S-ar putea să vă placă și

- Financial analysis – Tesco Plc: Model Answer SeriesDe la EverandFinancial analysis – Tesco Plc: Model Answer SeriesÎncă nu există evaluări

- Series 1: 1. Profit Margin RatioDocument10 paginiSeries 1: 1. Profit Margin RatioPooja WadhwaniÎncă nu există evaluări

- Financial Ratio AnalysisDocument5 paginiFinancial Ratio AnalysisIrin HaÎncă nu există evaluări

- Alkyl Amines Chemicals LTD (Ratio)Document7 paginiAlkyl Amines Chemicals LTD (Ratio)Hardik BhanushaliÎncă nu există evaluări

- Exide Financial AnalysisDocument8 paginiExide Financial AnalysisM. Romaan QamarÎncă nu există evaluări

- Ratio Analysis 2Document15 paginiRatio Analysis 2Azmira RoslanÎncă nu există evaluări

- Financial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedDocument41 paginiFinancial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedGovindraj PrabhuÎncă nu există evaluări

- Analysis of Financial StatementsDocument54 paginiAnalysis of Financial StatementsBabasab Patil (Karrisatte)Încă nu există evaluări

- Bilgin Demir: Financial Statement & Security Analysis Case StudyDocument20 paginiBilgin Demir: Financial Statement & Security Analysis Case StudyadiscriÎncă nu există evaluări

- Assignment of Financial AccountingDocument15 paginiAssignment of Financial AccountingBhushan WadherÎncă nu există evaluări

- B&I DBBL PRSNDocument42 paginiB&I DBBL PRSNMahirÎncă nu există evaluări

- Strategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Document40 paginiStrategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Rupesh KadamÎncă nu există evaluări

- Accnts Projest - BajajDocument24 paginiAccnts Projest - BajajAprajita SaxenaÎncă nu există evaluări

- Searle Company Ratio Analysis 2010 2011 2012Document63 paginiSearle Company Ratio Analysis 2010 2011 2012Kaleb VargasÎncă nu există evaluări

- Assignment Next PLCDocument16 paginiAssignment Next PLCJames Jane50% (2)

- Corp Fin AssignDocument9 paginiCorp Fin AssignTwafik MoÎncă nu există evaluări

- AXIS Bank AnalysisDocument44 paginiAXIS Bank AnalysisArup SarkarÎncă nu există evaluări

- Profitability AnalysisDocument9 paginiProfitability AnalysisAnkit TyagiÎncă nu există evaluări

- Reasons For Collapse of BanksDocument25 paginiReasons For Collapse of BanksMichael VuhaÎncă nu există evaluări

- Amui Ind. Pvt. LTDDocument29 paginiAmui Ind. Pvt. LTDArpit McWanÎncă nu există evaluări

- Financial Analysis P&GDocument10 paginiFinancial Analysis P&Gsayko88Încă nu există evaluări

- Financial Statement Analysis - Pantaloon Retail IndiaDocument7 paginiFinancial Statement Analysis - Pantaloon Retail IndiaSupriyaThengdiÎncă nu există evaluări

- Financial Analysis of GSK Consumer HealthcareDocument36 paginiFinancial Analysis of GSK Consumer Healthcareadnan424100% (1)

- Ratio Analysis ITCDocument15 paginiRatio Analysis ITCVivek MaheshwaryÎncă nu există evaluări

- Final Report On Attock - IbfDocument25 paginiFinal Report On Attock - IbfSanam Aamir0% (1)

- Financial Management AssignmentDocument16 paginiFinancial Management AssignmentNishant goyalÎncă nu există evaluări

- Case 3: BNL StoresDocument16 paginiCase 3: BNL StoresAMBWANI NAREN MAHESHÎncă nu există evaluări

- Financial Management and Control - AssignmentDocument7 paginiFinancial Management and Control - AssignmentSabahat BashirÎncă nu există evaluări

- Anamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaDocument24 paginiAnamika Chakrabarty Anika Thakur Avpsa Dash Babli Kumari Gala MonikaAnamika ChakrabartyÎncă nu există evaluări

