S-ar putea să vă placă și

- Premier Processing Loan AgreementDocument9 paginiPremier Processing Loan AgreementBob WeeksÎncă nu există evaluări

- Leadership Council Grow Primary Jobs: Update and DiscussionDocument13 paginiLeadership Council Grow Primary Jobs: Update and DiscussionBob WeeksÎncă nu există evaluări

- Report of The K-12 Student Performance and Efficiency Commission To The 2015 Kansas LegislatureDocument16 paginiReport of The K-12 Student Performance and Efficiency Commission To The 2015 Kansas LegislatureBob WeeksÎncă nu există evaluări

- Jeff Longwe Jeff Longwell Campaign Finance 2015-01-10 Mayorll Campaign Finance 2015-01-10 MayorDocument8 paginiJeff Longwe Jeff Longwell Campaign Finance 2015-01-10 Mayorll Campaign Finance 2015-01-10 MayorBob WeeksÎncă nu există evaluări

- Wichita Old Town Cinema TIF Update September 19, 2014Document6 paginiWichita Old Town Cinema TIF Update September 19, 2014Bob WeeksÎncă nu există evaluări

- Five-Year Budget Plan For The State of KansasDocument11 paginiFive-Year Budget Plan For The State of KansasBob WeeksÎncă nu există evaluări

- Wichita Sales Tax Vote, November 4, 2014Document4 paginiWichita Sales Tax Vote, November 4, 2014Bob WeeksÎncă nu există evaluări

- Development Plan For Downtown WichitaDocument121 paginiDevelopment Plan For Downtown WichitaBob WeeksÎncă nu există evaluări

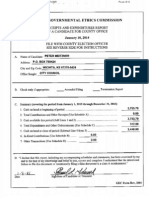

- Pete Meitzner Campaign Finance 2014-01-10Document5 paginiPete Meitzner Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- An Evaluation of The Kansas Affordable Airfares ProgramDocument40 paginiAn Evaluation of The Kansas Affordable Airfares ProgramBob WeeksÎncă nu există evaluări

- CEDBR Fiscal Model Presentation To Wichita City CouncilDocument14 paginiCEDBR Fiscal Model Presentation To Wichita City CouncilBob WeeksÎncă nu există evaluări

- Affordable Airfares Funding Agreement With Sedgwick County 2014-08-12Document15 paginiAffordable Airfares Funding Agreement With Sedgwick County 2014-08-12Bob WeeksÎncă nu există evaluări

- Resolution Considering The Establishment of The Union Station Redevelopment District (Tax Increment Financing)Document115 paginiResolution Considering The Establishment of The Union Station Redevelopment District (Tax Increment Financing)Bob WeeksÎncă nu există evaluări

- Sedgwick County Economic Development Incentives 2013 Status ReportDocument5 paginiSedgwick County Economic Development Incentives 2013 Status ReportBob WeeksÎncă nu există evaluări

- TIF History and Performance Report, Wichita 2011Document23 paginiTIF History and Performance Report, Wichita 2011Bob WeeksÎncă nu există evaluări

- Kansas Legislative Briefing Book, 2014Document411 paginiKansas Legislative Briefing Book, 2014Bob WeeksÎncă nu există evaluări

- State of The City Address 2014Document10 paginiState of The City Address 2014Bob WeeksÎncă nu există evaluări

- Tim Norton Campaign Finance 2014-01-10Document6 paginiTim Norton Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Karl Peterjohn Campaign Finance 2014-01-10Document3 paginiKarl Peterjohn Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Jeff Blubaugh Campaign Finance 2014-01-10Document7 paginiJeff Blubaugh Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Dave Unruh Campaign Finance 2014-01-10Document5 paginiDave Unruh Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Jim Howell Campaign Finance 2014-01-10Document6 paginiJim Howell Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Jim Skelton Campaign Finance 2014-01-10Document5 paginiJim Skelton Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Carolyn McGinn Campaign Finance 2014-01-10Document2 paginiCarolyn McGinn Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- James Clendenin Campaign Finance 2014-01-10Document5 paginiJames Clendenin Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Clinton Coen Campaign Finance 2014-01-10Document4 paginiClinton Coen Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

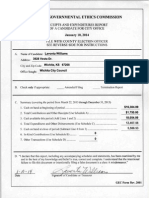

- Janet Miller Campaign Finance 2014-01-10Document3 paginiJanet Miller Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Lavonta Williams Campaign Finance 2014-01-10Document6 paginiLavonta Williams Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Joy Eakins Campaign Finance 2014-01-10Document5 paginiJoy Eakins Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- Jeff Longwell Campaign Finance 2014-01-10Document2 paginiJeff Longwell Campaign Finance 2014-01-10Bob WeeksÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Vice President Quality Operations in Greater Chicago IL Resume Kevin FredrichDocument2 paginiVice President Quality Operations in Greater Chicago IL Resume Kevin FredrichKevin Fredrich1Încă nu există evaluări

