S-ar putea să vă placă și

- Chapter 3Document173 paginiChapter 3Maria HafeezÎncă nu există evaluări

- Capital Budgeting FinalDocument46 paginiCapital Budgeting FinalMihir ShahÎncă nu există evaluări

- Investment Appraisal: Qs 435 Construction ECONOMICS IIDocument38 paginiInvestment Appraisal: Qs 435 Construction ECONOMICS IIGithu RobertÎncă nu există evaluări

- CH04 The Capital Budgeting Decision-UoHDocument31 paginiCH04 The Capital Budgeting Decision-UoHNimao SaedÎncă nu există evaluări

- Basic Methods For Making Economy Study (Written Report)Document9 paginiBasic Methods For Making Economy Study (Written Report)xxkooonxx100% (1)

- BUAD 839 ASSIGNMENT (Group F)Document4 paginiBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaÎncă nu există evaluări

- CH04 The Capital Budgeting DecisionDocument31 paginiCH04 The Capital Budgeting DecisionJamaÎncă nu există evaluări

- Ross Chapter 9 NotesDocument11 paginiRoss Chapter 9 NotesYuk Sim100% (1)

- Maximizing Profits Through Profitability Standards and Investment AnalysisDocument27 paginiMaximizing Profits Through Profitability Standards and Investment AnalysisRamez AlaliÎncă nu există evaluări

- CapitalizationDocument5 paginiCapitalizationmamp05Încă nu există evaluări

- Evaluating Project Risks & Capital RationingDocument53 paginiEvaluating Project Risks & Capital RationingShoniqua JohnsonÎncă nu există evaluări

- Ebtm3103 Slides Topic 3Document26 paginiEbtm3103 Slides Topic 3SUHAILI BINTI BOHORI STUDENTÎncă nu există evaluări

- Evaluating Production Investment AlternativesDocument26 paginiEvaluating Production Investment AlternativesSean WilsonÎncă nu există evaluări

- ARR, IRR and PIDocument8 paginiARR, IRR and PIAli HamzaÎncă nu există evaluări

- Combined Heating, Cooling & Power HandbookDocument8 paginiCombined Heating, Cooling & Power HandbookFREDIELABRADORÎncă nu există evaluări

- Capital BudgetingDocument12 paginiCapital BudgetingRizwan Ali100% (1)

- Capital BudgetingDocument5 paginiCapital BudgetingMaria StephenÎncă nu există evaluări

- Profitability AnalysisDocument43 paginiProfitability AnalysisAvinash Iyer100% (1)

- International Capital Burgeting AssignmentDocument22 paginiInternational Capital Burgeting AssignmentHitesh Kumar100% (1)

- Chap 9 Notes To Accompany The PP TransparenciesDocument8 paginiChap 9 Notes To Accompany The PP TransparenciesChantal AouadÎncă nu există evaluări

- PAYBACK PERIOD ANALYSIS: HOW TO EVALUATE INVESTMENT PROJECTS USING THE PAYBACK METHODDocument7 paginiPAYBACK PERIOD ANALYSIS: HOW TO EVALUATE INVESTMENT PROJECTS USING THE PAYBACK METHODSurya SumanÎncă nu există evaluări

- Investments Capital: Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To DetermineDocument9 paginiInvestments Capital: Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To DetermineManogya BhaskarÎncă nu există evaluări

- Chapter 7 Asset Investment Decisions and Capital RationingDocument31 paginiChapter 7 Asset Investment Decisions and Capital RationingdperepolkinÎncă nu există evaluări

- Weygandt, Kieso, & Kimmel: Managerial AccountingDocument54 paginiWeygandt, Kieso, & Kimmel: Managerial AccountingGiulia TabaraÎncă nu există evaluări

- Lecturenote - 1762467632financial Management-Chapter ThreeDocument22 paginiLecturenote - 1762467632financial Management-Chapter ThreeJOHNÎncă nu există evaluări

- Financial Management: A Project On Capital BudgetingDocument20 paginiFinancial Management: A Project On Capital BudgetingHimanshi SethÎncă nu există evaluări

- Capital Budgeting and Cost Analysis MethodsDocument75 paginiCapital Budgeting and Cost Analysis MethodsAkhil BatraÎncă nu există evaluări

- Project Selection Models and TechniquesDocument50 paginiProject Selection Models and TechniquesNeway Alem100% (1)

