S-ar putea să vă placă și

- DoE Lesson Plan 11 Interest The Cost of Borrowing MoneyDocument20 paginiDoE Lesson Plan 11 Interest The Cost of Borrowing MoneyHoney Grace BicarÎncă nu există evaluări

- Learning Journal Unit 6 - Basic AccountingDocument6 paginiLearning Journal Unit 6 - Basic AccountingSindisiwe DlaminiÎncă nu există evaluări

- Finance - Self Study Guide For Staff of Micro Finance InstitutionsDocument9 paginiFinance - Self Study Guide For Staff of Micro Finance InstitutionsmhussainÎncă nu există evaluări

- Closed-End Credit Principal Nominal Annual Percentage Rate Periodic RateDocument4 paginiClosed-End Credit Principal Nominal Annual Percentage Rate Periodic RateSK Sabbir AhmedÎncă nu există evaluări

- Closed-End Credit Principal Nominal Annual Percentage Rate Periodic RateDocument4 paginiClosed-End Credit Principal Nominal Annual Percentage Rate Periodic RateSK Sabbir AhmedÎncă nu există evaluări

- Updated Loan Repayment Methods DocumentDocument4 paginiUpdated Loan Repayment Methods DocumentAnggi Gayatri SetiawanÎncă nu există evaluări

- BMT6127 Financial Planning and Wealth Management: Digital Assignment 01Document5 paginiBMT6127 Financial Planning and Wealth Management: Digital Assignment 01Prithivi RajÎncă nu există evaluări

- Define and Explain Thoroughly What Is CREDITDocument4 paginiDefine and Explain Thoroughly What Is CREDITAngelika SinguranÎncă nu există evaluări

- Unit 3 - 1 The Three C's of Credit: Nine Different Credit CardsDocument8 paginiUnit 3 - 1 The Three C's of Credit: Nine Different Credit CardsSSAÎncă nu există evaluări

- C1 D1 Doc Tech 2Document4 paginiC1 D1 Doc Tech 2Suman TiwariÎncă nu există evaluări

- CLD TUTORIAL 4 - SolutionDocument6 paginiCLD TUTORIAL 4 - SolutionCrystalin LukmanÎncă nu există evaluări

- 4-CONSUMER CREDIT (PART 2) (Choosing A Source of Credit, The Cost of Credit Alternatives)Document19 pagini4-CONSUMER CREDIT (PART 2) (Choosing A Source of Credit, The Cost of Credit Alternatives)Nur DinieÎncă nu există evaluări

- Personal Finance 1st Edition Walker Solutions Manual 1Document24 paginiPersonal Finance 1st Edition Walker Solutions Manual 1kurt100% (44)

- How Much Will A Two-Week, $250 Pay-Day Loan Cost?: Payday Loan-Single PaymentDocument2 paginiHow Much Will A Two-Week, $250 Pay-Day Loan Cost?: Payday Loan-Single PaymentbootybethathangÎncă nu există evaluări

- Business and Personal Finance Unit 2 Chapter 6 2007 Glencoe500Document81 paginiBusiness and Personal Finance Unit 2 Chapter 6 2007 Glencoe500Avi ThakurÎncă nu există evaluări

- Credit Report and Score BenefitsDocument3 paginiCredit Report and Score BenefitsChelsea CalabazaÎncă nu există evaluări

- Calabaza Chelsea Assignment#6Document3 paginiCalabaza Chelsea Assignment#6Chelsea CalabazaÎncă nu există evaluări

- Chapter 6 Review QuestionsDocument3 paginiChapter 6 Review Questionsapi-242667057100% (1)

- FIN 438 - Chapter 15 QuestionsDocument6 paginiFIN 438 - Chapter 15 QuestionsTrần Dương Mai PhươngÎncă nu există evaluări

- Types of LoansDocument9 paginiTypes of LoansSanjay VaruteÎncă nu există evaluări

- SAS #3-FIN012.docxDocument7 paginiSAS #3-FIN012.docxconandetic123Încă nu există evaluări

- Guide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1De la EverandGuide to Modern Personal Finance: For Students and Young Adults: Guide to Modern Personal Finance, #1Încă nu există evaluări

- Credit and CollectionDocument17 paginiCredit and CollectionDia Cessianne VillarolaÎncă nu există evaluări

- 1Document4 pagini1Rohan ShresthaÎncă nu există evaluări

- Consumer CreditDocument41 paginiConsumer CreditRup HunkÎncă nu există evaluări

- CHAPTER 13 Debt Management in Retirement Planning PDFDocument35 paginiCHAPTER 13 Debt Management in Retirement Planning PDFMaisarah YaziddÎncă nu există evaluări

