Documente Academic

Documente Profesional

Documente Cultură

Compare The World Steel and Copper Markets: Similarities and Differences

Încărcat de

Alain MermoudTitlu original

Drepturi de autor

Formate disponibile

Partajați acest document

Partajați sau inserați document

Vi se pare util acest document?

Este necorespunzător acest conținut?

Raportați acest documentDrepturi de autor:

Formate disponibile

Compare The World Steel and Copper Markets: Similarities and Differences

Încărcat de

Alain MermoudDrepturi de autor:

Formate disponibile

ASSIGNEMENTINTERNATIONALECONOMICS&POLITICS

Subjectarea Globalsteel&coppermarkets

Rawmaterialmarketsanalysis

Commoditiesexchanges

Projectsupervisor Prof.Dr.Jean-DanielClavel

Submittedby AlainMermoud

alain.mermoud@etu.hesge.ch

Date 04.01.10

January

10

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

TableofContents

Executivesummary ................................................................................................ 3

Abbreviations......................................................................................................... 3

1 Introduction ..................................................................................................... 4

2 Parameters&frameworkconditions ................................................................ 4

2.1 History......................................................................................................................................................... 4

2.2 Strategicpositionandmajoreconomicsectors ........................................................................ 4

2.3 Politicalsituationandlegalissues .................................................................................................. 6

2.4 Culturalaspect ......................................................................................................................................... 6

2.5 Environment............................................................................................................................................. 6

2.6 Productionprocess................................................................................................................................ 6

2.7 Productspecificities .............................................................................................................................. 7

3 Analysis ............................................................................................................ 7

3.1 Economicanalysis.................................................................................................................................. 7

3.2 Positionofsteelandcopperininternationaltrade................................................................. 7

3.3 Macroeconomicparameters.............................................................................................................. 8

3.4 Businessstructuresusuallyused .................................................................................................... 8

3.5 Majortradingpartnersoverallworldexports&imports ................................................. 9

3.6 Marketfacts&figures........................................................................................................................ 10

3.7 Extentofinternationalintegration.............................................................................................. 10

4 Potentialoutcomes......................................................................................... 10

5 Personalassessment....................................................................................... 11

6 Prospects........................................................................................................ 11

7 Conclusion...................................................................................................... 12

Bibliography...................................................................................................................................................... 13

Attachments....................................................................................................................................................... 14

Statistics&tables ............................................................................................................................................ 15

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

3

Executivesummary

Steel is essential for economic growth; as it is primarily used for housing and

construction, infrastructures, transport and energy delivery. Indeed, this metal is the

second most important commodity (15%) after oil. The worldwide steel industry has

notescapedthecurrenteconomicdownturnandrecession.Theindustryhasresponded

rapidly with production cuts, to ensure supply matches demand. The main producer

countries are China, Japan, and the USA. The largest companies are ArcelorMittal,

Nippon Steel and Baosteel Group. Almost 40% of the steel production is exported

internationally.

Copper is a key raw material used worldwide in the industrial development. Its unique

physical and chemical properties (ductility, malleability, conductivity, corrosion

resistant, etc.), make it a superior material for use in constructions (almost 37% of the

market),telecommunications,transportations,etc.Theprincipalsourceofworldcopper

supply is from mine production and recycling (12%). Latin America is the biggest

contributor to mine production at 45%, followed by former Eastern Bloc countries at

19%,Oceaniaat18%andNorthAmericaat12%.

The steel and copper markets face similar issues such as sustainable development

(necessity to reduce CO2 emissions) and the global economic crisis, which reduce

demandandthereforeleadsquicklytoovercapacity.Bothmarketsareoftenconsidered

as being indicators of economic progress, because of their critical role played in

infrastructuresandoveralldevelopment.

Abbreviations

SHME ShanghaiMetalExchange

LME LondonMetalExchange

COMEX/NYMEX CommodityExchangeDivisionoftheNewYorkMercantileExchange

EU EuropeanUnion

GDP GrossDomesticProduct

GNP GrossNationalIncome

OECD OrganizationforEconomicCo-operationandDevelopment

FTA FreeTradeAgreement

LTO Long-TermOrientation

ICSG InternationalCopperStudyGroup

WSA WorldSteelAssociation

GSSA GlobalSteelSectoralApproach

SWOT StrengthWeaknessOpportunitiesThreats

WTO WorldTradeOrganization

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

4

1 Introduction

The copper and the steel markets shares some characteristics but are also different, in

terms of extraction, use, recycling, supply, etc. The purpose of this study is to expose

bothdifferencesandsimilaritiesofthesetworawmaterials.

Copperandsteelarecloselylinkedwiththeriseofmodernsocieties,andthereforethe

value of the metals grows with the development of emerging countries. Indeed, both

steel and copper are essential for economic growth; as they are primarily used for

infrastructure, transport, energy delivery, housing and construction. Factors such as

mine supply growth, the development of new technologies, the general health of the

economyhaveadirectimpactonthemarketofbothcommodities.

The recent financial crisis has given unique indicators on how the global copper and

steelmarketsreactbothsimilarlyanddifferently-inaperiodofeconomicturbulences

and recession. This assignment also aims to analyze new trends and the general

perspectiveforthecomingyears.

The data and statistics are mainly collected from the OECD, the World steel in figures

2009 from the WSA and the World Copper Factbook 2009 from the ICSG. Regarding

themethodologyoftheresearch,severaltoolsgiveninclassareusedsuchastheSWOT

analyzeorthePortergenericstrategies.

While the two metals are closely linked to the economic and industrial development

worldwide,itiscertainthattheybothwillcontributetothedevelopmentofsocietywell

intothefuture.

2 Parameters&frameworkconditions

2.1 History

Steel is an alloy of iron and carbon. Iron is found on the earths crust, like most metals,

onlyintheformofanore,whichcanstillbefoundinabundancearoundtheglobe.Steel

is already mentioned in the Bible. Evidence of the first production of high carbon steel

was founded in India by about 300 BC. Modern steelmaking started in Europe in the

1600s using coke instead of charcoal. Historically, steel and iron were separate

products, but today they are usually classified in the same entity commonly called the

ironandsteelindustry.Today,strongeralloysandlightermetalshavebeeninvented.

Copperwasoneofthefirstmetalsusedbymankindtomakejewelryandcurrencycoins.

DuringtheRomanera,thismaterialwasmainlyextractedinCyprus,relatingtoCopper's

originalnameofCyprium,"metalofCyprus",latertobecalledCuprumlatetobeknown

as Cuprum. During the Copper Age (3500 to 1700BC.) the material was mainly used to

make tools and weapons. In the 18th and 19th century, the inventions based on

magnetism and electricity involved copper in the Industrial Revolution and gave it a

new impulse in the modern world. Mammals and different organic life forms also use

copper as a vital element of nutrition. Excess and deficiencies can be dangerous to

health.

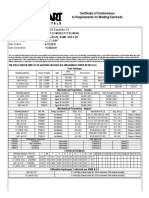

2.2 Strategicpositionandmajoreconomicsectors

Steel is the basic raw material for economic development. Before the introduction of

modern production techniques, it was considered as expensive and was therefore only

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

5

used when no cheaper alternative existed (swords, knives, razors). Nowadays steel is

used widely in the construction of roads, buildings, railways and other infrastructures

supportedbyasteelskeleton(airports,bridges,skyscrapers,etc.).

Humans started to use copper (chemical symbol Cu) at least 10,000 years ago and this

material is closely linked with the development of the modern civilization. Even today

copper-basedproductsarestillusedinahugerangeofindustryanddomesticactivities.

P

i

g

h

l

i

g

h

f

s

,

M

u

r

k

e

f

u

n

d

l

n

d

u

s

f

r

y

Steel Consumption and Markets

Steel consumption by end-user market in OECD*

3

2

1

4

5

o

B

Sourcc /rcciorMittci c.timctc..

1hc Orcni.ction or |conomic Coopcrction cnd Dcvciopmcnt.

Construct|on 44

^utomot|ve 19

Sh|pbu||d|ng 3

lec|eg|ng 4

Mechen|ce| end lndustr|e| mech|nery 22

O|| end Ces 5

le||s 2

Others 2

World steel market by product 2008

Sourcc Worid Stcci /..ociction.

1

2

3

Long 43

l|et 54

1ube 3

Steel consumption by region

Sourcc Worid Stcci /..ociction.

Luropeen 0n|on 15

ClS end Other Lurope

l^l1^ 11

Centre| end South ^mer|ce 4

Ch|ne 35

Jepen o

Other ^s|e 15

lest o the Wor|d

1

2

3

4

5

o

B

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! ;<<=!

