S-ar putea să vă placă și

- Druthers Forming Answer KeyDocument3 paginiDruthers Forming Answer KeyDesventes AdrienÎncă nu există evaluări

- Jun18l1-S02pm QaDocument22 paginiJun18l1-S02pm QajuanÎncă nu există evaluări

- Wilkerson Company ABCDocument4 paginiWilkerson Company ABCrajyalakshmiÎncă nu există evaluări

- KKTiwari - 18214263 - Worldwide Paper Company-2016Document5 paginiKKTiwari - 18214263 - Worldwide Paper Company-2016KritikaPandeyÎncă nu există evaluări

- Mercury Athletic (Student Templates) FinalDocument6 paginiMercury Athletic (Student Templates) FinalGarland GayÎncă nu există evaluări

- NPV and IRR Calculations for Investment Projects AnalysisDocument8 paginiNPV and IRR Calculations for Investment Projects AnalysisCheytan Thakar100% (3)

- Lockheed Case SolutionDocument3 paginiLockheed Case SolutionKashish SrivastavaÎncă nu există evaluări

- Lockheed Tristar Case SolutionDocument3 paginiLockheed Tristar Case SolutionPrakash Nishtala100% (1)

- Case Study: "Green Zebra": NotesDocument1 paginăCase Study: "Green Zebra": NotesFlora PapastfÎncă nu există evaluări

- Case SolutionDocument7 paginiCase SolutionNeha SadhotraÎncă nu există evaluări

- Lockheed Tristar Case Similar SolutionDocument12 paginiLockheed Tristar Case Similar SolutionguruprasadkudvaÎncă nu există evaluări

- Case 5Document12 paginiCase 5JIAXUAN WANGÎncă nu există evaluări

- Case 1 SolDocument22 paginiCase 1 Solstig2lufetÎncă nu există evaluări

- Lockeed 5 StarDocument6 paginiLockeed 5 StarAjay SinghÎncă nu există evaluări

- Chapter 7 Student File After 1st ClassDocument10 paginiChapter 7 Student File After 1st Classasflkhaf2Încă nu există evaluări

- Valuing ProjectsDocument5 paginiValuing ProjectsAjay SinghÎncă nu există evaluări

- Lockheed Tristar Case Study 11020241041Document19 paginiLockheed Tristar Case Study 11020241041R Harika Reddy100% (7)

- Lockheed Tristar ProjectDocument1 paginăLockheed Tristar ProjectDurgaprasad VelamalaÎncă nu există evaluări

- Chapter 12: Corporate Valuation and Financial Planning: Page 1Document33 paginiChapter 12: Corporate Valuation and Financial Planning: Page 1nouraÎncă nu există evaluări

- Super ProjectDocument1 paginăSuper ProjectVaibhav SaithÎncă nu există evaluări

- Student SpreadsheetDocument14 paginiStudent SpreadsheetPriyanka Agarwal0% (1)

- Investment DetectiveDocument5 paginiInvestment DetectiveNadya Rizkita100% (1)

- Rougir Cosmetics International Did Not Have Internal Capacity To Meet DemandDocument3 paginiRougir Cosmetics International Did Not Have Internal Capacity To Meet DemandSameed Zaheer Khan100% (1)

- HPC Western India Refinery Project NPV AnalysisDocument1 paginăHPC Western India Refinery Project NPV AnalysisAmmrita SharmaÎncă nu există evaluări

- Excel Spreadsheet Sampa VideoDocument5 paginiExcel Spreadsheet Sampa VideoFaith AllenÎncă nu există evaluări

- Capital Rationing PDFDocument4 paginiCapital Rationing PDFSigei Leonard90% (10)

- Homework Assignment 1 KeyDocument6 paginiHomework Assignment 1 KeymetetezcanÎncă nu există evaluări

- Project Management Chapter 8 Investment Criteria Question AnswersDocument6 paginiProject Management Chapter 8 Investment Criteria Question AnswersAkm EngidaÎncă nu există evaluări

- Valuing Capital Investment Projects For PracticeDocument18 paginiValuing Capital Investment Projects For PracticeShivam Goyal100% (1)

