S-ar putea să vă placă și

- Terms and Conditions For Loyalty ProgramDocument2 paginiTerms and Conditions For Loyalty ProgramSportspower WarrnamboolÎncă nu există evaluări

- Porter's Five Forces: Understand competitive forces and stay ahead of the competitionDe la EverandPorter's Five Forces: Understand competitive forces and stay ahead of the competitionEvaluare: 4 din 5 stele4/5 (10)

- Startup India Seed Fund Scheme: Startup Sample Pitch DeckDocument13 paginiStartup India Seed Fund Scheme: Startup Sample Pitch DeckSimran KhuranaÎncă nu există evaluări

- Dynamics of Internal Environment in BusinessDocument23 paginiDynamics of Internal Environment in Businesslionviji50% (2)

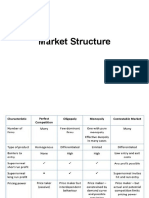

- Theory of Market: Perfect Competition: Nature and Relevance Monopoly and Monopolistic Competition OligopolyDocument18 paginiTheory of Market: Perfect Competition: Nature and Relevance Monopoly and Monopolistic Competition OligopolyDivyanshu BargaliÎncă nu există evaluări

- Solution Manualch13Document33 paginiSolution Manualch13StoneCold Alex Mochan80% (5)

- BIM Maturity MatrixDocument7 paginiBIM Maturity MatrixRicardo FreitasÎncă nu există evaluări

- Oligopoly:: Firm Industry Monopoly Monopolistic CompetitionDocument19 paginiOligopoly:: Firm Industry Monopoly Monopolistic CompetitionBernard Okpe100% (2)

- Monopolistic Competition - Written ReportDocument11 paginiMonopolistic Competition - Written ReportEd Leen Ü92% (12)

- Chap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsDocument48 paginiChap 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsjeankerlensÎncă nu există evaluări

- Effective Comunication SkillsDocument36 paginiEffective Comunication SkillsScarlet100% (5)

- niir-directory-database-india-professionals-architects-interior-decorators-building-contractors-property-dealers-real-estate-agents-brokers-developers-builders-delhi-amp-ncr-region-construction-materialsDocument11 pagininiir-directory-database-india-professionals-architects-interior-decorators-building-contractors-property-dealers-real-estate-agents-brokers-developers-builders-delhi-amp-ncr-region-construction-materialsDoctor SamÎncă nu există evaluări

- Consumer-Brand Relationships in Step-Down Line Extensions of Luxury and Designer BrandsDocument25 paginiConsumer-Brand Relationships in Step-Down Line Extensions of Luxury and Designer BrandsSohaib SangiÎncă nu există evaluări

- Cafe ProposalDocument14 paginiCafe ProposalSohaib SangiÎncă nu există evaluări

- Crafting Strategy - Summary'sDocument3 paginiCrafting Strategy - Summary'sShivam Kumar91% (11)

- A Market Structure Characterized by A Large Number of Small FirmsDocument9 paginiA Market Structure Characterized by A Large Number of Small FirmsSurya PanwarÎncă nu există evaluări

- Resume of Principles of Economics: Firms in Competitive Market (Chapter 14)Document4 paginiResume of Principles of Economics: Firms in Competitive Market (Chapter 14)Wanda AuliaÎncă nu există evaluări

- Monopolistic Competition, Oligopoly, and Pure MonopolyDocument5 paginiMonopolistic Competition, Oligopoly, and Pure MonopolyImran SiddÎncă nu există evaluări

- What Is Monopolistic CompetitionDocument9 paginiWhat Is Monopolistic CompetitionParag BorleÎncă nu există evaluări

- Group4 BSA 1A Monopolistic Competition Research ActivityDocument11 paginiGroup4 BSA 1A Monopolistic Competition Research ActivityRoisu De KuriÎncă nu există evaluări

- Types of Market Reviewer QuizDocument3 paginiTypes of Market Reviewer QuizJackie Lyn Bulatao Dela PasionÎncă nu există evaluări

- Monopolistic CompetitionDocument19 paginiMonopolistic Competitiondev.m.dodiyaÎncă nu există evaluări

- Chapter 9Document16 paginiChapter 9BenjaÎncă nu există evaluări

- Monopolies That Make Super Normal Profits Are Always Against Public Interest Because They Could Charge A Lower Price Than They DoDocument4 paginiMonopolies That Make Super Normal Profits Are Always Against Public Interest Because They Could Charge A Lower Price Than They DohotungsonÎncă nu există evaluări

- Micro 7 and 8Document36 paginiMicro 7 and 8amanuelÎncă nu există evaluări

- Monopolistic CompetitionDocument17 paginiMonopolistic CompetitionAlok ShuklaÎncă nu există evaluări