!""#

$%&&'(

"""

China 6,937

Japan 1,622

South Korea 768

India 882

ASEAN 892

Taiwan 521

Region. Asia 11,622

North America 3,171

Rest oI World 2,186

Latin America 1,533

Region. All others 6,890

Western Europe 3,984

Eastern Europe 1,451

Region. Europe 5,435

)%*+, !-./01

>0*,1*%?!

-+%@&(08&*+%!

#A<==

B,0C9*%?!

"AD;E

>0*,1*%?!

B,)%&! "FG

H(85*&'8&0('!

I==

-+CC0%*8)&*+%@!

;;F

J,'8&(*8),!

B+K'(!

FAG";

$%L()@&(08&0('!

FAI=E

B+K'(!

M&*,*&2!

;A#;I

4','8+CN!

EGI

JO0*.&C'%&!

P)%0L)8&0('!

"IAFD<

$%10@&(*),!

IA#<F

H0&+C+&*Q'!

"A=<=

R&5'(!4()%@.+(&)&*+%!

"A<E#

-+%@0C'(!S!

3'%'(),!B(+108&@!

;A<<"

-++,*%?!

"A#IF

J,'8&(+%*8!

ED#

T*Q'(@'!

;A;D;

Major Uses of Copper: Usage by End-Use Sector and Region, 2008

Basis: copper content, thousand metric tonnes

Source: nternational Copper Association

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

6

2.3 Politicalsituationandlegalissues

Steel industry was delicensed and decontrolled in 1992. However, some actors of the

steel and copper markets are sometimes tempted by protectionism, which can lead to

distorted markets. For instance, in March 2002 the USA placed temporary tariffs on

imported steel, in order to protect steel makers. The EU decided that it would impose

retaliatory tariffs, risking to start a trade war. In 2002, the WTO came out against the

steel tariffs, arguing that they were a violation of the USAs WTO tariff-rate

commitments. This example shows how these two markets are also closely linked to

diplomacy.

2.4 Culturalaspect

Steel and copper will continue to play a key role in the metal industry in the future

years. Indeed, steel and copper-based alloys will still be used in a wide range of

applications of daily life. Plastics and synthetics could eventually replace some steel-

basedproductinthenextyears.

2.5 Environment

Theextractions,transportandproductionofthosetworawmaterialshaveanimpacton

the environment. Efficient use of these natural resources is critical for sustainable

development.CO2emissionsinthesteelsectorareprimarilytheresultofburningfossil

fuelsduringtheproductionofironandsteel.Thatsway,thepost-Kyotonegotiationsare

important for the steel industry, which has an ambitious program for every steel

company in the world to measure its CO2 emissions. Another ecological challenge will

betoreducethehugeconsumptionofelectricityneededforsteelproduction.Otherwise,

steel is one of the most recycled materials in the world. This table shows the recycled

steelconsumptionandapparentdomesticsupplyin2008,inmillionmetrictons.

(source:Worldsteelassociation)

Theprocessofminingcopperresultsinasignificantbyproductofwaterpollution.Acid

drainage is used frequently in the mining of copper and thus harmful atmospheric

emissions of sulphur and heavy metal particles are released into the air during the

refiningandsmeltingprocess.

2.6 Productionprocess

Professionals, like geologists, research for clues that show the presence of copper in

nature. Once the ecological, geological, legal and economic issues are resolved, mining

can start (leaching, surface, or underground mining). Open-pit mining is the method

mainlyusedworldwide.First,thecopper-bearingoreshavetobeextractedandmined.

To obtain 30% of copper concentrate, the ore has to be crushed and grinded, followed

by the concentration by flotation. In the next step, the concentration is boiled to a

distinctsmellinordertoobtaina"matte"with60%copper.Thenextstepprocessesthe

molten matte in a converter, resulting in 99% copper, called blister copper. Recycled

copper is called secondary copper and it cannot be differentiated from primary

worldsteel.org

Recycled steel

Recycled steel is a key input needed for all steelmaking process routes.

Steel is one of the few magnetic metals. It is easy to separate from t

waste streams. About 80% of post-consumer steel is recycled.

1

By sector, steel recovery rates are estimated at 85% for t

construction, 85% for automotive, 90% for machinery, and 50%

for electrical and domestic appliances.

1

Recycled steel supply is

expected to fall short of demand by 2012.

5

Recycled steel (scrap) can be collected from excess material t

in steel facilities and foundries (home scrap) or downstream

production processes (industrial scrap) and from discarded

products (obsolete scrap).

e availability of home and industrial scrap is closely related to t

current domestic steel production levels while the availability of

obsolete scrap is closely related to levels of past steel production,

average product lives and ecient recycling programmes.

EAFs can be charged with 90 to 100% of recycled steel, Basic t

Oxygen Furnaces with up to 30% (see Figure 2).

7

Scrap prices vary greatly for dierent qualities. In 2008 (May-July) t

the price for heavy melting steel scrap (HMS) reached US$520/t

while shredded scrap prices reached US$600/t.

6

Currently, the use of recycled steel appears to be limited only by t

availability and price, not the processing capacity in the worlds

steel mills (see Table 1).

1

Responsible management of natural resources

e steel industry is highly ecient in its use of raw materials with

technology available today. Key contributing factors include high

material eciency rates, by-product recycling and steel recycling.

Steelmaking is nearing zero-waste, with current material eciency

rates at around 97%. e recycling and use of by-products from

steelmaking is up to 98% in some countries.

1

Slag is the main steelmaking by-product; it is mostly used in t

cement production, reducing CO

2

emissions by around 50%.

11

It can also be used in roads (substituting aggregates), as fertiliser

(slag rich in phosphate, silicate, magnesium, lime, manganese

and iron), and in coastal marine blocks to facilitate coral growth

thereby improving the ocean environment.

1

Gases produced during steelmaking are fully reused as an energy t

source either in the blast furnace and reheating furnaces or in

power generation plants within the steelworks, saving fossil fuels.

Coke oven gas contains about 55% hydrogen and may prove an

important hydrogen source in the future.

10

Footnotes

From World Steel Association data or publications (worldsteel.org) 1.

Mineral Information Institute (mii.org) 2.

Analysis of economic indicators of the EU metals industry: the impact of raw materials and energy supply on competitiveness. European 3.

Commission, 2006

Iron Ore, Mineral Commodity Summaries. U.S. Geological Survey, 2007 (minerals.usgs.gov) 4.

EconStatsTM (econstats.com) 5.

Metal Bulletin Research, Steelmaking Raw Materials Monthly Issue 146, July 2008 6.

Coal & Steel Facts 2007. World Coal Institute. worldcoal.org 7.

Steel Industry and the Environment, Technical and Management Issues. IISI and UNEP Technical Report No. 38. 1997. 8.

Metal Bulletin, Issue no. 9042, April 2008. 9.

1he 3tate-of-the-Art Clean 1eohnologies (30AC1) for 3teelmaking andbook." Asia-Paoito Partnership for Clean Uevelopment and Climate, 2007 10.

Legal Status of Slags, Position Paper, January 2006, pages 2 and 10. The European Slag Association (Euroslag). 11.

TABLE 1: RECYCLED STEEL CONSUMPTION AND APPARENT DOMESTIC

SUPPLY 2007, MILLION METRIC TONS (MMT)

1

Recycled steel

consumption

Apparent domestic

supply

EU-27 115.6 117.8

Other Europe 25.3 10.9

CIS 50 58.2

NAFTA 81.3 96.1

Central/South America 14.3 14.4

Asia 189.2 172.8

World 481.9 478.9

FIGURE 2: RECYCLED STEEL USE IN STEELMAKING

Steel recycling

Steel products naturally contribute to resource conservation through

their lightweight potential, durability and recyclability. At the end of

a products life, steels 100% recyclability ensures that the resources

invested in its production are not lost and can be innitely reused.

More steel is recycled worldwide annually than all other materials

put together, with an estimated 459 million metric tons (mmt) being

recycled in 2006, about 37% of the crude steel produced that year.

1

Recycling this steel:

avoided 827mmt of CO t

2

emissions

saved 868 mmt of iron ore, and t

saved the energy equivalent of 242 mmt of anthracite coal. t

1

WORLDSTEEL FACT SHEET

Last updated: October 2008

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

7

copper.Becauseofthissimilarity,copperisoneofthemostrecycledmetals.Copperis

mainlyshippedtocustomersortobemanufacturedaswirerod,ingot,cathodeorbillet.

Modern steelmaking began with the Bessemer process introduced in 1858, using

directly with pig iron as raw material. This was the first inexpensive industrial process

forthecheapmass-productionofsteelfrommoltenpigiron.Inthe1950s,thistechnique

wasrenderedobsoletebytheLinz-Donawitzprocessofbasicoxygensteelmaking,which

limits impurities. Consequently, this technique uses a lot of electricity (about 440 kWh

permetricton).