- Assignment 2 Lockheed CaseDocument6 paginiAssignment 2 Lockheed CaseBob MarlowÎncă nu există evaluări

- Year 1979 1980 1981 1982 1983 1984 Period 0 1 2 3 4 5Document30 paginiYear 1979 1980 1981 1982 1983 1984 Period 0 1 2 3 4 5shardullavande33% (3)

- Beta Management QuestionsDocument1 paginăBeta Management QuestionsbjhhjÎncă nu există evaluări

- Asset Beta AnalysisDocument13 paginiAsset Beta AnalysisamuakaÎncă nu există evaluări

- Investment Analysis - Lockheed Tri-StarDocument2 paginiInvestment Analysis - Lockheed Tri-Staraclink88100% (1)

- Msdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleDocument24 paginiMsdi Alcala de Henares, Spain: Click To Edit Master Subtitle StyleShashank Shekhar100% (1)

- Lockheed Tri Star Capital Budgeting Case AnalysisDocument9 paginiLockheed Tri Star Capital Budgeting Case AnalysisMichael DevereauxÎncă nu există evaluări

- American Chemical CorporationDocument8 paginiAmerican Chemical CorporationAnastasiaÎncă nu există evaluări

- Worldwide Paper Company: Case Solution Company BackgroundDocument4 paginiWorldwide Paper Company: Case Solution Company BackgroundJauhari WicaksonoÎncă nu există evaluări

- Section E - Group 1 - RegionFly CaseDocument6 paginiSection E - Group 1 - RegionFly CaseAshish VijayaratnaÎncă nu există evaluări

- Sampa Video: Project ValuationDocument18 paginiSampa Video: Project Valuationkrissh_87Încă nu există evaluări

- Financial analysis of American Chemical Corporation plant acquisitionDocument9 paginiFinancial analysis of American Chemical Corporation plant acquisitionBenÎncă nu există evaluări

- Daud Engine Parts CompanyDocument3 paginiDaud Engine Parts CompanyJawadÎncă nu există evaluări

- Valuing Capital Investment ProjectsDocument13 paginiValuing Capital Investment ProjectsSiddhesh MahadikÎncă nu există evaluări

- Sampa VideoDocument18 paginiSampa Videomilan979Încă nu există evaluări

- 18-Conway IndustriesDocument5 pagini18-Conway IndustriesKiranJumanÎncă nu există evaluări

- Hitungan Kuis 6 Bethesda Mining CompanyDocument6 paginiHitungan Kuis 6 Bethesda Mining Companyrica100% (1)

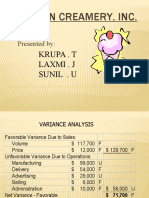

- Boston Creamery CaseDocument9 paginiBoston Creamery Caselion_heart3001100% (1)

- O.M Scott and Sons Case SummaryDocument2 paginiO.M Scott and Sons Case SummarySUSHMITA SHUBHAMÎncă nu există evaluări

- Nova Case Course HeroDocument10 paginiNova Case Course HerolibroaklatÎncă nu există evaluări

- Color ScopeDocument10 paginiColor Scopedharti_thakare100% (1)

- Satish M: Corporate Finance 2: MBA 2020-22Document49 paginiSatish M: Corporate Finance 2: MBA 2020-22Keerthi PaulÎncă nu există evaluări

- PIA Breakeven Analysis and Financial Performance ReportDocument3 paginiPIA Breakeven Analysis and Financial Performance ReportsaadsahilÎncă nu există evaluări

- Proforma Cash Flow Analysis and Recommendations for Chemalite IncDocument8 paginiProforma Cash Flow Analysis and Recommendations for Chemalite IncHàMềmÎncă nu există evaluări

- Sec-2 - Subgroup-9 (FM-Hola Kola)Document9 paginiSec-2 - Subgroup-9 (FM-Hola Kola)Ankit VisputeÎncă nu există evaluări

- Super ProjectDocument12 paginiSuper ProjectSrija LahiriÎncă nu există evaluări

- Sampa Video Inc.: Thousand of Dollars Exhibit 4Document2 paginiSampa Video Inc.: Thousand of Dollars Exhibit 4nimarÎncă nu există evaluări