- Financial Ratio AnalysisDocument26 paginiFinancial Ratio AnalysisMujtaba HassanÎncă nu există evaluări

- Project Report FAM HULDocument16 paginiProject Report FAM HULSagar PanchalÎncă nu există evaluări

- Ratio AnalysisDocument13 paginiRatio AnalysisBharatsinh SarvaiyaÎncă nu există evaluări

- Financial AnalysisDocument14 paginiFinancial Analysisnikita kothari18Încă nu există evaluări

- Corporation: Group 3 Austria, Caren Caday, Shayne Marion de Guzman, Vanessa Padilla, Angela Valencia, Ma. RowenaDocument30 paginiCorporation: Group 3 Austria, Caren Caday, Shayne Marion de Guzman, Vanessa Padilla, Angela Valencia, Ma. RowenaMk EdsÎncă nu există evaluări

- Financial Analysis VIP IndustriesDocument5 paginiFinancial Analysis VIP IndustriesAvinash KatochÎncă nu există evaluări

- Overview of The Investing ActivitiesDocument9 paginiOverview of The Investing ActivitiesTiyani RodrigoÎncă nu există evaluări

- Inventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andDocument23 paginiInventory Turn Over Ratio Inventory Turnover Is A Showing How Many Times A Company's Inventory Is Sold andrajendranSelviÎncă nu există evaluări

- Financial Analysis of Askari Bank 2012Document28 paginiFinancial Analysis of Askari Bank 2012usmanrehmat100% (1)

- Current Ratio (Attock) Quick Ratio: Liquidity RatiosDocument10 paginiCurrent Ratio (Attock) Quick Ratio: Liquidity RatiosAli AmarÎncă nu există evaluări

- GIT - Principles of Managerial Finance (13th Edition) - Cap.3 (Pág.85-90)Document8 paginiGIT - Principles of Managerial Finance (13th Edition) - Cap.3 (Pág.85-90)katebariÎncă nu există evaluări

- Ratio Analysis of Renata Limited PPPDocument32 paginiRatio Analysis of Renata Limited PPPmdnabab0% (1)

- Ratio AnaalysisDocument10 paginiRatio AnaalysisMark K. EapenÎncă nu există evaluări

- Apollo Tyres Final)Document65 paginiApollo Tyres Final)Mitisha GaurÎncă nu există evaluări

- Ratio Analysis of ITCDocument22 paginiRatio Analysis of ITCDheeraj Girase100% (1)

- Fin103 LT1 2004-BMHDocument5 paginiFin103 LT1 2004-BMHJARED DARREN ONGÎncă nu există evaluări

- Mitchell's Ratio AnalysisDocument3 paginiMitchell's Ratio Analysismadnansajid8765Încă nu există evaluări

- Article 2 Roe Breakd Dec 12 5pDocument5 paginiArticle 2 Roe Breakd Dec 12 5pRicardo Jáquez CortésÎncă nu există evaluări

- Analysis of RatiosDocument4 paginiAnalysis of RatiosYbrantSachinÎncă nu există evaluări

- Tan - Final ExamDocument15 paginiTan - Final ExamKent Braña Tan100% (1)

- ProjectDocument34 paginiProjectAkhil NairÎncă nu există evaluări

- Mba8101: Financial and Managerial Accounting Financial Statement Analysis BY Name: Reg No.: JULY 2014Document9 paginiMba8101: Financial and Managerial Accounting Financial Statement Analysis BY Name: Reg No.: JULY 2014Sammy Datastat GathuruÎncă nu există evaluări

- Solution To Case 22: EVA - Does It Really Work?Document5 paginiSolution To Case 22: EVA - Does It Really Work?Ra MinÎncă nu există evaluări

- 6.3.1 EditedDocument47 pagini6.3.1 EditedPia Angela ElemosÎncă nu există evaluări

- A Grade SampleDocument25 paginiA Grade SampleTharindu PereraÎncă nu există evaluări