2.7 Productspecificities

Key raw material inputs needed in steelmaking include iron ore, coal, limestone, and

recycledsteel.Ironoreisoneofthemostabundantmetallicelements.Coalisalsoakey

material in steel productions. Another major feature is the continuous improvement of

steelgrades.Indeed,50%oftodayssteelgradeswerenotavailabletenyearsago.

Coppercanbealloyedtotinoraluminum(tomakebronzes)orzinc(tomakebrass)to

form new characteristics and to improve its thermal and electric

conductivity. Copper is a natural metal than can easily be found in nature and is easily

recycled without any lost of its physical or chemical properties. Copper is energy and

thermalefficient,meaningheatandelectricitycancirculateincopperwiresmoreeasily

compared to other metals. Thus, copper has antimicrobial properties, which are much

appreciatedinthehealthcarefieldandfortransportingdrinkablewater.

3 Analysis

3.1 Economicanalysis

Because copper and steel are an input in almost all construction projects, the demand

tendstorisewhenthereisaconstructionupturninmainconsumingcountries.Also,ina

periodofaslackdemand(such as the mid-1980s and 1998-2002) there is an excess of

production over final demand, which results in an overload of stock. This abundance

makes these two markets rather different than other perishable commodities. In order

to moderate price fluctuation, the stocks and inventories are built up when demand is

lowandrundownwhenitishigh.

3.2 Positionofsteelandcopperininternationaltrade

Steel and copper are commodities like any other in the global economy, as they are

traded between producers and consumers. Price regulation of iron & steel was

abolished in 1992, since then steel prices are determined by the interplay of market

forces. The producers sell their actual or next production to customers, who transform

themetalsintoalloysorshapes,inordertoallowdownstreamfabricatorstotransform

Steel Production by Process

Crude steel production by process and region 2008

Crude steel production by process 2008

Sourcc Worid Stcci /..ociction.

M||||ons o metr|c tonnes lroduct|on 8es|c Oxygen lurnece L|ectr|c ^rc lurnece Open eerth lurnece

Luropeen 0n|on 19B.O 5B.2 41.5 O.3

ClS end Other Lurope 143.B 49.O 32.O 19.O

l^l1^ 123.4 42.2 5.B -

Centre| end South ^mer|ce 4B.3 o1. 3B.3 -

^r|ce 1.O 35.o o4.4 -

M|dd|e Lest 1o.3 12.1 B.9 -

Ch|ne 5O4.4 9O.9 9.1 -

lnd|e 55.2 4O.O 5B.2 1.B

Jepen 11B. 5.2 24.B -

lest o ^s|e 93.O 43.3 5o. -

Oceen|e B.4 9.B 2O.2 -

ruog

Sourcc Worid Stcci /..ociction.

1

2

3

8es|c Oxygen lurnece o

L|ectr|c ^rc lurnece 31

Open eerth lurnece 2

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

8

them into several end-use products. The settlement price is important to consider for

the present day (spot price) or for in the future. Copper can be traded over three

commodity exchanges: the SHME (traded in lots of 5 tons and quoted in Renminbi per

ton), the LME (traded in 25 tons lots and quoted in US dollars per ton), and the

COMEX/NYMEX (traded in lots of 25,000 pounds and quoted in US cents per pound).

Pricesaresetbyofferandbid,reflectingthemarketsperceptionofdemandandsupply.

In2008,steelstartedtobetradedasacommodityintheLME.Inordertofixapricein

the future and to provide a hedge against price variations, the exchanges also provide

futuresandoptioncontracts.

The following tables show that the current prices sit between cyclical low and high

prices since 2004 and that the copper market suffered less from the financial crisis in

2009.

3.3 Macroeconomicparameters

The demand of copper and steel boomed in 2004-2005 due to strong Chinese demand

and general economic upturn worldwide. Since 2000, several Indian and Chinese steel

firms entered the market like Shagang Groupe, Shangai Baosteel Groupe, Tata Steel

(which bought Cornus Group in 2007). Arcelormittal is the worlds largest steel

producer.Chinaisthetopproducerorsteelwithabout30%oftheglobalmarket.World

copperreserveshaveincreasedfrom90milliontonsin1950to280milliontonsin1970

and490milliontonsin2007.

3.4 Businessstructuresusuallyused

The mine supply growth, technological, economical and societal factors are related to

the supply and demand of copper. When an area needs more copper, new plants and

mines are built and existing ones expanded. In times of market surplus, the current

operations are scaled back or even closed down, and expansions are delayed or

canceled.

Credit Suisse 2009 Global Steel and Mining Conference 5

60

80

100

120

140

160

180

200

220

1/1/2009 3/1/2009 5/1/2009 7/1/2009

1 January 2009 = 100

Spot iron ore (62% Fe, fob)

Aluminium

Copper

Thermal coal (NEWC)

Source: LME, SBB, Reuters Ecowin

0 100 200 300 400 500

Aluminium

Copper

Thermal

coal

Iron ore *

Index (Low Price=100)

Current Spot

Cyclical High*

Cyclical Low*

* Iron ore CFR China,

prices from Dec 04

Source: SBB, LME, Energy Publishing

Cycle here is defined as the period from January 2004 to Mid 2008. Highs and

lows of monthly prices are taken.

!"##$%&'(#)*$+'+)&',$&-$$%'*.*/)*0/'/1-'0%2'3)43'

(#)*$+'+)%*$'5667

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

9

3.5 Majortradingpartnersoverallworldexports&imports

Thefollowingtableshowstheworldsteeltradebyarea

(source:Worldsteelinfigures,WorldSteelAssociation,2009)

24 25

Exporting

Region

Destination

E

u

r

o

p

e

a

n

U

n

io

n

(

2

5

)

O

t

h

e

r

E

u

r

o

p

e

C

I

S

N

A

F

T

A

O

t

h

e

r

A

m

e

r

ic

a

A

f

r

ic

a

a

n

d

M

id

d

le

E

a

s

t

C

h

in

a

J

a

p

a

n

O

t

h

e

r

A

s

ia

O

c

e

a

n

ia

T

o

t

a

l

Im

p

o

r

t

s

o

f

w

h

ic

h

:

e

x

t

r

a

-

r

e

g

io

n

a

l

im

p

o

r

t

s

European

Union (25)

127.7 4.6 15.9 1.9 2.1 0.6 11.1 0.4 4.8 0.2 169.3 41.6

Other Europe 10.8 0.1 9.3 0.0 0.1 0.0 0.6 0.1 0.3 0.0 21.3 21.3

CIS 1.8 2.6 9.7 0.0 0.5 0.0 1.5 0.1 0.3 0.0 16.6 6.9

NAFTA 6.4 0.2 2.5 16.7 4.4 0.2 4.5 2.6 4.6 0.3 42.4 25.7

Other America 1.3 0.0 1.8 1.3 4.6 0.1 2.0 0.5 0.7 0.0 12.3 7.7

Africa 4.2 0.2 4.7 0.2 0.5 2.2 1.9 0.4 1.1 0.0 15.3 13.2

Middle East 3.7 4.0 12.3 0.2 0.2 2.5 8.6 1.3 4.0 0.0 36.7 34.2

China 1.2 0.0 1.4 0.2 0.0 0.1 - 6.2 8.1 0.0 17.2 17.2

Japan 0.1 0.0 0.0 0.0 0.0 0.0 0.9 - 3.7 0.0 4.8 4.8

Other Asia 4.4 0.0 8.9 1.1 2.1 0.6 34.6 23.6 19.8 0.5 95.5 75.7

Oceania 0.3 0.0 0.0 0.0 0.0 0.0 0.6 0.5 1.0 0.4 2.8 2.5

Total Exports 161.8 11.6 66.4 21.7 14.4 6.4 66.4 35.6 48.5 1.5 434.3 250.7

of which:

extra-regional

exports*

34.1 11.6 56.7 5.0 9.8 1.7 66.4 35.6 28.7 1.1 250.7

Net Exports

(exports - imports)

-7.5 -9.7 49.8 -20.7 2.1 -45.7 49.2 30.9 -47.0 -1.4

* - excluding intra-regional trade marked

WORLD STEEL TRADE BY AREA

2007

million metric tons

MAJOR IMPORTERS AND

EXPORTERS OF STEEL

2007

Rank Total Exports

1 China 66.4

2 Japan 35.6

3 European Union (27)

1

34.1

4 Ukraine 30.3

5 Germany

2

29.9

6 Russia 29.4

7 Belgium - Luxembourg

2

26.6

8 South Korea 18.3

9 France

2

18.2

10 Italy

2

17.9

11 Taiwan, China 11.1

12 Netherlands

2

10.7

13 Brazil 10.4

14 United States 9.8

15 United Kingdom

2

9.5

16 Spain

2

8.0

17 Austria

2

7.0

18 Turkey 6.9

19 Canada 6.8

20 India 6.6

Rank Total Imports

1 European Union (27)

1

41.6

2 United States 27.7

3 Germany

2

27.4

4 South Korea 26.2

5 Italy

2

24.6

6 Belgium - Luxembourg

2

19.2

7 France

2

18.1

8 China 17.2

9 Spain

2

15.0

10 Turkey 13.5

11 Iran 12.2

12 Thailand 9.8

13 United Kingdom

2

9.3

14 Taiwan, China 9.2

15 Netherlands

2

8.8

16 Viet Nam 8.5

17 Poland

2

8.0

18 Canada 8.0

19 India 7.7

20 Russia 7.3

Rank Net Exports

(exports - imports)