- General Mathematics LAS Q2 WK 6Document18 paginiGeneral Mathematics LAS Q2 WK 6Prince Joshua SumagitÎncă nu există evaluări

- An Introduction To Credit CardDocument58 paginiAn Introduction To Credit CardAsefÎncă nu există evaluări

- Example Amortization ScheduleDocument3 paginiExample Amortization SchedulePankil R ShahÎncă nu există evaluări

- Chapter 7. Consumer CreditDocument27 paginiChapter 7. Consumer CreditshitalÎncă nu există evaluări

- UntitledDocument24 paginiUntitledEric JohnsonÎncă nu există evaluări

- C1T4 - Intro To Credit Cards Part 2 PDFDocument10 paginiC1T4 - Intro To Credit Cards Part 2 PDFTanmoy IimcÎncă nu există evaluări

- Banking and Finance: Biyani's Think TankDocument23 paginiBanking and Finance: Biyani's Think TankonlyvictoryÎncă nu există evaluări

- Loan AmortizationDocument14 paginiLoan AmortizationPoorvajaÎncă nu există evaluări

- Examen Parcial de InglesDocument18 paginiExamen Parcial de InglesIshaid Raul Reymundo AmesÎncă nu există evaluări

- Unit 4 Credit - For WEBSITEDocument46 paginiUnit 4 Credit - For WEBSITEASHISH KUMARÎncă nu există evaluări

- Microsoft Word - Week 6 Bonds Version - 1 Solution 9th 04 2019Document6 paginiMicrosoft Word - Week 6 Bonds Version - 1 Solution 9th 04 2019Mark LiÎncă nu există evaluări

- Personal Finance Canadian 3rd Edition Madura Solutions Manual 1Document36 paginiPersonal Finance Canadian 3rd Edition Madura Solutions Manual 1karenhalesondbatxme100% (26)

- Working Capital Management (GROUP 5)Document33 paginiWorking Capital Management (GROUP 5)Cyrylle AngelesÎncă nu există evaluări

- Mba Fa Iv Sem 403 Credit PolicyDocument9 paginiMba Fa Iv Sem 403 Credit Policyprachi bhattÎncă nu există evaluări

- J B Gupta Classes: General TopicsDocument29 paginiJ B Gupta Classes: General TopicsceojiÎncă nu există evaluări

- FinmanDocument3 paginiFinmanKaren LaccayÎncă nu există evaluări

- Module 7 8 Managing Your CreditDocument5 paginiModule 7 8 Managing Your CreditDonna Mae FernandezÎncă nu există evaluări

- Business Finance 5Document10 paginiBusiness Finance 5JizleÎncă nu există evaluări

- How to Manage Credit WiselyDocument36 paginiHow to Manage Credit WiselyAmara MaduagwuÎncă nu există evaluări

- Personal Finacial Literacy NotesDocument64 paginiPersonal Finacial Literacy Notesmpontier123100% (1)

- AdvancesprocessmDocument98 paginiAdvancesprocessmAmol DahiphaleÎncă nu există evaluări

- Notes in Fi3Document5 paginiNotes in Fi3Gray JavierÎncă nu există evaluări

- What is a Current Account Savings Account (CASADocument18 paginiWhat is a Current Account Savings Account (CASAKritika T100% (1)

- APTA - Endorsed Consolidation Loan ProgramDocument28 paginiAPTA - Endorsed Consolidation Loan Programaeman26Încă nu există evaluări

- 4 Lect. Time Value of Money - 2Document19 pagini4 Lect. Time Value of Money - 2Muhammad Hammad RajputÎncă nu există evaluări

- Module 1 3 Notes PayableDocument8 paginiModule 1 3 Notes PayableFujoshi BeeÎncă nu există evaluări

- 4 PDFDocument7 pagini4 PDFblitzkrigÎncă nu există evaluări

- Lovely Professional University - Docx MY ASIGNMENTDocument10 paginiLovely Professional University - Docx MY ASIGNMENTBali's Aabhi XBÎncă nu există evaluări

- TYPES OF CREDIT Week13Document61 paginiTYPES OF CREDIT Week13Richard Santiago JimenezÎncă nu există evaluări

- Current Liabilities Management: Prepared by Keldon BauerDocument35 paginiCurrent Liabilities Management: Prepared by Keldon BauerMónica GarzaÎncă nu există evaluări

- Credit CardDocument5 paginiCredit CardRitesh TolaniÎncă nu există evaluări

- From Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsDe la EverandFrom Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsÎncă nu există evaluări