- Credit Evaluation ProcessDocument73 paginiCredit Evaluation ProcessNeeRaz Kunwar100% (2)

- High Performance Tire Case Study Report 1 (Group 7)Document24 paginiHigh Performance Tire Case Study Report 1 (Group 7)AZLINDA MOHD NADZRIÎncă nu există evaluări

- Financial Analysis of Tesco PLCDocument7 paginiFinancial Analysis of Tesco PLCSyed Toseef Ali100% (1)

- Final Review Session SPR12RปDocument10 paginiFinal Review Session SPR12RปFight FionaÎncă nu există evaluări

- Dmp3e Ch05 Solutions 02.28.10 FinalDocument37 paginiDmp3e Ch05 Solutions 02.28.10 Finalmichaelkwok1Încă nu există evaluări

- Corporate Finance:: School of Economics and ManagementDocument13 paginiCorporate Finance:: School of Economics and ManagementNgouem LudovicÎncă nu există evaluări

- KYC Version 3Document2 paginiKYC Version 3chanderp_15Încă nu există evaluări

- Madras High Court: M.Baskar Vs The Sub Registrar On 10 December, 2014Document12 paginiMadras High Court: M.Baskar Vs The Sub Registrar On 10 December, 2014Yugendra Babu K100% (1)

- Preetham Kaur VsDocument2 paginiPreetham Kaur VsYugendra Babu KÎncă nu există evaluări

- KYC Version 3Document2 paginiKYC Version 3chanderp_15Încă nu există evaluări

- From M. Subba RajuDocument1 paginăFrom M. Subba RajuYugendra Babu KÎncă nu există evaluări

- 10022016fin MS18Document8 pagini10022016fin MS18Yugendra Babu KÎncă nu există evaluări

- Andhra Pradesh State Level Police Recruitment Board: User GuideDocument10 paginiAndhra Pradesh State Level Police Recruitment Board: User GuideMK YÎncă nu există evaluări

- Nijo Project WorkDocument65 paginiNijo Project WorkJosh NirmalÎncă nu există evaluări

- TVP 456 ReportsDocument10 paginiTVP 456 ReportsYugendra Babu KÎncă nu există evaluări

- Working Capital Synopsis NewDocument4 paginiWorking Capital Synopsis NewYugendra Babu KÎncă nu există evaluări

- J CJ Notified 13012016 RCDocument1 paginăJ CJ Notified 13012016 RCYugendra Babu KÎncă nu există evaluări

- 31122015fin MS189Document2 pagini31122015fin MS189Yugendra Babu KÎncă nu există evaluări

- 11022016fin MS19Document19 pagini11022016fin MS19Yugendra Babu KÎncă nu există evaluări

- Heritage InventoryDocument83 paginiHeritage InventoryYugendra Babu KÎncă nu există evaluări

- 2013fin ms331Document5 pagini2013fin ms331api-218060126Încă nu există evaluări

- Environmental Pollution: Module - 4Document21 paginiEnvironmental Pollution: Module - 4sauravds7Încă nu există evaluări

- Manual Option FormDocument2 paginiManual Option Formsri kalyanÎncă nu există evaluări

- Plagarism Report For Journal 1Document6 paginiPlagarism Report For Journal 1Yugendra Babu KÎncă nu există evaluări

- The Importance of Communication: What Exactly Is Communication?Document5 paginiThe Importance of Communication: What Exactly Is Communication?Pramathesh NandanÎncă nu există evaluări

- Curriculum Vitae: A.SudheerDocument2 paginiCurriculum Vitae: A.SudheerYugendra Babu KÎncă nu există evaluări

- Applying For The Location / AreaDocument1 paginăApplying For The Location / AreaYugendra Babu KÎncă nu există evaluări

- Pulicherla 456reportsDocument10 paginiPulicherla 456reportsYugendra Babu KÎncă nu există evaluări

- Election Bills1Document1 paginăElection Bills1Yugendra Babu KÎncă nu există evaluări