1 China 49.2

2 Japan 30.9

3 Ukraine 28.1

4 Russia 22.1

5 Brazil 8.8

6 Belgium - Luxembourg

2

7.4

7 Austria

2

2.8

8 South Africa 2.5

9 Germany

2

2.4

10 Slovakia

2

2.3

11 Netherlands

2

1.9

12 Taiwan, China 1.9

13 Kazakhstan 1.2

14 Venezuela 0.7

15 Moldova 0.6

Rank Net Imports

(imports - exports)

1 United States 17.9

2 Iran 11.7

3 Viet Nam 8.3

4 South Korea 7.9

5 European Union (27)

1

7.5

6 Spain

2

7.1

7 Thailand 7.0

8 Italy

2

6.7

9 United Arab Emirates 6.6

10 Turkey 6.6

11 Saudi Arabia 4.2

12 Indonesia 4.2

13 Hong Kong, China 3.7

14 Philippines 3.4

15 Poland

2

3.1

1

Excluding intra-regional trade

2

Data for individual European Union (27) countries include intra-European trade

million metric tons

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! ;<<=!

Exporters

Peru

15%

Others

12%

ChiIe

36%

AustraIia

10%

Indonesia

9%

Canada

5%

P

N

G

3

%

BraziI 3%

A

rgentina 3%

M

o

n

g

o

Ii

a

2

%

S

.

A

f

r

i

c

a

2

%

Importers

Japan

23%

China

28%

B

u

I

g

a

r

i

a

3

%

F

i

n

I

a

n

d

3

%

B

r

a

z

i

I

3

%

Others

7%

Korean Rep.

8%

Spain

6%

P

h

iIip

p

in

e

s

3

%

Germany

6%

India

10%

Leading Exporters and Importers of Copper Ores and Concentrates, 2008

Percentage and thousand metric tonnes copper content

Source: CSG

"#$%&!'#'(%)!*+,-. "#$%&!'#'(%)!*+/*0

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

10

3.6 Marketfacts&figures

Inthelastcentury,thedemandforcopperhasincreasedfrom500thousandmetrictons

toover18millionmetrictonsin2007asdemandoverthisperiodgrewbyanaverageof

4%/year.From1960until2006demandforcopperinAsiajumpedfrom455thousand

metrictonstoaround8000thousandmetricton.Theaverageannualgrowthrateofthe

coppermarketsince1900is4%.Chilehasincreaseditsproductionofcopperfrom14%

in 1960 to 36% in 2006, making South America the biggest producer worldwide. Chile

contains5ofthetop10and8ofthetop20copperminesbycapacityintheworld.

The following table shows the geographical distribution of steel production and use in

2008:

(source:Worldsteelinfigures,WorldSteelAssociation,2009)

Fordetails,pleaserefertotheattachedstatistics&tables.

3.7 Extentofinternationalintegration

New steel futures contracts introduced in 2008 in the LME have filled an information

gap and extend the international integration of the steel market. However, some major

producers have said that industry consolidation is a better way forward than futures

contracts,whichenablethesteelindustrytohedgeagainstvolatilityinsteelprices.

4 Potentialoutcomes

This paper could help an investor looking for opportunities in the steel or copper

market. Based on the information available in this document, he would be able to

compare the two markets and make up his choice for an investment responding to his

needs. The steel market is probably attractive on a short-term basis, due to the new

derivates available on the LME and the particular low prices. The copper market will

probablybelessspeculativeinthenextmonthandwouldprobablybemoreadaptedon

a long-term investment, as copper will stay a key material for future economic

developmentworldwide.

14 15

STEEL PRODUCTION AND USE:

GEOGRAPHICAL DISTRIBUTION

2008

Production

Use (nished steel products)

World total: 1,327 million metric tons crude steel

Others comprise:

Africa 1.3%

Middle East 1.3%

Central and South America 3.7%

Australia and New Zealand 0.6%

Others comprise:

Africa 2.2%

Middle East 3.6%

Central and South America 3.7%

Australia and New Zealand 0.8%

STEEL PRODUCTION AND USE:

GEOGRAPHICAL DISTRIBUTION

1998

Others comprise:

Africa 1.6 %

Middle East 1.2 %

CIS

3.5%

Other Europe

2.5%

China

16.0%

NAFTA

21.4%

Japan

10.2%

Other Asia

13.9%

EU (27)

22.7%

Others

9.8%

CIS

4.2%

Other Europe

2.4%

China

35.5%

NAFTA

10.8%

Japan

6.4%

Other Asia

15.2%

EU (27)

15.2%

Others

10.2%

CIS

9.5%

Other Europe

2.2%

China

14.7%

NAFTA

16.6%

Japan

12.0%

Other Asia

11.5%

Others

8.9% EU (27)

24.6%

CIS

8.6%

Other Europe

2.4%

China

37.7%

NAFTA

9.3%

Japan

9.0%

Other Asia

11.2%

EU (27)

14.9%

Others

6.8%

Use (nished steel products)

World total: 777 million metric tons crude steel

Production

Central and South America 4.8 %

Australia and New Zealand 1.2 %

Others comprise:

Africa 2.2%

Middle East 2.4%

Central and South America 4.0%

Australia and New Zealand 1.2%

World total: 692 million metric tons

World total: 1,198 million metric tons

14 15

STEEL PRODUCTION AND USE:

GEOGRAPHICAL DISTRIBUTION

2008

Production

Use (nished steel products)

World total: 1,327 million metric tons crude steel

Others comprise:

Africa 1.3%

Middle East 1.3%

Central and South America 3.7%

Australia and New Zealand 0.6%

Others comprise:

Africa 2.2%

Middle East 3.6%

Central and South America 3.7%

Australia and New Zealand 0.8%

STEEL PRODUCTION AND USE:

GEOGRAPHICAL DISTRIBUTION

1998

Others comprise:

Africa 1.6 %

Middle East 1.2 %

CIS

3.5%

Other Europe

2.5%

China

16.0%

NAFTA

21.4%

Japan

10.2%

Other Asia

13.9%

EU (27)

22.7%

Others

9.8%

CIS

4.2%

Other Europe

2.4%

China

35.5%

NAFTA

10.8%

Japan

6.4%

Other Asia

15.2%

EU (27)

15.2%

Others

10.2%

CIS

9.5%

Other Europe

2.2%

China

14.7%

NAFTA

16.6%

Japan

12.0%

Other Asia

11.5%

Others

8.9% EU (27)

24.6%

CIS

8.6%

Other Europe

2.4%

China

37.7%

NAFTA

9.3%

Japan

9.0%

Other Asia

11.2%

EU (27)

14.9%

Others

6.8%

Use (nished steel products)

World total: 777 million metric tons crude steel

Production

Central and South America 4.8 %

Australia and New Zealand 1.2 %

Others comprise:

Africa 2.2%

Middle East 2.4%

Central and South America 4.0%

Australia and New Zealand 1.2%

World total: 692 million metric tons

World total: 1,198 million metric tons

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

11

5 Personalassessment

TheSWOTanalysisisanadequateinstrumenttoassessandcomparethetwomarkets

SWOTSTEELMARKET

Strength Opportunities

-Stabilityinsomeemergingeconomies

-StrongCO2emissionsmeasures

-Globalpolicy&perspective(GSSA)

-Export-facilitatingmeasures

-Non-tariffbarriersinemergingAsia

-Modern steelmaking with advanced

technologies

Weakness Threats

- The economic crisis has pushed the

industryintorecession

- Construction sector accounts for half of

worlddemand

- Will demand go down when the stimulus

ends?

- Overcapacity: steelmaking capacity

continuing to increase despite the market

downturns

- Uncertainties regarding public

constructionactivity

SWOTCOPPERMARKET

Strength Opportunities

-Shippingcostsnotanissuenow

-Easilyrecyclable

-Energyefficient(goodconductivity)

-Emergingmarkets

-Economyrecovery

-Healthcare(antimicrobialproperties)

Weakness Threats

-Marketpower/concentration

-Coalusedformining(CO2emissions)

-Watersupplyindryminingdistricts

-Fallingoresgrades(USA,Chile)

- Project finance: high interest rates may

reduceinvestments

-Capitalcostoverruns(USdollarinflation)

6 Prospects

TheglobaltrendintheUEandtheUSAisonconsolidationofindustry.Thefocusisnow

on technological improvement and new products. The Chinese steel industry seems to

be currently staggering, but considering its population of 1.3 billion people; the per

capitasteelconsumptionisbelowthanintheEUortheUSA.Chinahasrecentlybecome

anetexporterofsteel,meaningthatChinaalsoreachedalevelofproductionsaturation

and it steels industry needs to be consolidated and reorganized in coming years rather

thananexpanded.