- Understanding Credit Cards and Using Them WiselyDocument8 paginiUnderstanding Credit Cards and Using Them Wiselyasmat ullah khanÎncă nu există evaluări

- Integrated Business (Econ) 1516Document8 paginiIntegrated Business (Econ) 1516Victor NgÎncă nu există evaluări

- Book 3 Chapter 6 Answers EngDocument5 paginiBook 3 Chapter 6 Answers EngVictor NgÎncă nu există evaluări

- Book 3 Chapter 5 Answers EngDocument7 paginiBook 3 Chapter 5 Answers EngVictor NgÎncă nu există evaluări

- CA TM Chapter 22 EngDocument15 paginiCA TM Chapter 22 EngVictor NgÎncă nu există evaluări

- Marketing Chapter 8 3 RevisedDocument18 paginiMarketing Chapter 8 3 RevisedVictor NgÎncă nu există evaluări

- Book 3 Chapter 3 Answers EngDocument6 paginiBook 3 Chapter 3 Answers EngVictor NgÎncă nu există evaluări

- Book 3 Chapter 2 Answers EngDocument7 paginiBook 3 Chapter 2 Answers EngVictor NgÎncă nu există evaluări

- CA TM Chapter 23 EngDocument16 paginiCA TM Chapter 23 EngVictor NgÎncă nu există evaluări

- Book 3 Chapter 1 Answers EngDocument11 paginiBook 3 Chapter 1 Answers EngVictor NgÎncă nu există evaluări

- Longman F24 (Key)Document10 paginiLongman F24 (Key)Thomas Kong Ying LiÎncă nu există evaluări

- Longman F20 (Key)Document9 paginiLongman F20 (Key)Yan Pak KiuÎncă nu există evaluări

- Longman F21 (Key)Document18 paginiLongman F21 (Key)Yan Pak KiuÎncă nu există evaluări

- Marketing Chapter 1 3 RevisedDocument16 paginiMarketing Chapter 1 3 RevisedVictor NgÎncă nu există evaluări

- Marketing Chapter 5 3 RevisedDocument21 paginiMarketing Chapter 5 3 RevisedVictor NgÎncă nu există evaluări

- Marketing Chapter 7 3 RevisedDocument16 paginiMarketing Chapter 7 3 RevisedVictor NgÎncă nu există evaluări

- Sample BookletDocument28 paginiSample BookletVictor NgÎncă nu există evaluări

- Marketing Chapter 6 3 RevisedDocument13 paginiMarketing Chapter 6 3 RevisedVictor NgÎncă nu există evaluări

- Marketing Chapter 4 3 RevisedDocument19 paginiMarketing Chapter 4 3 RevisedVictor NgÎncă nu există evaluări

- HR Chapter 2 2 Eng Finalised0831Document16 paginiHR Chapter 2 2 Eng Finalised0831Victor NgÎncă nu există evaluări

- Marketing Chapter 2 3 RevisedDocument19 paginiMarketing Chapter 2 3 RevisedVictor NgÎncă nu există evaluări

- HR Chapter 6 2 Eng Finalised0903Document18 paginiHR Chapter 6 2 Eng Finalised0903Victor NgÎncă nu există evaluări

- Marketing Chapter 3 3 RevisedDocument15 paginiMarketing Chapter 3 3 RevisedVictor NgÎncă nu există evaluări

- HR Chapter 5 2 Eng Finalised0902Document19 paginiHR Chapter 5 2 Eng Finalised0902Victor NgÎncă nu există evaluări

- HR Chapter 1 2 Eng Finalised 0901Document22 paginiHR Chapter 1 2 Eng Finalised 0901Victor NgÎncă nu există evaluări

- HR Chapter 4 2 Eng Finalised0902Document14 paginiHR Chapter 4 2 Eng Finalised0902Victor Ng100% (1)

- Rev Ex For S4Document30 paginiRev Ex For S4Victor NgÎncă nu există evaluări

- HR Chapter 3 2 Eng Finalised0901Document15 paginiHR Chapter 3 2 Eng Finalised0901Victor NgÎncă nu există evaluări

- 3M First Assessment Oct 09-10Document8 pagini3M First Assessment Oct 09-10Victor NgÎncă nu există evaluări

- Ch11 WB eDocument44 paginiCh11 WB eVictor NgÎncă nu există evaluări

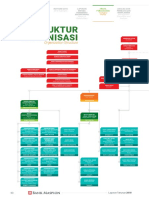

- Struktur Organisasi: Organization StructureDocument2 paginiStruktur Organisasi: Organization StructureRalila SejahteraÎncă nu există evaluări