- 2010 Chpt11answersDocument6 pagini2010 Chpt11answersMyron JohnsonÎncă nu există evaluări

- Monopolistic CompetitionDocument15 paginiMonopolistic Competitionvivekmestri0% (1)

- Monopolistic CompetitionDocument5 paginiMonopolistic CompetitionSyed BabrakÎncă nu există evaluări

- ECON 2 Module CHAP 5 Market Structure and Imperfect CompetitionDocument15 paginiECON 2 Module CHAP 5 Market Structure and Imperfect CompetitionAngelica MayÎncă nu există evaluări

- Economics AssignmentDocument4 paginiEconomics AssignmentFarman RazaÎncă nu există evaluări

- Chapter 16 - MicroeconomicsDocument9 paginiChapter 16 - MicroeconomicsFidan MehdizadəÎncă nu există evaluări

- Monopolistic Competition and Oligopoly 1Document6 paginiMonopolistic Competition and Oligopoly 1Katrina LabisÎncă nu există evaluări

- Unit III Monopolistic CompitionDocument6 paginiUnit III Monopolistic CompitionPrashant ShahaneÎncă nu există evaluări

- Chapter 7 Market Structures Teacher NotesDocument10 paginiChapter 7 Market Structures Teacher Notesresendizalexander05Încă nu există evaluări

- EconomicsDocument2 paginiEconomicsIrish Mae T. EspallardoÎncă nu există evaluări

- Monopolistic CompetitionDocument10 paginiMonopolistic CompetitionDharmaj AnajwalaÎncă nu există evaluări

- Monopoly and Monopolist Competition: DefinitionDocument6 paginiMonopoly and Monopolist Competition: DefinitionLavanya KasettyÎncă nu există evaluări

- Unit 4 CC 4 PDFDocument49 paginiUnit 4 CC 4 PDFKamlesh AgrawalÎncă nu există evaluări

- Monopolistic Competition-1Document24 paginiMonopolistic Competition-1Rishbha patelÎncă nu există evaluări

- Presetation On Perfectly Competittive Market Vs Monopoly: Rafi Ahmed (11100100030)Document16 paginiPresetation On Perfectly Competittive Market Vs Monopoly: Rafi Ahmed (11100100030)Rafi AhmêdÎncă nu există evaluări

- What Government Policies Might Be Used To Counteract The Problems That Result From High Barriers To Entry?Document3 paginiWhat Government Policies Might Be Used To Counteract The Problems That Result From High Barriers To Entry?Trisha VelascoÎncă nu există evaluări

- Perfect Competition Describes Markets Such That No Participants Are Large Enough To HauctDocument17 paginiPerfect Competition Describes Markets Such That No Participants Are Large Enough To HauctRrisingg MishraaÎncă nu există evaluări

- Market StructureDocument3 paginiMarket StructureJoshua CaraldeÎncă nu există evaluări

- Monopolistic Competition: Registration For Wikiconference India 2011, Mumbai Is Now OpenDocument6 paginiMonopolistic Competition: Registration For Wikiconference India 2011, Mumbai Is Now Openakhilthambi123Încă nu există evaluări

- Project ReportDocument10 paginiProject ReportfarhanÎncă nu există evaluări

- Chapter Review 15Document4 paginiChapter Review 15Tória RajabecÎncă nu există evaluări

- Jawapan Saq 3 LatestDocument3 paginiJawapan Saq 3 LatestAre HidayuÎncă nu există evaluări

- Managerial EconDocument5 paginiManagerial EconJulienne CaitÎncă nu există evaluări

- Task Monopolistic CompetitionDocument2 paginiTask Monopolistic CompetitionmulianiÎncă nu există evaluări

- Monopolistic Comeptition: M. Shivarama Krishna 10HM28Document19 paginiMonopolistic Comeptition: M. Shivarama Krishna 10HM28Powli HarshavardhanÎncă nu există evaluări

- Monopolistic CompetitionDocument4 paginiMonopolistic CompetitionCookie LayugÎncă nu există evaluări

- Assignment - Market StructureDocument5 paginiAssignment - Market Structurerhizelle19Încă nu există evaluări

- 8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsDocument6 pagini8 - Managing in Competitive, Monopolistic, and Monopolistically Competitive MarketsMikkoÎncă nu există evaluări

- ECO 204 Final PaperDocument9 paginiECO 204 Final Paperfields169Încă nu există evaluări

- Economics Notes Nec CH - 5 StuDocument11 paginiEconomics Notes Nec CH - 5 StuBirendra ShresthaÎncă nu există evaluări

