DEVELOPMENT THRUOGH CO-OPERATIVE MOVEMENT - A CASE STUDY OF CO-OPERATIVES IN VASAI TALUKA CRITICAL STUDY OF RURAL DEVELOPMENT THRUOGH CO-OPERATIVE MOVEMENT - A CASE STUDY OF CO-OPERATIVES IN VASAI TALUKASubhash DsouzaÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Cooperatives and Financial InclusionDocument6 paginiCooperatives and Financial InclusionSubhash DsouzaÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Rural development certificate guide certificationDocument15 paginiRural development certificate guide certificationSubhash DsouzaÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Ibs Kota Bharu 1 31/03/23Document8 paginiIbs Kota Bharu 1 31/03/23Azam WahidÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Chapter 5 AAOIFI and MASBDocument21 paginiChapter 5 AAOIFI and MASBHeerlina PariuryÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Dissolution Changes in OwnershipDocument29 paginiDissolution Changes in OwnershipKenaniah SanchezÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- 11 Tips for Effective Business Chat and Email WritingDocument3 pagini11 Tips for Effective Business Chat and Email WritingAnn DroÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Simply Jordan TD Bank Statement Castillo Mar 2021Document2 paginiSimply Jordan TD Bank Statement Castillo Mar 2021MD MasumÎncă nu există evaluări

- Trends and Prospects of Mobile Payment Industry in China 2012-2015Document0 paginiTrends and Prospects of Mobile Payment Industry in China 2012-2015zvonimir1511Încă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- WhitepaperDocument12 paginiWhitepaperPepa pigÎncă nu există evaluări

- Not For Profit Organisation1Document20 paginiNot For Profit Organisation1Harsh ThakurÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Material For BSC6900 UMTS Parameter Changes (V900R018C10 Vs V900R016C00)Document19 paginiMaterial For BSC6900 UMTS Parameter Changes (V900R018C10 Vs V900R016C00)Diego Germán Domínguez HurtadoÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Fibocom FG360 EAU Datasheet - V1.7Document2 paginiFibocom FG360 EAU Datasheet - V1.7kashif bharwana TvÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Payment Receipt Oyo - 15-03-2021Document1 paginăPayment Receipt Oyo - 15-03-2021Ritesh0% (1)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- AC Exam PDF - IBPS Clerk 2019 by AffairsCloud PDFDocument115 paginiAC Exam PDF - IBPS Clerk 2019 by AffairsCloud PDFAZMI 333625Încă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Kotak MahindraDocument43 paginiKotak MahindraUZARA KHANÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- Samsung Le32a656a1f XXH Quick StartDocument5 paginiSamsung Le32a656a1f XXH Quick StartTomasz SkrzypińskiÎncă nu există evaluări

- Organizational Communication Group 18Document46 paginiOrganizational Communication Group 18pankajbhatt1993Încă nu există evaluări

- Your Flight Ticket - FMN1HCMLXMUDocument2 paginiYour Flight Ticket - FMN1HCMLXMUSurya thotaÎncă nu există evaluări

- Accounting Quiz on Merchandising ConceptsDocument8 paginiAccounting Quiz on Merchandising ConceptsJayson LucenaÎncă nu există evaluări

- OM3 CH 12 Managing InventoriesDocument19 paginiOM3 CH 12 Managing InventoriesGanessa RolandÎncă nu există evaluări

- Medical InsuranceDocument1 paginăMedical InsuranceMasood AhmadÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- GSM/GPRS Modem Wireless ConnectivityDocument2 paginiGSM/GPRS Modem Wireless ConnectivityAaaaÎncă nu există evaluări

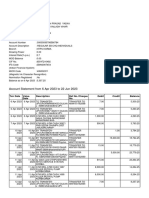

- Account Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 paginiAccount Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNishant Sagar DewanganÎncă nu există evaluări

- Topics in Preliminary for Highway and Railroad EngineeringDocument15 paginiTopics in Preliminary for Highway and Railroad EngineeringRodin James GabrilloÎncă nu există evaluări

- Case Study On Bay Networks IncDocument2 paginiCase Study On Bay Networks IncAbhishekKaushik100% (3)

- Quectel AG35 at Commands Manual V1.0Document238 paginiQuectel AG35 at Commands Manual V1.0Alex BaranciraÎncă nu există evaluări

- AUDTHEO2 Activity 1 AnswersDocument4 paginiAUDTHEO2 Activity 1 AnswersChristian Arnel Jumpay LopezÎncă nu există evaluări

- Chapter 5 QuizextraDocument5 paginiChapter 5 QuizextraAra AlcantaraÎncă nu există evaluări

- Gmail - Accenture Location DetailsDocument3 paginiGmail - Accenture Location Detailsrithuik1598Încă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Services: Reply To AdDocument3 paginiServices: Reply To AdSeanKeithNeriÎncă nu există evaluări

- Switch Juniper EX4650 (Datasheet)Document13 paginiSwitch Juniper EX4650 (Datasheet)Alejandro NavaÎncă nu există evaluări

- Activity 7 Villanueva BSBA FM 3Document3 paginiActivity 7 Villanueva BSBA FM 3Infinity TVÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)