- Option FormDocument2 paginiOption FormYugendra Babu KÎncă nu există evaluări

- A Study On Performance Appraisal in Nutrine Confectionery Company Pvt. LTD., at ChittoorDocument3 paginiA Study On Performance Appraisal in Nutrine Confectionery Company Pvt. LTD., at ChittoorYugendra Babu K100% (1)

- Electronic Ticket Record: Passenger Name(s)Document1 paginăElectronic Ticket Record: Passenger Name(s)Yugendra Babu KÎncă nu există evaluări

- Synopsis OldDocument44 paginiSynopsis OldYugendra Babu KÎncă nu există evaluări

- To Whome So Ever Itmay Concern: Ref No - HR/SMPPL/10348Document1 paginăTo Whome So Ever Itmay Concern: Ref No - HR/SMPPL/10348Yugendra Babu KÎncă nu există evaluări

- Future Trends in Advertising: E. Usha 134M1E00C6 Dept. of MBADocument18 paginiFuture Trends in Advertising: E. Usha 134M1E00C6 Dept. of MBAYugendra Babu KÎncă nu există evaluări

- Quantitative Techniques PDFDocument36 paginiQuantitative Techniques PDFGitsirasÎncă nu există evaluări

- Setting Value, Not Price - McKinsey & CompanyDocument15 paginiSetting Value, Not Price - McKinsey & Companya_sahaiÎncă nu există evaluări

- CmiDocument10 paginiCmiSanket GhelaniÎncă nu există evaluări

- Business Models Summary XINE249Document9 paginiBusiness Models Summary XINE249Antonio Prudencio Mori100% (1)

- Why Do Banks Disappear?: A History of Bank Failures and Acquisitions in Trinidad, 1836-1992Document26 paginiWhy Do Banks Disappear?: A History of Bank Failures and Acquisitions in Trinidad, 1836-1992Sauvik ChakrabortyÎncă nu există evaluări

- Marketing Strategy and Plan For New Product LaunchesDocument15 paginiMarketing Strategy and Plan For New Product LaunchesachwalotienoÎncă nu există evaluări

- My Project PollmansDocument16 paginiMy Project PollmansGilbertoumaÎncă nu există evaluări

- IAS 41 Application of Fair Value MeasurementDocument22 paginiIAS 41 Application of Fair Value MeasurementgigitoÎncă nu există evaluări

- Taxation - Paper T5Document20 paginiTaxation - Paper T5Kabutu ChuungaÎncă nu există evaluări

- Chapter 8Document11 paginiChapter 8Kalyani GogoiÎncă nu există evaluări

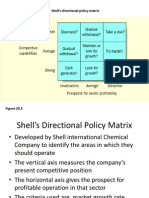

- Shell MatrixDocument10 paginiShell Matrixleloup84Încă nu există evaluări

- Max, M. (2004) ABC Trends in The Banking Sector - A Practitioner's Perspective'Document17 paginiMax, M. (2004) ABC Trends in The Banking Sector - A Practitioner's Perspective'Anonymous WFjMFHQÎncă nu există evaluări

- 411 Product Management-1Document110 pagini411 Product Management-1Awadhesh YadavÎncă nu există evaluări

- Launch of Juice ProductDocument16 paginiLaunch of Juice ProductMr. Unknown50% (2)

- Meaning and Definitions of Management AccountingDocument2 paginiMeaning and Definitions of Management AccountingHafizullah AnsariÎncă nu există evaluări

- Financial Management DBA1654Document130 paginiFinancial Management DBA1654Anbuoli ParthasarathyÎncă nu există evaluări

- Chapter 11 - Sheep and Goat Economics of Production and MarkeDocument28 paginiChapter 11 - Sheep and Goat Economics of Production and MarkegavinilaaÎncă nu există evaluări

- Wonderful Malaysia Berhad - Illustrative Financial Statements 2014Document243 paginiWonderful Malaysia Berhad - Illustrative Financial Statements 2014Selva Bavani SelwaduraiÎncă nu există evaluări