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

12

7 Conclusion

The steel and copper markets are often considered as being indicators of economic

progress, because of their critical role played in infrastructures and overall

development.Thevolumeofsteelandcopperconsumedisagoodbarometertomeasure

development and economic progress, as they are both basic raw materials. The intense

use of copper relates to the demand and consumption in economic activity. When less

developed regions expand their infrastructure the price goes up. Indeed, both raw

materialsareinputsintomajorindustriesinmaincountriesworldwide.

Like other markets, which have a perfect competitive structure, there is a homogenous

product and the global price is determined by the supply and demand. In both cases

copper and steel markets are in perfect competition, because there are very large

producersandconsumers.However,inbothcasestheglobalmarketislarge,compared

to the output of even the biggest company (each firm is a price-taker). Thus, both steel

andcoppercanbeproducedinmanypartsoftheglobe.

Bothindustrieshavetofacetheenvironmentalissuesandthesustainabledevelopment

challenge for the coming years. They will also have to face reduction in workforce, as

theywillnotbelabor-intensiveindustryastheyusedtobe.

Summing up, as both markets are closely linked to the economic and industrial

development worldwide, they will benefit from the global economy recover which

should happen in the year 2010. Therefore, they will stay attractive to investors on a

long-term basis and this way it is certain that it will contribute to the development of

societywellintothefuture.

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

13

Bibliography

Worldsteelinfigures,WorldSteelAssociation,2009,ISSN:1379-9746,27p.

TheWorldCopperFactbook2009,InternationalCopperStudyGroup,2009,67p.

Latribunedesmtaux,Veron&Cie,novembredcembre2009,ESSN1167.4849

SafeSustnainableSteel,ArcelorMittalFactbook2008,publishedinJune2009,126p.

Economics - Eleventh Edition, Lipsey & Chrystal, Oxford University Press 2007, 665 p.,

ISBN978-0-19-928641-6

La Chine influence plus que jamais le march de lacier, Eric Louvet, in Le Temps

31.08.09

Consultedwebsites:

http://www.trademap.org(04.01.10)

http://stats.oecd.org(04.01.10)

http://www.intracen.org(04.01.10)

http://stat.wto.org(04.01.10)

http://www.ft.com(04.01.10)

http://europe.wsj.com(04.01.10)

http://www.letemps.ch(04.01.10)

https://www.cia.gov/library/publications/the-world-factbook(04.01.10)

Contactedreferenceofexpertise:

Mr.EricLouvet,SeniorAdvisorMetals&MiningBNPParibas(Suisse)SA,Geneva.

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

14

Attachments

Tableofcontent

Annualsteelprices,Europep.15

Copperstocks,pricesandusage..p.15

Apparentsteelusepercapita2002to2008p.16

Intensityofrefinedcopperuse2008p.17

Worldcrudesteelproduction2008inmillionsofmetrictones..p.17

Crudesteelproductionbyprocessandregion2008..p.17

Copperproductionandusagebycountry,2008p.18

Topsteel-producingproducingcompanies2007and2008..p.18

Majorsteel-producingcountries2007and2008..p.18

Top20copperminesbycapacity2009..p.19

Top20copperfabricatingplantsbycapacity2008p.19

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

15

Statistics&tables

Annual steel prices, Europe*

Steel Prices continucd

Metr|c tonnes 1999 2OOO 2OO1 2OO2 2OO3 2OO4 2OO5 2OOo 2OO 2OOB

ClS S|eb Lxport (0SLJt) 145 14 132 1B3 23 45O 3B 3B2 49B 5o

Chcnc yccr,yccr -12 20 -24 39 29 90 -16 1 30 52

ClS 8|||et Lxport (0SLJt) 155 1o2 144 1o5 215 345 33 3B1 4B9 45

Chcnc yccr,yccr -16 4 -11 15 31 60 -2 13 2B 52

lC Cermen Lomest|c (L0lJt) 23o 31 25B 2o 3O9 443 45O 4o4 4BB o3O

lC Cermen Lomest|c (0SLJt) 251 293 231 2o1 35O 551 5o1 5B3 oo9 92

Chcnc yccr,yccr -1 1 -21 13 34 5B 2 4 15 39

ClC Cermen Lomest|c (L0lJt) 314 435 349 3o 39 52B 552 5o1 55B oBO

ClC Cermen Lomest|c (0SLJt) 334 4O2 312 34 45O o5 oBB O5 o5 1,OO1

Chcnc yccr,yccr -1 20 -22 11 30 46 5 2 9 31

LC Cermen Lomest|c (L0lJt) 35 42 3o2 34 414 53B 55B o42 o5o 2o

LC Cermen Lomest|c (0SLJt) 399 43o 324 355 4oB oO o9 BO9 9OO 1,Oo

Chcnc yccr,yccr -23 9 -26 10 32 43 4 16 11 19

l|ete Cermen Lomest|c (L0lJt) 22 34 3B1 3o2 39o 493 o19 o49 43 B39

l|ete Cermen Lomest|c (0SLJt) 2B9 319 341 343 449 o13 O B1o 1,O1B 1,234

Chcnc yccr,yccr -2 10 1 31 3 26 6 25 21

W|re rod Cermen Lomest|c (L0lJt) 224 254 245 2o4 292 435 3B 424 45 o21

W|re rod Cermen Lomest|c (0SLJt) 23B 235 22O 25O 331 54O 42 534 o2 913

Chcnc yccr,yccr -10 -1 - 14 32 63 -13 13 1 46

Merchent bers Cermen Lomest|c (L0lJt) 2o2 2Bo 293 3OB 333 393 414 524 5B 32

Merchent bers Cermen Lomest|c (0SLJt) 29 2o4 2o3 291 3 4B9 515 o59 92 1,O

Chcnc yccr,yccr -11 -5 -1 11 30 30 5 2B 20 36

Sect|ons Cermen Lomest|c (L0lJt) 2B4 315 31O 31B 35O 495 5O9 552 o5B B1B

Sect|ons Cermen Lomest|c (0SLJt) 3O2 291 2B 3O1 39 o1o o34 o94 9O2 1,2O3

Chcnc yccr,yccr -14 -4 -4 B 32 55 3 9 30 33

Sourcc CRU, 1|X rcport, Mctci Buiictin cnd /rcciorMittci ctimctc.

Currcncy convcrion bccd on cvcrcc cxchcnc rctc.

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! ;<<=!

Copper Stocks, Prices and Usage

Thousand metric tonnes copper and US cents/pound

Source: CSG

0

75

150

225

300

375

450

525

600

675

750

825

900

975

1,050

1,125

1,200

1,275

1,350

1,425

1,500

1,575

1,650

1,725

1,800

1,875

1,950

2,025

2,100

2,175

2,250

2,325

2,400

2,475

2,550

2,625

2,700

2,775

2,850

2,925

3,000

Jan 00 Jul 00 Jan 01 Jul 01 Jan 02 Jul 02 Jan 03 Jul 03 Jan 04 Jul 04 Jan 05 Jul 05 Jan 06 Jul 06 Jan 07 Jul-07 Jan 08 Jul-08 Jan 09

T

h

o

u

s

a

n

d

m

e

t

r

i

c

t

o

n

n

e

s

,

c

o

p

p

e

r

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

260

270

280

290

300

310

320

330

340

350

360

370

380

390

400

P

r

i

c

e

L

M

E

(

U

S

c

e

n

t

s

/

p

o

u

n

d

)