- ASsignmentDocument10 paginiASsignmenthu mirzaÎncă nu există evaluări

- What Is Capital BudgetingDocument24 paginiWhat Is Capital BudgetingZohaib Zohaib Khurshid AhmadÎncă nu există evaluări

- Capital Budgeting Chapter ReviewDocument27 paginiCapital Budgeting Chapter Reviewcindysia000Încă nu există evaluări

- Payback Period Method For Capital Budgeting DecisionsDocument5 paginiPayback Period Method For Capital Budgeting DecisionsAmit Kainth100% (1)

- Net Present Value and The Internal Rate of Return - CFA Level 1 - InvestopediaDocument9 paginiNet Present Value and The Internal Rate of Return - CFA Level 1 - InvestopediaPrannoyChakrabortyÎncă nu există evaluări

- Applied Corporate Finance. What is a Company worth?De la EverandApplied Corporate Finance. What is a Company worth?Evaluare: 3 din 5 stele3/5 (2)

- NPV Recommended for Investment Appraisal Due to Consideration of Time Value and All Cash FlowsDocument3 paginiNPV Recommended for Investment Appraisal Due to Consideration of Time Value and All Cash FlowsWasi Nafijur RahmanÎncă nu există evaluări

- Accounting ExplainedDocument69 paginiAccounting ExplainedGeetaÎncă nu există evaluări

- Capital BudgetingDocument8 paginiCapital BudgetingVarsha KastureÎncă nu există evaluări

- CapbudgetDocument31 paginiCapbudgetnaveen penugondaÎncă nu există evaluări

- Net Present ValueDocument17 paginiNet Present ValueSalman JindranÎncă nu există evaluări

- Capital Budgeting MethodsDocument13 paginiCapital Budgeting MethodsAmit SinghÎncă nu există evaluări

- Capital BudgetingDocument52 paginiCapital BudgetingMichael BlueÎncă nu există evaluări

- 8.3: The Profitability Index Definition: The Profitability Index Is A Method To Evaluate An Investment Project. It Is TheDocument2 pagini8.3: The Profitability Index Definition: The Profitability Index Is A Method To Evaluate An Investment Project. It Is ThetedyfardiansyahÎncă nu există evaluări

- Analyzing Profitability MethodsDocument6 paginiAnalyzing Profitability MethodsMuhammad MustafaÎncă nu există evaluări

- Financial Management Chapter 09 IM 10th EdDocument24 paginiFinancial Management Chapter 09 IM 10th EdDr Rushen SinghÎncă nu există evaluări

- Cost Benefit AnalysisDocument23 paginiCost Benefit AnalysisIvan LopezÎncă nu există evaluări

- Capital Budgeting TechniquesDocument8 paginiCapital Budgeting TechniquesshankariscribdÎncă nu există evaluări

- Project Appraisal TechniquesDocument31 paginiProject Appraisal TechniquesRajeevAgrawal86% (7)

- Case Study RevisedDocument7 paginiCase Study Revisedbhardwaj_manish44100% (3)

- UntitledDocument145 paginiUntitleddhirajpironÎncă nu există evaluări

- Capital Budgeting Methods and DecisionsDocument4 paginiCapital Budgeting Methods and Decisionshxn1421Încă nu există evaluări

- Capital BudgetingDocument12 paginiCapital Budgetingjunhe898Încă nu există evaluări

- Capital Budgeting: Learning ObjectivesDocument41 paginiCapital Budgeting: Learning ObjectivesJane Michelle EmanÎncă nu există evaluări

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsDe la EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsÎncă nu există evaluări

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisDe la EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisÎncă nu există evaluări

- DCF Budgeting: A Step-By-Step Guide to Financial SuccessDe la EverandDCF Budgeting: A Step-By-Step Guide to Financial SuccessÎncă nu există evaluări

- Discounted Cash Flow Demystified: A Comprehensive Guide to DCF BudgetingDe la EverandDiscounted Cash Flow Demystified: A Comprehensive Guide to DCF BudgetingÎncă nu există evaluări

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationDe la EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationÎncă nu există evaluări

- Polytropic CompressionDocument22 paginiPolytropic CompressionSonal Power Unlimitd50% (2)

- Trans Jour 1Document4 paginiTrans Jour 1Sonal Power UnlimitdÎncă nu există evaluări

