S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Jesusyouth Jesusyouth: Hope DarknessDocument16 paginiJesusyouth Jesusyouth: Hope Darknessjyjc_admÎncă nu există evaluări

- GEP January 2023Document198 paginiGEP January 2023bassÎncă nu există evaluări

- SocGen End of The Super Cycle 7-20-2011Document5 paginiSocGen End of The Super Cycle 7-20-2011Red911TÎncă nu există evaluări

- WQU FM Group Work Project InstructionsDocument6 paginiWQU FM Group Work Project InstructionsAhmed Sabry0% (1)

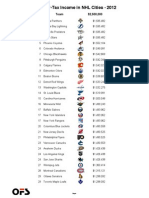

- Net After-Tax Income in NHL Cities - 2013: Team $2,500,000Document2 paginiNet After-Tax Income in NHL Cities - 2013: Team $2,500,000ericaaliniÎncă nu există evaluări

- Myanmar: Rice ExportDocument88 paginiMyanmar: Rice Exportericaalini100% (1)

- NHL 2013-2012Document1 paginăNHL 2013-2012ericaaliniÎncă nu există evaluări

- NHL 2013-2012Document1 paginăNHL 2013-2012ericaaliniÎncă nu există evaluări

- 2013 Single $2 5MDocument1 pagină2013 Single $2 5MVanna LeÎncă nu există evaluări

- NHL 2012Document1 paginăNHL 2012ericaaliniÎncă nu există evaluări

- Poloz Remarks Fina 06062013Document5 paginiPoloz Remarks Fina 06062013ericaaliniÎncă nu există evaluări

- Speech From The ThroneDocument24 paginiSpeech From The ThroneCPAC TV0% (1)

- Poloz Remarks 190613Document6 paginiPoloz Remarks 190613ericaaliniÎncă nu există evaluări

- Regearing Canadian Economic Growth Away From Household Debt - Bank of Canada (10 Jan 2013)Document27 paginiRegearing Canadian Economic Growth Away From Household Debt - Bank of Canada (10 Jan 2013)leithvanonselenÎncă nu există evaluări

- Globalisation, Financial Stability and EmploymentDocument10 paginiGlobalisation, Financial Stability and EmploymentericaaliniÎncă nu există evaluări

- Flemming Nytoft RasmussenDocument6 paginiFlemming Nytoft RasmussenAlezNgÎncă nu există evaluări

- Page 33 PDFDocument144 paginiPage 33 PDFDenise ValdezÎncă nu există evaluări

- Emerging Trends 2018Document103 paginiEmerging Trends 2018CrainsChicagoBusiness100% (3)

- The Economic Monitor U.S.: Free EditionDocument5 paginiThe Economic Monitor U.S.: Free EditionInternational Business TimesÎncă nu există evaluări

- The Asian Financial CrisisDocument19 paginiThe Asian Financial CrisisJohnny Cage100% (1)

- PBSA006 Accountancy Research Bernabe de Leon Diego 1Document113 paginiPBSA006 Accountancy Research Bernabe de Leon Diego 1Trisha DiegoÎncă nu există evaluări

- SecuritisationDocument28 paginiSecuritisationChinmayee ChoudhuryÎncă nu există evaluări

- GJBR V9N3 2015 3Document16 paginiGJBR V9N3 2015 3IJHRDS SRAKMÎncă nu există evaluări

- Financial Services: Securities Brokerage and Investment BankingDocument16 paginiFinancial Services: Securities Brokerage and Investment BankingSta KerÎncă nu există evaluări

- f9 02 The Financial Management EnvironmentDocument27 paginif9 02 The Financial Management EnvironmentGAURAVÎncă nu există evaluări

- Chapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Document27 paginiChapter 1 Economics of Money, Banking, and Financial Markets (5th Cad. Ed.)Edith KuaÎncă nu există evaluări

- In India Financial Management & Governance: A Roundtable DiscussionDocument24 paginiIn India Financial Management & Governance: A Roundtable DiscussionsviimaÎncă nu există evaluări

- Euro HY Xover 2008-09-17 UnicreditDocument334 paginiEuro HY Xover 2008-09-17 UnicreditVeraciousReaderÎncă nu există evaluări

- Harsco Investor PresentationDocument18 paginiHarsco Investor PresentationVincent C. CiepielÎncă nu există evaluări

- Real Estate Investment and FinanceDocument7 paginiReal Estate Investment and Financepatrick wafulaÎncă nu există evaluări

- Reflexivity Concept-George SorosDocument11 paginiReflexivity Concept-George SorosMartinÎncă nu există evaluări

- QE HouseOfLordsDocument68 paginiQE HouseOfLordsVincyÎncă nu există evaluări

- ASC Merit Decision - David JonesDocument33 paginiASC Merit Decision - David JonesCalgary HeraldÎncă nu există evaluări

- Transportation in Canada 2011 PDFDocument155 paginiTransportation in Canada 2011 PDFmenagesÎncă nu există evaluări

- Fiscal Stimulus - Pros and ConsDocument4 paginiFiscal Stimulus - Pros and ConsDillip KhuntiaÎncă nu există evaluări

- HSBC - China's Big BangDocument63 paginiHSBC - China's Big BangSunil KumarÎncă nu există evaluări

- Credit Valuation AdjustmentDocument14 paginiCredit Valuation Adjustmenttasneem chherawalaÎncă nu există evaluări

- Financial Distress Thesis-1Document80 paginiFinancial Distress Thesis-1Asaminew DesalegnÎncă nu există evaluări

- Charles Brandes' Q1 2015 Commentary - Seeking Pockets of Value in Divergent MarketsDocument10 paginiCharles Brandes' Q1 2015 Commentary - Seeking Pockets of Value in Divergent MarketsCharlie TianÎncă nu există evaluări

- Public Debt and Economic Growth-Is There A Change in ThresholdEffect - Hu - Xinruo - Honor ThesisDocument35 paginiPublic Debt and Economic Growth-Is There A Change in ThresholdEffect - Hu - Xinruo - Honor ThesisFitria GandiÎncă nu există evaluări

- Economic Crisis in Pakistan: Present Challenges, Causes, SolutionsDocument2 paginiEconomic Crisis in Pakistan: Present Challenges, Causes, SolutionsSiddaquat aliÎncă nu există evaluări