Exchanges Producers

Merchants Consumers

Price LME (UScents/pound) 3 mth moving average copper usage seasonally adjusted

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

16

16 17

APPARENT STEEL USE PER CAPITA

2002 TO 2008

kilograms nished steel products

APPARENT STEEL USE

2002 TO 2008

2002 2003 2004 2005 2006 2007 2008

Austria 3.1 3.1 3.3 3.5 4.1 4.1 4.0

Belgium - Luxembourg 4.5 4.0 4.8 4.6 5.5 5.8 5.6

Czech Republic 4.2 4.4 5.2 5.2 6.0 6.6 6.5

France 17.2 15.6 16.7 14.8 16.2 16.6 15.3

Germany 31.6 31.9 36.3 35.3 39.2 42.7 41.5

Italy 29.5 31.8 33.2 31.6 36.6 36.6 34.3

Netherlands 4.0 3.4 3.5 3.6 3.5 3.5 3.2

Poland 7.7 7.3 8.5 8.4 10.7 12.1 11.4

Romania 2.8 3.1 3.3 3.5 4.2 5.1 4.3

Spain 19.7 21.0 21.1 20.9 23.6 24.5 19.6

Sweden 3.3 3.6 4.0 4.1 4.5 4.8 4.9

United Kingdom 12.6 12.3 13.2 11.4 12.9 12.7 11.7

Other EU (27) 18.5 18.5 19.5 18.6 21.7 23.0 20.0

European Union (27) 158.7 160.1 172.4 165.5 188.6 198.1 182.1

Turkey 12.3 14.6 16.2 18.5 21.3 23.6 21.3

Others 5.3 5.3 6.4 6.6 7.7 8.0 7.6

Other Europe 17.5 19.9 22.6 25.1 28.9 31.6 28.9

Russia 24.9 25.3 26.3 29.3 34.9 40.4 35.4

Ukraine 5.5 6.4 5.8 5.6 6.7 8.3 6.9

Other CIS 3.5 0.7 0.8 0.8 1.0 1.3 1.3

CIS 34.0 37.0 38.1 41.5 48.9 56.6 49.9

Canada 15.9 15.5 17.4 16.8 18.1 15.5 15.0

Mexico 14.3 14.9 16.0 16.1 18.0 17.8 17.3

United States 107.3 100.8 117.4 105.4 119.6 108.0 97.5

NAFTA 137.5 131.3 150.8 138.3 155.7 141.3 129.7

Argentina 1.7 2.8 3.6 3.7 4.5 4.6 4.8

Brazil 16.5 16.0 18.3 16.8 18.5 22.1 24.0

Venezuela 1.6 1.5 2.4 2.7 3.1 4.0 3.3

Others 7.7 7.1 8.6 9.1 10.1 11.0 12.1

Central and South America 27.7 27.6 33.0 32.5 36.4 41.9 44.4

Egypt 5.5 4.2 3.8 5.0 4.6 5.5 6.5

South Africa 4.9 4.1 4.9 4.7 6.0 6.0 6.1

Other Africa 8.7 10.0 11.1 11.9 12.2 13.6 13.5

Africa 19.1 18.3 19.9 21.5 22.9 25.1 26.2

Iran 11.3 14.7 14.5 15.6 14.6 16.1 15.6

Other Middle East 12.9 14.2 15.2 17.9 20.3 24.2 27.5

Middle East 24.1 28.9 29.8 33.5 34.9 40.3 43.1

China 191.3 240.5 275.8 340.2 369.8 413.7 425.7

India 30.7 33.1 35.3 39.9 45.6 49.5 52.6

Japan 71.7 73.4 76.8 76.7 77.3 79.6 76.4

South Korea 43.7 45.4 47.2 47.1 50.2 55.2 58.6

Taiwan, China 20.4 19.9 22.1 19.9 19.8 18.1 16.7

Other Asia 41.6 41.9 45.8 50.2 47.4 55.2 54.6

Asia 399.4 454.2 503.0 574.1 610.1 671.3 684.6

Australia and New Zealand 7.2 7.5 8.0 7.9 7.9 8.6 9.2

World 825.2 884.7 977.6 1,040.0 1,134.4 1,214.8 1,198.1

2002 2003 2004 2005 2006 2007 2008

Austria 384.0 382.1 399.6 419.4 492.9 495.7 472.2

Belgium - Luxembourg 417.9 375.1 440.3 423.6 505.1 530.6 510.6

Czech Republic 409.6 432.7 508.1 513.7 585.9 644.6 639.3

France 287.7 259.2 275.5 243.4 263.5 269.6 247.4

Germany 383.4 386.6 438.8 426.6 474.6 517.2 502.4

Italy 507.6 545.7 567.8 538.8 622.7 621.6 582.0

Netherlands 246.8 210.3 216.7 221.9 215.0 211.5 191.5

Poland 200.7 190.6 221.4 219.2 279.5 316.5 299.6

Romania 129.5 141.1 149.6 161.8 195.1 235.5 200.4

Spain 475.7 497.8 493.3 481.8 538.6 552.6 440.5

Sweden 366.0 398.0 444.3 453.8 492.2 531.6 532.2

United Kingdom 212.0 206.3 219.7 189.4 212.4 209.1 191.4

Other EU (27) 265.6 265.5 279.4 265.6 309.7 328.2 284.6

European Union (27) 327.0 328.6 352.8 337.5 383.5 401.9 368.9

Turkey 174.8 205.3 224.7 254.1 287.8 314.6 281.2

Others 140.3 141.3 170.1 174.1 203.3 214.3 202.4

Other Europe 163.0 183.6 206.4 227.4 259.8 281.6 255.4

Russia 170.6 174.2 181.7 203.2 243.8 283.4 249.6

Ukraine 115.5 134.7 121.9 118.5 144.3 179.7 151.2

Other CIS 51.8 27.8 31.1 30.4 37.7 47.4 47.6

CIS 129.9 141.9 146.7 160.2 189.2 219.6 194.2

Canada 508.0 490.4 543.9 521.9 556.1 471.7 451.5

Mexico 140.5 145.7 155.0 154.0 171.1 167.3 160.2

United States 368.8 343.2 395.4 351.4 394.9 353.1 315.6

NAFTA 324.3 306.8 348.9 316.9 353.4 317.4 288.4

Argentina 46.4 74.8 93.3 95.5 114.7 116.9 119.9

Brazil 92.0 87.8 99.4 90.0 97.9 115.2 123.6

Venezuela 63.4 57.3 91.3 101.0 113.8 143.9 118.3

Others 46.5 42.5 50.4 52.8 58.2 62.4 67.4

Central and South America 66.5 65.3 77.2 74.8 82.9 94.1 98.4

Egypt 80.2 59.5 53.7 68.2 62.1 72.4 85.1

South Africa 104.6 87.3 104.0 97.6 125.0 123.3 124.7

Other Africa 14.9 17.7 18.1 19.9 19.7 21.8 20.9

Africa 29.7 28.1 28.9 31.5 32.7 35.3 36.0

Iran 167.1 216.1 211.5 225.4 208.5 226.1 216.0

Other Middle East 153.8 165.3 172.5 197.1 217.9 253.9 280.7

Middle East 159.7 187.7 189.6 209.3 213.8 242.0 253.3

China 148.5 185.4 211.4 259.1 280.0 311.4 318.5

India 28.4 30.1 31.6 35.2 39.6 42.4 44.3

Japan 562.4 575.2 600.9 599.9 604.4 622.0 597.2

South Korea 924.6 955.4 990.3 984.4 1 044.2 1 144.8 1 210.4

Taiwan, China 907.4 878.4 969.3 869.7 860.4 780.1 717.8

Other Asia 48.4 48.0 51.8 56.0 52.0 59.7 58.3

Asia 116.6 131.0 143.5 162.0 170.3 185.4 187.1

Australia and New Zealand 298.1 308.3 327.0 321.2 315.8 340.7 359.3

World 140.0 148.4 162.1 170.7 184.1 195.1 190.4

million metric tons nished steel products

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

17

31! lnLernaLlonal Copper SLudy Croup

1he World Copper lacLbook 2009

Africa

China

EU-27

Japan

Latin America (ex Mexico)

MiddIe East

North America

Oceania

Russian Fed.

ASEAN-5

India

United States

0

1

2

3

4

5

6

7

8

9

10

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

GDP per Capita (2008 US$/person)

R

e

f

i

n

e

d

C

o

p

p

e

r

U

s

a

g

e

p

e

r

C

a

p

i

t

a

(

k

g

/

p

e

r

s

o

n

)

Intensity of Refined Copper Use, 2008

1

Sources: CSG, nternational Monetary Fund, U.S. Census Bureau

1

noLe: 8eflned copper ls consumed by semls fabrlcaLors or Lhe flrsL users" of reflned copper, lncludlng lngoL makers, masLer alloy planLs, wlre rod planLs, brass mllls, alloy

wlre mllls, foundrles and foll mllls. As a resulL, per caplLa consumpLlon of reflned copper refers Lo Lhe amounL of copper consumed by lndusLry dlvlded by Lhe LoLal domesLlc

populaLlon and does noL represenL consumpLlon of copper ln flnlshed producLs per person.

World crude steel production 2008 in millions of metric tonnes

Sourcc Worid Stcci /..ociction.

Steel Production by Process

Crude steel production by process and region 2008

Crude steel production by process 2008

Sourcc Worid Stcci /..ociction.