- BPMN6053 Management Information System: Individual Assignment Topic 1Document6 paginiBPMN6053 Management Information System: Individual Assignment Topic 1salman ahmadÎncă nu există evaluări

- Research Paper - EVA Indian Banking SectorDocument14 paginiResearch Paper - EVA Indian Banking SectorAnonymous rkZNo8Încă nu există evaluări

- Audit of Marketing FunctionDocument27 paginiAudit of Marketing FunctionElizabeth Patton67% (3)

- Sales Manager in Minneapolis ST Paul MN Resume Stacey BuzayDocument2 paginiSales Manager in Minneapolis ST Paul MN Resume Stacey BuzayStaceyBuzayÎncă nu există evaluări

- F7 June 2013 BPP Answers - LowresDocument16 paginiF7 June 2013 BPP Answers - Lowreskumassa kenya100% (1)

- Intimation Regarding Investors Meetings of The Company and Submission of Presentation To Be Made To The Investors (Company Update)Document37 paginiIntimation Regarding Investors Meetings of The Company and Submission of Presentation To Be Made To The Investors (Company Update)Shyam SunderÎncă nu există evaluări

- ROI For Cybersecurity ApproachesDocument17 paginiROI For Cybersecurity ApproachesArturo SeijasÎncă nu există evaluări

- Questions PPR 1Document2 paginiQuestions PPR 1kiss_naaÎncă nu există evaluări

- Fraud Risk Assement For B BankDocument66 paginiFraud Risk Assement For B BankdbedadaÎncă nu există evaluări

- Impact of Leverage Ratio On ProfitabilityDocument9 paginiImpact of Leverage Ratio On ProfitabilitySaadia SaeedÎncă nu există evaluări

- Working Capital ManagementDocument41 paginiWorking Capital ManagementHari Kishan Lal100% (1)

- International Marketing Business Plan: Coconut Husk TilesDocument24 paginiInternational Marketing Business Plan: Coconut Husk TilesBea MendozaÎncă nu există evaluări

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDe la Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNEvaluare: 4.5 din 5 stele4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDe la EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisEvaluare: 5 din 5 stele5/5 (6)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialEvaluare: 4.5 din 5 stele4.5/5 (32)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthDe la EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthEvaluare: 4 din 5 stele4/5 (20)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDe la EverandReady, Set, Growth hack:: A beginners guide to growth hacking successEvaluare: 4.5 din 5 stele4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistDe la EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistEvaluare: 4.5 din 5 stele4.5/5 (73)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDe la EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursEvaluare: 4.5 din 5 stele4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDe la EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingEvaluare: 4.5 din 5 stele4.5/5 (17)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 3.5 din 5 stele3.5/5 (8)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsDe la EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsEvaluare: 5 din 5 stele5/5 (1)

- Venture Deals: Be Smarter Than Your Lawyer and Venture CapitalistDe la EverandVenture Deals: Be Smarter Than Your Lawyer and Venture CapitalistEvaluare: 4 din 5 stele4/5 (32)

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- Mind over Money: The Psychology of Money and How to Use It BetterDe la EverandMind over Money: The Psychology of Money and How to Use It BetterEvaluare: 4 din 5 stele4/5 (24)

- Joy of Agility: How to Solve Problems and Succeed SoonerDe la EverandJoy of Agility: How to Solve Problems and Succeed SoonerEvaluare: 4 din 5 stele4/5 (1)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetDe la EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetEvaluare: 5 din 5 stele5/5 (2)

- Creating Shareholder Value: A Guide For Managers And InvestorsDe la EverandCreating Shareholder Value: A Guide For Managers And InvestorsEvaluare: 4.5 din 5 stele4.5/5 (8)

- How to Measure Anything: Finding the Value of Intangibles in BusinessDe la EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessEvaluare: 3.5 din 5 stele3.5/5 (4)

- Value: The Four Cornerstones of Corporate FinanceDe la EverandValue: The Four Cornerstones of Corporate FinanceEvaluare: 4.5 din 5 stele4.5/5 (18)