- Applied Ec 6Document9 paginiApplied Ec 6CallistaÎncă nu există evaluări

- Market Structure NotesDocument8 paginiMarket Structure NotesABDUL HADIÎncă nu există evaluări

- Economics AssignmentDocument21 paginiEconomics AssignmentMichael RopÎncă nu există evaluări

- Economics Chap 13 ReviewDocument5 paginiEconomics Chap 13 ReviewAnonymous EBW1hy64Q1Încă nu există evaluări

- Characteristics of OligopolyDocument3 paginiCharacteristics of OligopolyJulie ann YbanezÎncă nu există evaluări

- Competition, Profit and Other Objectives: What Does Normal Profit Mean?Document7 paginiCompetition, Profit and Other Objectives: What Does Normal Profit Mean?Ming Pong NgÎncă nu există evaluări

- Monopoly Equilibrium UploadedDocument10 paginiMonopoly Equilibrium Uploadedasal661Încă nu există evaluări

- Zishan Eco AssignmentDocument5 paginiZishan Eco AssignmentAnas AliÎncă nu există evaluări

- Practice Questions For Quiz 4 With SolutionsDocument6 paginiPractice Questions For Quiz 4 With SolutionsvdvdÎncă nu există evaluări

- Price and Output Under A Pure MonopolyDocument5 paginiPrice and Output Under A Pure MonopolysumayyabanuÎncă nu există evaluări

- Types of Market and Price DeterminationDocument4 paginiTypes of Market and Price DeterminationSaurabhÎncă nu există evaluări

- Market StructureDocument19 paginiMarket StructureSri HarshaÎncă nu există evaluări

- Perfect and Imperfect CompetitionDocument7 paginiPerfect and Imperfect CompetitionShirish GutheÎncă nu există evaluări

- AssignmentDocument3 paginiAssignmentSohaib SangiÎncă nu există evaluări

- Electronic CommerceDocument46 paginiElectronic CommerceSohaib SangiÎncă nu există evaluări

- TarmacDocument14 paginiTarmacSohaib SangiÎncă nu există evaluări

- Dr. Anjum PDFDocument31 paginiDr. Anjum PDFfaiqsattarÎncă nu există evaluări

- Corrugated PackagesDocument19 paginiCorrugated PackagesSohaib SangiÎncă nu există evaluări

- 7 Good Business Habits We Can Learn From Prophet MuhammadDocument3 pagini7 Good Business Habits We Can Learn From Prophet MuhammadSohaib SangiÎncă nu există evaluări

- EcommerceDocument3 paginiEcommerceSohaib SangiÎncă nu există evaluări

- Case Study CSM Entry Strategy of An Asian Car Manufacturer in The Swiss MarketDocument8 paginiCase Study CSM Entry Strategy of An Asian Car Manufacturer in The Swiss MarketMrs. Deepika JoshiÎncă nu există evaluări

- Children AdvertisingDocument23 paginiChildren AdvertisingSohaib SangiÎncă nu există evaluări

- Gourmet Foods FinalDocument86 paginiGourmet Foods FinalSohaib Sangi100% (1)

- Submitted To: Sir Nadir MagsiDocument52 paginiSubmitted To: Sir Nadir MagsiSohaib SangiÎncă nu există evaluări

- Pakistan Electronic Media Regulatory Authority ORDINANCE-2002Document32 paginiPakistan Electronic Media Regulatory Authority ORDINANCE-2002Sohaib SangiÎncă nu există evaluări

- News PaperDocument60 paginiNews PaperSohaib SangiÎncă nu există evaluări

- JFMM 08 2013 0096Document21 paginiJFMM 08 2013 0096Sohaib SangiÎncă nu există evaluări

- Hot Air Ballon. FinalDocument44 paginiHot Air Ballon. FinalSohaib SangiÎncă nu există evaluări

- Get FileDocument135 paginiGet FileSohaib SangiÎncă nu există evaluări

- Jrim 02 2014 0007Document24 paginiJrim 02 2014 0007Sohaib SangiÎncă nu există evaluări

- Final Criteria For Choosing Brand ElementsDocument99 paginiFinal Criteria For Choosing Brand ElementsSohaib Sangi100% (1)

- Jrim 02 2014 0007Document24 paginiJrim 02 2014 0007Sohaib SangiÎncă nu există evaluări

- Beef BookDocument49 paginiBeef Bookpynhun612Încă nu există evaluări

- Ejm 10 2012 0627Document22 paginiEjm 10 2012 0627Sohaib SangiÎncă nu există evaluări

- Ebr 11 2013 0132Document19 paginiEbr 11 2013 0132Sohaib SangiÎncă nu există evaluări