M||||ons o metr|c tonnes lroduct|on 8es|c Oxygen lurnece L|ectr|c ^rc lurnece Open eerth lurnece

Luropeen 0n|on 19B.O 5B.2 41.5 O.3

ClS end Other Lurope 143.B 49.O 32.O 19.O

l^l1^ 123.4 42.2 5.B -

Centre| end South ^mer|ce 4B.3 o1. 3B.3 -

^r|ce 1.O 35.o o4.4 -

M|dd|e Lest 1o.3 12.1 B.9 -

Ch|ne 5O4.4 9O.9 9.1 -

lnd|e 55.2 4O.O 5B.2 1.B

Jepen 11B. 5.2 24.B -

lest o ^s|e 93.O 43.3 5o. -

Oceen|e B.4 9.B 2O.2 -

ruog

Sourcc Worid Stcci /..ociction.

1

2

3

8es|c Oxygen lurnece o

L|ectr|c ^rc lurnece 31

Open eerth lurnece 2

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

18

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! ;<<=!

Mine

Production

Refined

Production

Refined

Usage

Mine

Production

Refined

Production

Refined

Usage

Mine

Production

Refined

Production

Refined

Usage

Argentina 157 16 30 Iran 248 201 135 PoIand 429 527 247

AustraIia 883 502 151 ItaIy 24 635 PortugaI 89 2

Austria 107 33 Japan 1,540 1,184 Romania 5 15 36

BeIgium 396 285 Kazakhstan 420 398 56 Russian Fed. 705 862 650

Botswana 29 Korea, North 12 15 15 Saudi Arabia 1 192

BraziI 212 223 375 Korea, South 531 780 Serbia 19 34 37

BuIgaria 105 127 59 Laos 89 64 South Africa 109 93 86

Canada 607 442 197 MaIaysia 177 Spain 7 319 385

ChiIe 5,328 3,058 103 Mauritania 33 Sweden 57 228 170

China 951 3,791 5,198 Mexico 247 295 325 Taiwan (China) 582

CoIombia 1 10 10 MongoIia 129 3 Tanzania 4

Congo, Dem Rep 214 64 Morocco 5 ThaiIand 0 240

Czech RepubIic 6 Myanmar 0 0 Turkey 83 88 360

Egypt 4 170 Namibia 9 Ukraine 20 20

FinIand 13 131 67 NetherIands 22 United Arab Emirates 36

France 410 Norway 37 United Kingdom 54

Germany 690 1,398 Oman 20 25 15 United States 1,335 1,282 2,020

Greece 75 Pakistan 20 41 Uzbekistan 80 90 48

Hungary 8 Papua New Guinea 160 Vietnam 11 2 102

India 28 662 520 Peru 1,268 464 55 Zambia 547 417 29

Indonesia 651 254 195 PhiIippines 21 175 39 Zimbabwe 3 7 10

Copper Production and Usage by Country, 2008

Thousand metric tonnes

Source: CSG

8 9

MAJOR STEEL-PRODUCING COUNTRIES

2007 AND 2008

million metric tons crude steel production

Country 2008 2007

China 1 500.5 1 494.9

Japan 2 118.7 2 120.2

United States 3 91.4 3 98.1

Russia 4 68.5 4 72.4

India (e) 5 55.2 5 53.1

South Korea 6 53.6 6 51.5

Germany 7 45.8 7 48.6

Ukraine 8 37.1 8 42.8

Brazil 9 33.7 9 33.8

Italy 10 30.6 10 31.6

Turkey 11 26.8 11 25.8

Taiwan, China 12 19.9 12 20.9

Spain 13 18.6 14 19.0

France 14 17.9 13 19.2

Mexico 15 17.2 15 17.6

Canada 16 14.8 16 15.6

United Kingdom 17 13.5 17 14.3

Belgium 18 10.7 18 10.7

Iran 19 10.0 20 10.1

Poland 20 9.7 19 10.6

South Africa 21 8.3 21 9.1

Australia 22 7.6 22 7.9

Austria 23 7.6 23 7.6

Netherlands 24 6.9 24 7.4

Czech Republic 25 6.4 25 7.1

Egypt 26 6.2 28 6.2

Malaysia (e) 27 6.1 26 6.9

Argentina 28 5.5 31 5.4

Thailand (e) 29 5.5 30 5.6

Sweden 30 5.2 29 5.7

Romania 31 5.0 27 6.3

Saudi Arabia 32 4.7 35 4.6

Slovak Republic 33 4.5 32 5.1

Finland 34 4.4 36 4.4

Kazakhstan 35 4.3 34 4.8

Venezuela 36 4.2 33 5.0

Indonesia (e) 37 3.6 37 4.0

Luxembourg 38 2.6 38 2.9

Byelorussia 39 2.6 40 2.4

Greece 40 2.5 39 2.6

Viet Nam (e) 41 2.2 42 2.0

Hungary 42 2.1 41 2.2

Others 24.3 24.3

World 1,326.5 1,351.3

(e): estimate

TOP STEEL-PRODUCING COMPANIES

2007 AND 2008

million metric tons crude steel production

2008 2007 2008 2007

1 103.3 1 116.4 ArcelorMittal 41 6.9 40 7.4 Jiuquan Steel

2 37.5 2 35.7 Nippon Steel

1

42 6.9 41 7.3 Salzgitter

5

3 35.4 5 28.6 Baosteel Group 43 6.8 43 6.9 voestalpine

4 34.7 4 31.1 POSCO 44 6.5 39 7.8 Jianlong Group

5 33.3 NA 31.1 Hebei Steel Group 45 6.5 44 6.8 BlueScope

6 33.0 3 34.0 JFE 46 6.4 46 6.4 Metalloinvest

7 27.7 11 20.2 Wuhan Steel Group 47 6.4 47 6.4 Beitei Steel

8 24.4 6 26.5 Tata Steel

2

48 6.1 60 5.2 Guofeng Steel

9 23.3 8 22.9 Jiangsu Shagang Group 49 6.1 51 6.1 SSAB

10 23.2 10 21.5 U.S. Steel 50 6.0 58 5.4 Erdemir

11 21.8 NA 23.8 Shandong Steel Group 51 5.9 54 5.9 AK Steel

12 20.4 12 20.0 Nucor 52 5.9 52 6.1 Mechel

13 20.4 13 18.6 Gerdau 53 5.7 53 6.0 Nanjing Steel

14 19.2 15 17.3 Severstal 54 5.6 42 7.0 Ilyich

15 17.7 17 16.2 Evraz 55 5.4 61 5.0 Tonghua Steel

16 16.9 14 17.9 Riva 56 5.3 56 5.6 Xinyu Steel

17 16.0 NA 16.2 Anshan Steel 57 5.2 57 5.5 HKM

6

18 15.9 16 17.0 ThyssenKrupp

3

58 5.1 NA 4.5 Sanming Steel

19 15.0 18 14.2 Maanshan Steel 59 5.0 59 5.3 CSN

20 14.1 20 13.8 Sumitomo Metal Ind 60 4.7 63 4.6 HADEED

21 13.7 19 13.9 SAIL 61 4.5 68 4.4 Tianjin Tiantie Group

22 12.2 23 12.9 Shougang Group 62 4.4 72 4.0 Hebei Jinxi Group

23 12.0 21 13.3 Magnitogorsk 63 4.3 62 5.0 Steel Dynamics

24 11.3 30 9.7 Novolipetsk 64 4.3 69 4.1 Pingxiang Steel

25 11.3 26 11.1 Hunan Valin Group 65 4.3 65 4.5 Ezz Group

26 11.0 27 10.9 China Steel Corporation 66 4.0 71 4.1 Nisshin

27 10.4 22 13.1 Techint

4

67 4.0 70 4.1 Tianjin Steel Pipe

28 10.0 28 10.1 IMIDRO 68 3.9 64 4.6 Zaporizhstahl

29 9.9 NA 11.6

Industrial Union

of Donbass

69 3.8 NA 3.0 JSW Steel

30 9.9 29 10.0 Hyundai Steel 70 3.7 73 4.0 Lion Group

31 9.8 34 8.8 Baotou Steel 71 3.7 75 3.5 AHMSA

32 9.2 31 9.3 Taiyuan Steel 72 3.7 NA 3.0 ICDAS

33 9.0 33 9.0 Anyang Steel 73 3.6 NA 4.3 SIDOR

6

34 8.2 32 9.1 Metinvest 74 3.6 78 3.5 Hangzhou Steel

35 8.2 37 8.1 Celsa 75 3.5 NA 2.7 Hebei Jingye Steel

36 8.1 38 8.1 Kobe Steel 76 3.5 77 3.5 Chongqing Steel

37 8.0 35 8.7 Usiminas 77 3.4 NA 2.7 Commercial Metals

38 7.5 45 6.6 Panzhihua Steel 78 3.4 74 3.6 Essar Steel

39 7.5 50 6.2 Rizhao Steel 79 3.4 79 3.5 Tokyo Steel

40 7.4 NA 7.6 Benxi Steel 80 3.1 NA 3.2 Vizag Steel

(1) - includes part of Usiminas

(2) - includes Corus

(3) - 50% of HKM included in ThyssenKrupp

(4) - includes partial tonnage of SIDOR

(5) - includes part of HKM

(6) - total production

NA: not applicable

Comparetheworldsteelandcoppermarkets:similaritiesanddifferences

AlainMermoudMScBA20104January2010

19

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! #;;<!