- Travel Details:: Fjordtours@fjordtours - NoDocument1 paginăTravel Details:: Fjordtours@fjordtours - NoSonal Power UnlimitdÎncă nu există evaluări

- Star CollegeDocument27 paginiStar CollegeSonal Power UnlimitdÎncă nu există evaluări

- Your Booking Has Been Successfully Completed. A Confirmation Email Will Be Sent To YouDocument2 paginiYour Booking Has Been Successfully Completed. A Confirmation Email Will Be Sent To YouSonal Power UnlimitdÎncă nu există evaluări

- Automation NotesDocument28 paginiAutomation NotesSonal Power UnlimitdÎncă nu există evaluări

- PcsDocument9 paginiPcsSonal Power UnlimitdÎncă nu există evaluări

- Thank You For Your Order!: What Are The Benefits of Registering As A Customer?Document1 paginăThank You For Your Order!: What Are The Benefits of Registering As A Customer?Sonal Power UnlimitdÎncă nu există evaluări

- LG Master K Training 1Document74 paginiLG Master K Training 1Khaled Chowdhury100% (6)

- Fluid FrictionDocument6 paginiFluid FrictionVinay KumarÎncă nu există evaluări

- Fluid FrictionDocument6 paginiFluid FrictionVinay KumarÎncă nu există evaluări

- LG Master K Training 1Document74 paginiLG Master K Training 1Khaled Chowdhury100% (6)

- Fluid FrictionDocument6 paginiFluid FrictionVinay KumarÎncă nu există evaluări

- Star CollegeDocument27 paginiStar CollegeSonal Power UnlimitdÎncă nu există evaluări

- LG Master K Training 1Document74 paginiLG Master K Training 1Khaled Chowdhury100% (6)

- LG Master K Training 1Document74 paginiLG Master K Training 1Khaled Chowdhury100% (6)

- Pressure FundamentalsDocument14 paginiPressure FundamentalsGuillermo RastelliÎncă nu există evaluări

- Ground FaultDocument54 paginiGround FaultSonal Power UnlimitdÎncă nu există evaluări

- TestDocument1 paginăTestSonal Power UnlimitdÎncă nu există evaluări

- TestDocument1 paginăTestSonal Power UnlimitdÎncă nu există evaluări

- Automated Application of Design Patterns: A Refactoring ApproachDocument242 paginiAutomated Application of Design Patterns: A Refactoring ApproachSonal Power UnlimitdÎncă nu există evaluări

- Automation Programming in PLC CodeDocument122 paginiAutomation Programming in PLC CodeSonal Power UnlimitdÎncă nu există evaluări

- Fluid FrictionDocument6 paginiFluid FrictionVinay KumarÎncă nu există evaluări

- BIM2Met Exam GuideDocument21 paginiBIM2Met Exam GuideSonal Power UnlimitdÎncă nu există evaluări

- TestDocument1 paginăTestSonal Power UnlimitdÎncă nu există evaluări

- Specification 612 Rev 1264150583. 0 Testing Precommissioning and CommissioningDocument54 paginiSpecification 612 Rev 1264150583. 0 Testing Precommissioning and Commissioningcharleselitb92Încă nu există evaluări

- Instrumentation Q&ADocument8 paginiInstrumentation Q&ASonal Power UnlimitdÎncă nu există evaluări

- Drives & ControlsDocument102 paginiDrives & ControlsSonal Power UnlimitdÎncă nu există evaluări

- Colebrook White. (1939)Document29 paginiColebrook White. (1939)carloscartasine100% (2)

- VALTEK Valve Size PDFDocument16 paginiVALTEK Valve Size PDFalbahbahaneeÎncă nu există evaluări

- Foreign BanksDocument9 paginiForeign Banks1986anuÎncă nu există evaluări

- Quantitative Trading Strategies Using Python Technical Analysis, Statistical Testing, and Machine Learning (Peng Liu) (Z-Library)Document341 paginiQuantitative Trading Strategies Using Python Technical Analysis, Statistical Testing, and Machine Learning (Peng Liu) (Z-Library)alex seow100% (1)

- AugDocument3 paginiAugArjun Mishra0% (1)

- Tutorial Chapter 3 Cash BudgetDocument12 paginiTutorial Chapter 3 Cash Budgetrayyan danÎncă nu există evaluări

