S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Red Herring ProspectusDocument414 paginiRed Herring ProspectusTejesh GoudÎncă nu există evaluări

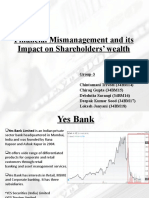

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 paginiGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodÎncă nu există evaluări

- Guideline 3. Parte Cesar MartinezDocument25 paginiGuideline 3. Parte Cesar MartinezCesarMartinezÎncă nu există evaluări

- 6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresDocument45 pagini6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresSullivan LyaÎncă nu există evaluări

- Company Info - Print FinancialsDocument5 paginiCompany Info - Print FinancialsVishvajit PatilÎncă nu există evaluări

- Summary Pointer Chapter 2 Advanced AccountingDocument6 paginiSummary Pointer Chapter 2 Advanced Accountingahmed arfanÎncă nu există evaluări

- The Fashion Rack: FDNACCT: Group Case AnalysisDocument6 paginiThe Fashion Rack: FDNACCT: Group Case AnalysisPrincess HoshinoÎncă nu există evaluări

- Accounts ReceivableDocument7 paginiAccounts ReceivablePeter PiperÎncă nu există evaluări

- Lcci LV I TextDocument65 paginiLcci LV I TextPyin Nyar AungÎncă nu există evaluări

- AdvacDocument13 paginiAdvacAmie Jane MirandaÎncă nu există evaluări

- Chapter 5 PPEDocument99 paginiChapter 5 PPELay100% (1)

- End. 12,133 End. 6,950 End. 612Document3 paginiEnd. 12,133 End. 6,950 End. 612Nam NguyenÎncă nu există evaluări

- This Study Resource Was: F-ACADL-01Document8 paginiThis Study Resource Was: F-ACADL-01Marjorie PalmaÎncă nu există evaluări

- Quiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueDocument2 paginiQuiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueUNKNOWNN50% (2)

- Handout Bus Com 2302Document6 paginiHandout Bus Com 2302Cylevri TomimboÎncă nu există evaluări

- Corporate Accounting PDFDocument5 paginiCorporate Accounting PDFshivaji jadhavÎncă nu există evaluări

- Tugas2 Elriska Tiffani 142200111 EA-DDocument4 paginiTugas2 Elriska Tiffani 142200111 EA-DElriska TiffaniÎncă nu există evaluări

- FINA 1310 Course Schedule KLDocument2 paginiFINA 1310 Course Schedule KLadmin AdminÎncă nu există evaluări

- Managerial Accounting - HW Case 5-2 Celtex Feb 05 2011Document1 paginăManagerial Accounting - HW Case 5-2 Celtex Feb 05 2011Gautam RandhawaÎncă nu există evaluări

- Assets and Liability Management: A Synopsis Report ONDocument8 paginiAssets and Liability Management: A Synopsis Report ONMohmmedKhayyumÎncă nu există evaluări

- Answer KeysDocument26 paginiAnswer Keysmia uyÎncă nu există evaluări

- Disinformation Index Foundation (An Foundation) 2021 990Document20 paginiDisinformation Index Foundation (An Foundation) 2021 990Gabe KaminskyÎncă nu există evaluări

- Book Building: Presented By: Rajni Sharma MBA, Final YearDocument23 paginiBook Building: Presented By: Rajni Sharma MBA, Final YearRixim86% (7)

- HO 1 - Commercial Law - Corporation Law PDFDocument35 paginiHO 1 - Commercial Law - Corporation Law PDFBerchman MelendezÎncă nu există evaluări

- Caf 5 Far1 STDocument588 paginiCaf 5 Far1 STMuhammad YousafÎncă nu există evaluări

- Annexure B To Directors' Report Report On Corporate GovernanceDocument10 paginiAnnexure B To Directors' Report Report On Corporate GovernancePritam BhadadeÎncă nu există evaluări

- Hertz AMC Chapter 11 FT 2021-01-26Document1 paginăHertz AMC Chapter 11 FT 2021-01-26Karya BangunanÎncă nu există evaluări

- Long StrangleDocument2 paginiLong StrangleAKSHAYA AKSHAYAÎncă nu există evaluări

- Mergers and Acquisitions 2021Document47 paginiMergers and Acquisitions 2021Evelyne BiwottÎncă nu există evaluări

- F2 Exam Practice Kit PDFDocument634 paginiF2 Exam Practice Kit PDFZHANG EmilyÎncă nu există evaluări