- According To India International Coffee Festival in The TitledDocument4 paginiAccording To India International Coffee Festival in The Titledsalman vavaÎncă nu există evaluări

- D8045-16 Standard Test Method For Acid Number of Crude Oils and Petroleum Products by CatalyticDocument6 paginiD8045-16 Standard Test Method For Acid Number of Crude Oils and Petroleum Products by CatalytichishamÎncă nu există evaluări

- GS Module 3 ConcessionDocument3 paginiGS Module 3 ConcessionManolacheÎncă nu există evaluări

- Surface Vehicle Recommended Practice: 400 Commonwealth Drive, Warrendale, PA 15096-0001Document20 paginiSurface Vehicle Recommended Practice: 400 Commonwealth Drive, Warrendale, PA 15096-0001Leonardo Gonçalves GomideÎncă nu există evaluări

- ND 0108 SpongeDiver SymiDocument2 paginiND 0108 SpongeDiver SymiPoki MokiÎncă nu există evaluări

- Fulltext PDFDocument55 paginiFulltext PDFManikandan VpÎncă nu există evaluări

- Material SelfDocument9 paginiMaterial Selfic perlasÎncă nu există evaluări

- Electric Vehicle in IndonesiaDocument49 paginiElectric Vehicle in IndonesiaGabriella Devina Tirta100% (1)

- SurveyDocument1 paginăSurveyJainne Ann BetchaidaÎncă nu există evaluări

- Midas Tutorial Fea 7Document3 paginiMidas Tutorial Fea 7sasiÎncă nu există evaluări

- Presentation 2Document70 paginiPresentation 2Vivek LathÎncă nu există evaluări

- Budget Reform ProgramDocument31 paginiBudget Reform ProgramSannyboy DatumanongÎncă nu există evaluări

- Water Distiller - ManualDocument2 paginiWater Distiller - ManualSanjeevi JagadishÎncă nu există evaluări

- hw410 Unit 9 Assignment 1Document8 paginihw410 Unit 9 Assignment 1api-600248850Încă nu există evaluări

- OGJ Worldwide Refining Survey 2010Document67 paginiOGJ Worldwide Refining Survey 2010Zahra GhÎncă nu există evaluări

- 01 Head and Neck JMDocument16 pagini01 Head and Neck JMJowi SalÎncă nu există evaluări

- Leadership 29Document32 paginiLeadership 29Efe AgbozeroÎncă nu există evaluări

- Lesson 3.3 Inside An AtomDocument42 paginiLesson 3.3 Inside An AtomReign CallosÎncă nu există evaluări

- Fan Tool Kit - Ad Hoc Group - V4ddDocument121 paginiFan Tool Kit - Ad Hoc Group - V4ddhmaza shakeelÎncă nu există evaluări

- Afcat Question Paper 01-2014 PDFDocument10 paginiAfcat Question Paper 01-2014 PDFTuhin AzadÎncă nu există evaluări

- UNIT-5 International Dimensions To Industrial Relations: ObjectivesDocument27 paginiUNIT-5 International Dimensions To Industrial Relations: ObjectivesManish DwivediÎncă nu există evaluări

- AssaultDocument12 paginiAssaultEd Mundo100% (3)

- Liquid Fertilizer PresentationDocument17 paginiLiquid Fertilizer PresentationAnna RothÎncă nu există evaluări

- Kmartinez Draft Research PaperDocument14 paginiKmartinez Draft Research Paperapi-273007806Încă nu există evaluări

- Types of ProcurementDocument7 paginiTypes of ProcurementrahulÎncă nu există evaluări

- Formula Sheet Pre-MidDocument4 paginiFormula Sheet Pre-MidUzair KhanÎncă nu există evaluări

- Gerardus Johannes Mulder: 20 Aug 1779 - 7 Aug 1848Document25 paginiGerardus Johannes Mulder: 20 Aug 1779 - 7 Aug 1848NihalÎncă nu există evaluări

- Jurnal Kasus Etikolegal Dalam Praktik KebidananDocument13 paginiJurnal Kasus Etikolegal Dalam Praktik KebidananErni AnggieÎncă nu există evaluări

- A&P Exam 2 ReviewDocument7 paginiA&P Exam 2 ReviewKathleen SaucedoÎncă nu există evaluări