- Final Ocean Carriers Case ReportDocument7 paginiFinal Ocean Carriers Case ReportStefanoAquilinoÎncă nu există evaluări

- Msdi - Alcala de Henares, SpainDocument4 paginiMsdi - Alcala de Henares, SpainDurgesh Nandini Mohanty100% (1)

- Tire City Case Study SolutionDocument2 paginiTire City Case Study SolutionPrathap Sankar0% (1)

- Investment Analysis and Lockheed Tri Star: V C KGDocument6 paginiInvestment Analysis and Lockheed Tri Star: V C KGKrishna Prasad NÎncă nu există evaluări

- Corporate Finance I: Home Assignment 2 Due by January 30Document2 paginiCorporate Finance I: Home Assignment 2 Due by January 30RahulÎncă nu există evaluări

- Session 4: Free Cash Flow and Net Present Value: N. K. Chidambaran Corporate FinanceDocument26 paginiSession 4: Free Cash Flow and Net Present Value: N. K. Chidambaran Corporate FinanceSaurabh GuptaÎncă nu există evaluări

- Tristar Case Sol.Document4 paginiTristar Case Sol.Niketa JaiswalÎncă nu există evaluări

- Theoretical and Conceptual Questions: (See Notes or Textbook)Document4 paginiTheoretical and Conceptual Questions: (See Notes or Textbook)raymondÎncă nu există evaluări

- Capital BudgetingDocument2 paginiCapital BudgetingZarmina ZaidÎncă nu există evaluări

- Tutorial 3 SheetDocument2 paginiTutorial 3 Sheetnourkhaled1218Încă nu există evaluări

- PS01 MainDocument12 paginiPS01 MainSumanth KolliÎncă nu există evaluări

- Global Market NutraceuticalsDocument50 paginiGlobal Market NutraceuticalsRahmi Jinan AuuriyahÎncă nu există evaluări

- How Long Does Stored Food LastDocument7 paginiHow Long Does Stored Food LastAjay SinghÎncă nu există evaluări

- Hb-Essentials For Kids and Teens-One-pagerDocument2 paginiHb-Essentials For Kids and Teens-One-pagerAjay SinghÎncă nu există evaluări

- Certificate For TeeDocument1 paginăCertificate For TeehitenbhardwajÎncă nu există evaluări

- Food Fortification Basic On PremixDocument36 paginiFood Fortification Basic On PremixAjay SinghÎncă nu există evaluări

- SWOT Analysis of PEPSICO IndiaDocument4 paginiSWOT Analysis of PEPSICO IndiaKartik KaushikÎncă nu există evaluări

- Think Without EggDocument28 paginiThink Without EggAjay Singh100% (1)

- Sensory Evaluation 1Document9 paginiSensory Evaluation 1Sachin TondarkarÎncă nu există evaluări

- Beverage Industry ProspectiveDocument4 paginiBeverage Industry ProspectiveAjay SinghÎncă nu există evaluări

- OTA Book 7 031013Document22 paginiOTA Book 7 031013Ajay SinghÎncă nu există evaluări

- Indian Snacks Industry OverviewDocument3 paginiIndian Snacks Industry OverviewNirav Parmar0% (1)

- Regional Manager Sales Marketing Bayer Mumbai JobDocument1 paginăRegional Manager Sales Marketing Bayer Mumbai JobAjay SinghÎncă nu există evaluări

- SWOT Analysis of PEPSICO IndiaDocument4 paginiSWOT Analysis of PEPSICO IndiaKartik KaushikÎncă nu există evaluări

- DMRC 123iit DelhiDocument7 paginiDMRC 123iit DelhiAjay SinghÎncă nu există evaluări

- Fast Moving Consumer GoodsDocument44 paginiFast Moving Consumer GoodsDeenDayal50% (4)

- Welcome To Paschimanchal Vidyut Vitran Nigam Ltd2Document1 paginăWelcome To Paschimanchal Vidyut Vitran Nigam Ltd2Ajay SinghÎncă nu există evaluări

- DMRC 123iit DelhiDocument7 paginiDMRC 123iit DelhiAjay SinghÎncă nu există evaluări