- Accounting For Tania MamDocument24 paginiAccounting For Tania MamTanjinÎncă nu există evaluări

- Auditing Problems Ocampo/Soliman/Ocampo AP.2905-Audit of Receivables OCTOBER 2020Document7 paginiAuditing Problems Ocampo/Soliman/Ocampo AP.2905-Audit of Receivables OCTOBER 2020moÎncă nu există evaluări

- SodapdfDocument61 paginiSodapdfNicole Anne Santiago SibuloÎncă nu există evaluări

- Cash Flow Statement Format and ProblemsDocument21 paginiCash Flow Statement Format and ProblemsAnkit pattnaikÎncă nu există evaluări

- TEST As Accounting Double EntryDocument1 paginăTEST As Accounting Double EntryEdu TainmentÎncă nu există evaluări

- Chapter 10: Systems Design: Job-Order and Process CostingDocument38 paginiChapter 10: Systems Design: Job-Order and Process CostingNicole J. CentenoÎncă nu există evaluări

- SIMPLE INTEREST & COMPOUND INTEREST - 1st - Chapter PDFDocument6 paginiSIMPLE INTEREST & COMPOUND INTEREST - 1st - Chapter PDFarasuÎncă nu există evaluări

- Interests and Investment CostDocument16 paginiInterests and Investment CostAbdullah RamzanÎncă nu există evaluări

- Kombo WarrantDocument29 paginiKombo WarrantThe Valley IndyÎncă nu există evaluări

- 5.3 Income StatementDocument4 pagini5.3 Income StatementHiÎncă nu există evaluări

- Amazing RaceDocument6 paginiAmazing RaceHanns Lexter PadillaÎncă nu există evaluări

- Bcom Piecemeal Distribution of CashDocument6 paginiBcom Piecemeal Distribution of CashNeelam SarojÎncă nu există evaluări

- BIP 390 Investment Banking RegulationsDocument38 paginiBIP 390 Investment Banking RegulationsDuc Bui100% (2)

- Electronic Payment Systems For E-Commerce (2002)Document360 paginiElectronic Payment Systems For E-Commerce (2002)Trà MộcÎncă nu există evaluări

- BBA 8th Sem Regular T 20197112600889969486821Document117 paginiBBA 8th Sem Regular T 20197112600889969486821Torreus AdhikariÎncă nu există evaluări

- Executive Sell Trainee Program Succeed TogetherDocument28 paginiExecutive Sell Trainee Program Succeed TogetherParul AgarwalÎncă nu există evaluări

- Naresh Prajapati - Finance 19.03.2019Document4 paginiNaresh Prajapati - Finance 19.03.2019ShanaÎncă nu există evaluări

- Cagayan Executive Summary 2022Document5 paginiCagayan Executive Summary 2022Arjimar BaloyoÎncă nu există evaluări

- Principles of Auditing and Other Assurance Services 20Th Edition Whittington Solutions Manual Full Chapter PDFDocument43 paginiPrinciples of Auditing and Other Assurance Services 20Th Edition Whittington Solutions Manual Full Chapter PDFAndrewRobinsonixez100% (8)

- Risk Profiles of Islamic BankDocument31 paginiRisk Profiles of Islamic Bankkadung@gmail.comÎncă nu există evaluări

- Phone Pe Pay & Win Scheme For April To June'20Document4 paginiPhone Pe Pay & Win Scheme For April To June'20Prabhjot SinghÎncă nu există evaluări

- Ac OpeningDocument47 paginiAc OpeningKawoser AhammadÎncă nu există evaluări

- Cash Flow Indirect and DirectDocument2 paginiCash Flow Indirect and DirectKatherine Borja0% (1)

- Chapter 2 Cash and Cash EquivalentsDocument10 paginiChapter 2 Cash and Cash EquivalentsShe SalazarÎncă nu există evaluări

- Refunds Maceda Law and PD957Document2 paginiRefunds Maceda Law and PD957QUINTO CRISTINA MAEÎncă nu există evaluări

- E Zobel, Inc. vs. CA CDDocument1 paginăE Zobel, Inc. vs. CA CDJumen Gamaru TamayoÎncă nu există evaluări

- (Accounting) Chapter 3. Recording TransactionsDocument40 pagini(Accounting) Chapter 3. Recording TransactionsThùy DươngÎncă nu există evaluări

- FCFF and FcfeDocument23 paginiFCFF and FcfeSaurav VidyarthiÎncă nu există evaluări

- Viking Insurance Endorsement Confirmation for Added 1994 CorvetteDocument10 paginiViking Insurance Endorsement Confirmation for Added 1994 Corvettemesa1965Încă nu există evaluări