- Supplementary Services in Banking FirmsDocument39 paginiSupplementary Services in Banking FirmsSohaib Sangi0% (1)

- Ebr 11 2013 0132Document19 paginiEbr 11 2013 0132Sohaib SangiÎncă nu există evaluări

- Ejm 10 2012 0627Document22 paginiEjm 10 2012 0627Sohaib SangiÎncă nu există evaluări

- Apjml 10 2014 0148Document18 paginiApjml 10 2014 0148Sohaib SangiÎncă nu există evaluări

- Project ShaktiDocument48 paginiProject ShaktiSohaib SangiÎncă nu există evaluări

- Supply Chain Management - Applications and Simulations - M. Habib (Intech, 2011) WWDocument264 paginiSupply Chain Management - Applications and Simulations - M. Habib (Intech, 2011) WWEddie MylesÎncă nu există evaluări

- ResearchDocument22 paginiResearchAbegail BlancoÎncă nu există evaluări

- UC Course - Marketing Communication Strategy - Work1Document30 paginiUC Course - Marketing Communication Strategy - Work1ChefJumboTheSoundchefÎncă nu există evaluări

- P&G Group8 FinalDocument24 paginiP&G Group8 FinalFernando Williams100% (1)

- The Cultural Knowledge Perspective: Insights On Resource Creation For Marketing Theory, Practice, and EducationDocument13 paginiThe Cultural Knowledge Perspective: Insights On Resource Creation For Marketing Theory, Practice, and EducationEstudanteSaxÎncă nu există evaluări

- History: Nature Home (China) Co., LTDDocument3 paginiHistory: Nature Home (China) Co., LTDLeonel Chih-Shan MessiÎncă nu există evaluări

- Syl Ato Jan 15Document4 paginiSyl Ato Jan 15anilÎncă nu există evaluări

- Putanginang Thesis Nanaman!Document2 paginiPutanginang Thesis Nanaman!Iannie May ManlogonÎncă nu există evaluări

- RiriDocument89 paginiRiriCitraaÎncă nu există evaluări

- Sales Marketing Manager Building Materials in Albany NY Resume Christopher MicardiDocument3 paginiSales Marketing Manager Building Materials in Albany NY Resume Christopher MicardiChristopherMicardiÎncă nu există evaluări

- SHORT ANSWERS (8 Marks) What Is Price Discrimination? Explain The Basis of Price DiscriminationDocument36 paginiSHORT ANSWERS (8 Marks) What Is Price Discrimination? Explain The Basis of Price DiscriminationSathish KrishnaÎncă nu există evaluări

- Alice Hooper's TIE Case Study - CPP/Arcos/Alice/Leo BurnettDocument129 paginiAlice Hooper's TIE Case Study - CPP/Arcos/Alice/Leo BurnettThe International Exchange (aka TIE)Încă nu există evaluări

- Data HyundaiDocument16 paginiData Hyundaivishal kashyapÎncă nu există evaluări

- 1.budgeting QuestionDocument4 pagini1.budgeting QuestionPriyahemaniÎncă nu există evaluări

- MASTER Hyperion Performance Scorecard OverviewDocument36 paginiMASTER Hyperion Performance Scorecard OverviewmadangarliÎncă nu există evaluări

- 15 Strength 7 ElevenDocument3 pagini15 Strength 7 ElevenPavitra ThinakaranÎncă nu există evaluări

- mcd2050 WK 5 Quiz 2020 01Document3 paginimcd2050 WK 5 Quiz 2020 01Maureen EvangelineÎncă nu există evaluări

- 10key Decision AreasDocument18 pagini10key Decision AreasPham Gia Khiem (BTECHN)Încă nu există evaluări

- Managerial SkillsDocument136 paginiManagerial SkillsdiannevavenidoÎncă nu există evaluări

- Life Insurance Policy-A Case Study Project at Bajaj AllianzDocument35 paginiLife Insurance Policy-A Case Study Project at Bajaj AllianzrupalÎncă nu există evaluări

- Business Management Paper 1 Case Study HLSL PDFDocument4 paginiBusiness Management Paper 1 Case Study HLSL PDFAmerico Mallma SonccoÎncă nu există evaluări

- Journal Critique: A Literature Review of Corporate GovernanceDocument11 paginiJournal Critique: A Literature Review of Corporate GovernanceAudrey Kristina MaypaÎncă nu există evaluări

- CVP AnalysisDocument7 paginiCVP AnalysisKat Lontok0% (1)

- A Business Owner's Guide: Transform Your Business With SystemsDocument11 paginiA Business Owner's Guide: Transform Your Business With SystemsswapneelbawsayÎncă nu există evaluări