- Sanjeev LudhianaDocument1 paginăSanjeev LudhianaAjay SinghÎncă nu există evaluări

- RadicoDocument1 paginăRadicoAjay SinghÎncă nu există evaluări

- Can India Be The Food Basket For The OwrkdDocument16 paginiCan India Be The Food Basket For The OwrkdShailendra KumarÎncă nu există evaluări

- Decemeber 2020 Examinations: Suggested Answers ToDocument66 paginiDecemeber 2020 Examinations: Suggested Answers ToramanÎncă nu există evaluări

- Chapter 4 AnswersDocument9 paginiChapter 4 AnswersCDT MIKI EMERALD CUEVAÎncă nu există evaluări

- Leasing ProblemsDocument11 paginiLeasing ProblemsAbhishek AbhiÎncă nu există evaluări

- Project Management UnitDocument12 paginiProject Management UnitSyed JafferÎncă nu există evaluări

- Fiscal Year Is January-December. All Values USD Millions.: AssetsDocument29 paginiFiscal Year Is January-December. All Values USD Millions.: AssetsHubert Luis Madariaga ManyaÎncă nu există evaluări

- Capital Budgeting Analysis of Overseas SubsidiaryDocument12 paginiCapital Budgeting Analysis of Overseas SubsidiaryThao Bui ThiÎncă nu există evaluări

- Fmi S3Document9 paginiFmi S3Paras Mavani50% (2)

- Bs Revision GuideDocument64 paginiBs Revision GuideFegason Fegy100% (1)

- Chapter 18 - ShanaDocument8 paginiChapter 18 - ShanaHanz SadiaÎncă nu există evaluări

- Capital and Revenue ExpenditureDocument87 paginiCapital and Revenue ExpenditurefatynssvÎncă nu există evaluări

- Capital Budgeting InflationDocument11 paginiCapital Budgeting InflationMeghana ErapagaÎncă nu există evaluări

- Investment DecisionDocument26 paginiInvestment DecisionToyin Gabriel AyelemiÎncă nu există evaluări

- BAIT3153 Software Project Management Tutorial 1Document4 paginiBAIT3153 Software Project Management Tutorial 1WEI SHEUNG CHENÎncă nu există evaluări

- 11 12 NPV Ror PBP BCRDocument18 pagini11 12 NPV Ror PBP BCRizmehsjjjjÎncă nu există evaluări

- Majestic Gold NI 43-101 August 2013Document191 paginiMajestic Gold NI 43-101 August 2013MJSgetgoingÎncă nu există evaluări

- Capital Iq MaterialDocument38 paginiCapital Iq MaterialMadan MohanÎncă nu există evaluări

- ECBS Livestock Feed Feasibility Report for Anambra StateDocument70 paginiECBS Livestock Feed Feasibility Report for Anambra StateEmerging Capital Business SchoolÎncă nu există evaluări

- Assignment - Corporate FinanceDocument9 paginiAssignment - Corporate FinanceShivam GoelÎncă nu există evaluări

- 9 Capital Budgeting Class ProblemDocument8 pagini9 Capital Budgeting Class Problemowen.berthetÎncă nu există evaluări

- Risk and Managerial (Real) Options in Capital Budgeting Risk and Managerial (Real) Options in Capital BudgetingDocument44 paginiRisk and Managerial (Real) Options in Capital Budgeting Risk and Managerial (Real) Options in Capital Budgetingabdul salamÎncă nu există evaluări

- Homework 2 2018 Auditing 12522Document3 paginiHomework 2 2018 Auditing 12522Muhammad MudassarÎncă nu există evaluări

- FMG 22-IntroductionDocument22 paginiFMG 22-IntroductionPrateek GargÎncă nu există evaluări

- Performance Improvement in Hospitals and Health Systems Managing Analytics and Quality in Healthcare (2nd Edition), Cap 5Document32 paginiPerformance Improvement in Hospitals and Health Systems Managing Analytics and Quality in Healthcare (2nd Edition), Cap 5Daniela LópezÎncă nu există evaluări

- 2-4 2006 Dec ADocument13 pagini2-4 2006 Dec AAjay Takiar50% (2)