- The History of MoneyDocument30 paginiThe History of MoneyBea Nicole AugustoÎncă nu există evaluări

- LT E-BillDocument2 paginiLT E-BillSachin VaishnavÎncă nu există evaluări

- Final Report - Payments ProcessDocument32 paginiFinal Report - Payments Processmrshami7754Încă nu există evaluări

- Accounting For Foreign Currency Transactions PDFDocument49 paginiAccounting For Foreign Currency Transactions PDFDaniel DakaÎncă nu există evaluări

- Working Capital Management AssignmentDocument10 paginiWorking Capital Management AssignmentRitesh Singh RathoreÎncă nu există evaluări

- Introduction To Corporate FinanceDocument29 paginiIntroduction To Corporate FinanceYee Mon AungÎncă nu există evaluări

- Home Loan Form 2023Document6 paginiHome Loan Form 2023Sitar ComebackÎncă nu există evaluări

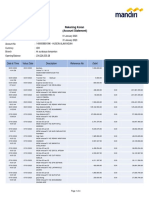

- Rek Koran Mandiri PT HAI Jan-April 2023Document14 paginiRek Koran Mandiri PT HAI Jan-April 2023wahyu suhartonoÎncă nu există evaluări

- Modes of Islamic Finance AssignmentDocument4 paginiModes of Islamic Finance AssignmentSohaib AsifÎncă nu există evaluări

- This Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)Document6 paginiThis Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)kashanr82Încă nu există evaluări

- Axis Triple Advantage Fund Application FormDocument8 paginiAxis Triple Advantage Fund Application Formrkdgr87880Încă nu există evaluări

- U.S.a. - The House That No One Lives inDocument52 paginiU.S.a. - The House That No One Lives inMichael McCurdyÎncă nu există evaluări

- 4.3 Q MiniCase Turkish Kriz (A)Document6 pagini4.3 Q MiniCase Turkish Kriz (A)SanaFatimaÎncă nu există evaluări

- 1540395230512Gvsx636FlEg3pp89 PDFDocument3 pagini1540395230512Gvsx636FlEg3pp89 PDFMathew RaiÎncă nu există evaluări

- Ank Otes: Bank Deposits Are Risky - Now More Than EverDocument12 paginiAnk Otes: Bank Deposits Are Risky - Now More Than EverMichael HeidbrinkÎncă nu există evaluări

- Fundamentals of Finance: Ignacio Lezaun English Edition 2021Document25 paginiFundamentals of Finance: Ignacio Lezaun English Edition 2021Elias Macher CarpenaÎncă nu există evaluări

- Analyze Financial Statements with Common-Size StatementsDocument33 paginiAnalyze Financial Statements with Common-Size StatementsAiden Pats100% (1)

- Sign Verified Tax Invoice for GPON Fiber HD5 HYD 50Mbps Monthly SubscriptionDocument1 paginăSign Verified Tax Invoice for GPON Fiber HD5 HYD 50Mbps Monthly SubscriptionShetkar GouthamÎncă nu există evaluări

- Harshad Mehta's Connection to BPL ScamDocument9 paginiHarshad Mehta's Connection to BPL ScamDharmendra SinghÎncă nu există evaluări

- My BillDocument2 paginiMy BillMohammad AtifÎncă nu există evaluări

- International BankingDocument21 paginiInternational BankingVarun Rauthan50% (2)

- Sunview 2023 Q2Document20 paginiSunview 2023 Q2Quint WongÎncă nu există evaluări

- Investment Objective: Fund Fact Sheet As of September 2020Document2 paginiInvestment Objective: Fund Fact Sheet As of September 2020Neil MijaresÎncă nu există evaluări

- Internship Report: Janata Bank Limited and Its General Banking ActivitiesDocument54 paginiInternship Report: Janata Bank Limited and Its General Banking ActivitiesMehedi HasanÎncă nu există evaluări

- Survey of Accounting 6Th Edition Warren Solutions Manual Full Chapter PDFDocument46 paginiSurvey of Accounting 6Th Edition Warren Solutions Manual Full Chapter PDFzanewilliamhzkbr100% (5)

- Mundell-Fleming Model IS-LM FrameworkDocument30 paginiMundell-Fleming Model IS-LM FrameworkAnonymous Ptxr6wl9DhÎncă nu există evaluări