Rank Mine Country Owner(s) Source Capacity

1 Escondida Chile BHP Billiton (57.5%), Rio Tinto Corp. (30%), Japan Escondida (10%), FC

(2.5%)

Concs & SX-EW 1,330

2 Codelco Norte Chile Codelco Concs & SX-EW 900

3 Grasberg ndonesia P.T. Freeport ndonesia Co. (PT-F), Rio Tinto Concentrates 750

4 Collahuasi Chile Anglo American (44%), Xstrata plc (44%), Mitsui + Nippon (12%) Concs & SX-EW 498

5 El Teniente Chile Codelco Chile Concentrates 440

6 Taimyr Peninsula (Norilsk/

Talnakh Mills)

Russia Norilsk Nickel Concentrates 430

7 Antamina Peru BHP Billiton (33.75%), Teck (22.5%), Xstrata plc (33.75%), Mitsubishi (10%) Concentrates 420

8 Morenci United States Freeport-McMoRan Copper & Gold nc./Sumitomo SX-EW 400

9 Los Pelambres Chile Antofagasta Holdings (60%), Nippon Mining (25%), Mitsubishi Materials

(15%)

Concentrates 360

10 Bingham Canyon United States Kennecott Concentrates 280

10 Batu Hijau ndonesia PT Pukuafu ndah (20%), Newmont (45%), Sumitomo Corp. (27.5%),

Sumitomo Metal Mining (5%), Mitsubishi Materials (2.5%)

Concentrates 280

12 Kansanshi Zambia First Quantum Minerals Ltd (80%), ZCCM (20%) Concs & SX-EW 270

13 Andina Chile Codelco Chile Concentrates 250

14 Zhezkazgan Complex Kazakhstan Kazakhmys (Samsung) Concentrates 230

15 Los Bronces Chile Anglo American (100%) Concs & SX-EW 228

16 Olympic Dam Australia BHP Billiton Concs & SX-EW 225

17 Rudna Poland KGHM Polska Miedz S.A. Concentrates 220

18 Cananea Mexico Grupo Mexico Concs & SX-EW 210

19 Sarcheshmeh ran National ranian Copper ndustry Co. Concs & SX-EW 204

20 Bajo de la Alumbrera Argentina Xstrata plc 50%, Goldcorp nc 37.5%, Yamana Gold 12.5% Concentrates 200

Top 20 Copper Mines by Capacity, 2009

Thousand metric tonnes

Source: CSG

!

"#! $%&'(%)&*+%),!-+..'(!/&012!3(+0.!!!

!

45'!6+(,1!-+..'(!7)8&9++:! #;;<!

Rank Owners PIant Country PIant Type Capacity

1 Wieland Werke (Wieland Metals) Vhringen Germany Brass mill 360

2 Freeport McMoRan Copper & Gold nc. El Paso, TX USA Wire rod plant 355

2 Freeport McMoRan Copper & Gold nc. Norwich, CT USA Wire rod plant 355

4 Conticon (Condumex - Grupo Carso) Celaya Mexico Wire rod plant 318

5 Southwire Carollton, GA USA Wire rod plant 310

6 Jinagsu Jinhui Copper Group Jinagsu Jinhui Copper Group China Wire rod plant 300

6 Nanjing Walsin Wire & Cable Nanjing China Wire rod plant 300

6 SCCC - Societe de Coulee Continue de Cuivre (Nexans) Chauny France Wire rod plant 300

6 Trafilierie Carlo Gnutti Chiari, Brescia taly Brass mill 300

10 Hitachi Wire Rod (Hitachi Cable 70%; Pan Pacific 20%) baraki-Ken Japan Wire rod plant 280

10 Cumerio (Aurubis) Olen (Plant 1) Belgium Wire rod plant 280

12 Aurubis Hamburg Germany Wire rod plant 275

13 Asarco (Grupo Mexico) Amarillo, TX USA Wire rod plant 270

13 LS Cable Gumi Korea Wire rod plant 270

15 Katur-nvest (Uralelektromed) Verkhnaya Pyshma Russia Wire rod plant 265

16 Nexans Canada nc. (Nexans 100%) Montreal Canada Wire rod plant 260

17 Nanjin Walsin Nanjin Walsin China Wire rod plant 250

17 Taihan Electric Wire Anyang Korea Wire rod plant 250

19 Deutsche Giessdraht (Aurubis 60%, Codelco 40%) Emmerich Germany Wire rod plant 250

19 MKM Mansfelder Kupfer & Messing (Kazakhmys) Hettstedt Germany Brass mill 250

Top 20 Copper Fabricating PIants by Capacity, 2008

Thousand metric tonnes

Source: CSG

S-ar putea să vă placă și

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Coatings For High Temperature ApplicationsDocument91 paginiCoatings For High Temperature ApplicationssupendiÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Certificado de Cumplimiento Alambre 0.062Document2 paginiCertificado de Cumplimiento Alambre 0.062gizaloÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- CZ120 (CW612N) : Technical DatasheetDocument1 paginăCZ120 (CW612N) : Technical DatasheetAmrut KanungoÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- General Information For Bicycle and Tricycle RepairDocument9 paginiGeneral Information For Bicycle and Tricycle RepairyuvarajchiÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- SAP EWM TrainingDocument10 paginiSAP EWM TrainingMindMajix TechnologiesÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Quality Walk Report FormatDocument14 paginiQuality Walk Report FormatAmar KolachinaÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Introduction To CIM & Manufacturing EnterpriseDocument53 paginiIntroduction To CIM & Manufacturing Enterprisesabtrex0% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- NTPC Quality InspectionDocument39 paginiNTPC Quality InspectionPower Power60% (5)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Pharma Chemical IrelandDocument33 paginiPharma Chemical IrelandlydiecoulÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Rmc3low Mold in GraphicsDocument6 paginiRmc3low Mold in GraphicsKyle PomaÎncă nu există evaluări

- Redbook Vol2part1Document194 paginiRedbook Vol2part1fiestosu_testosu0% (1)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Morris Medium Duty Cutting and Welding Outfit Model HCW-23P Instruction ManualsDocument18 paginiMorris Medium Duty Cutting and Welding Outfit Model HCW-23P Instruction ManualsTaj Deluria100% (1)

- Position Paper Outline SampleDocument3 paginiPosition Paper Outline SampleRenee Louise CoÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Cable Tray SystemsDocument45 paginiCable Tray SystemsAmin Hasan AminÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Job Order Costing Seatwork 3Document2 paginiJob Order Costing Seatwork 3Charie VelasquezÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Advanced Quality ManualDocument15 paginiAdvanced Quality ManualPhilip AnomnezeÎncă nu există evaluări

- Tube Rolling WorksheetDocument1 paginăTube Rolling Worksheetmicheld1964Încă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Job CostingDocument28 paginiJob CostingAbi BieÎncă nu există evaluări

- Stability Q ADocument16 paginiStability Q Amaneshdixit4312Încă nu există evaluări

- MPC BlockdiagramDocument15 paginiMPC BlockdiagramKalpesh BardeÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Operations Management MRPDocument32 paginiOperations Management MRPDeni KurniawanÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- 4.2-Certificados Ekc Agosto 2013 90 CilindrosDocument7 pagini4.2-Certificados Ekc Agosto 2013 90 CilindrosPercyAlexanderÎncă nu există evaluări

- Cost CurvesDocument40 paginiCost CurvesNRK Ravi Shankar CCBMDO - 16 BatchÎncă nu există evaluări

- Aprroved MPS EPDocument1 paginăAprroved MPS EPAlverastine AnÎncă nu există evaluări

- Storage Shelf Life of Paints 0Document1 paginăStorage Shelf Life of Paints 0Maung SleeperÎncă nu există evaluări

- Small Industries Service Institute: Details of Major Extension Services Provided in The Institute Are Given BelowDocument5 paginiSmall Industries Service Institute: Details of Major Extension Services Provided in The Institute Are Given BelowMểểŕá PáńćhálÎncă nu există evaluări

- UltraTech AFR Presentation PDFDocument11 paginiUltraTech AFR Presentation PDFAnonymous Cxriyx9HIXÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Research MethodologyDocument9 paginiResearch MethodologyYasHesh MorkhiaÎncă nu există evaluări

- Trends in Apparel Manufacturing TechnologyDocument8 paginiTrends in Apparel Manufacturing TechnologyAmit SinghÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)