S-ar putea să vă placă și

- Payment Systems Part 1Document282 paginiPayment Systems Part 1ashimadania100% (2)

- RTGSDocument14 paginiRTGSHarshUpadhyayÎncă nu există evaluări

- Payment Settlement System in Us: Presented By: Heninle Magh ROLL-7Document24 paginiPayment Settlement System in Us: Presented By: Heninle Magh ROLL-7Henny SebÎncă nu există evaluări

- Clearing and Payment System Within The CountryDocument4 paginiClearing and Payment System Within The CountryHardik Malde100% (1)

- International Remittances: Business Process Outsourcing Consulting System Integration Universal Banking SolutionDocument11 paginiInternational Remittances: Business Process Outsourcing Consulting System Integration Universal Banking Solutionakther_aisÎncă nu există evaluări

- Electronic Financial Services: Technology and ManagementDe la EverandElectronic Financial Services: Technology and ManagementEvaluare: 5 din 5 stele5/5 (1)

- All About Swift Software in BanksDocument15 paginiAll About Swift Software in BanksDeepthi RavichandhranÎncă nu există evaluări

- Payment, Clearing and Settlement Systems in The United States (BIS)Document38 paginiPayment, Clearing and Settlement Systems in The United States (BIS)Ji_y100% (2)

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsDe la EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsÎncă nu există evaluări

- Treasury management A Complete Guide - 2019 EditionDe la EverandTreasury management A Complete Guide - 2019 EditionÎncă nu există evaluări

- ACH Payments ExplainedDocument12 paginiACH Payments ExplainedshaileshawasthiÎncă nu există evaluări

- Payment SystemsDocument7 paginiPayment SystemsGanesh ShankarÎncă nu există evaluări

- Private Banking ProcessesDocument18 paginiPrivate Banking Processescogosnofla123Încă nu există evaluări

- Innovation in Banking: A Review From The Point of View of Corporate GovernanceDocument35 paginiInnovation in Banking: A Review From The Point of View of Corporate GovernanceMj PorcionculaÎncă nu există evaluări

- Payment Processing: - Murali KrishnaDocument57 paginiPayment Processing: - Murali KrishnaRAVITEJA100% (1)

- Demat AccountDocument8 paginiDemat Account29.Kritika SinghÎncă nu există evaluări

- Electronic Fund TransferDocument19 paginiElectronic Fund Transfersandhya kumarÎncă nu există evaluări

- Closing of Bank AccountDocument15 paginiClosing of Bank AccountGurpreet Singh100% (1)

- What Is Revolving Credit?Document3 paginiWhat Is Revolving Credit?Niño Rey LopezÎncă nu există evaluări

- Wire Remittance Domestic Best PracticesDocument10 paginiWire Remittance Domestic Best PracticesBernardo AlbaÎncă nu există evaluări

- Fixed Income Securities: IntroductionDocument33 paginiFixed Income Securities: IntroductionYogaPratamaDosen100% (1)

- Rights of Drawers Banks and Holders in Bank Checks and Other CADocument57 paginiRights of Drawers Banks and Holders in Bank Checks and Other CASiddharth Singh TomarÎncă nu există evaluări

- Open BankingDocument23 paginiOpen BankingJayesh BaliÎncă nu există evaluări

- Banking SoftwaresDocument3 paginiBanking Softwaressri3680Încă nu există evaluări

- Electronic Payment SystemsDocument20 paginiElectronic Payment SystemsHinaJhaveriÎncă nu există evaluări

- Rebuilding Operating Model Credit Card CompaniesDocument4 paginiRebuilding Operating Model Credit Card CompaniesapluÎncă nu există evaluări

- Payment and Clearing SystemDocument33 paginiPayment and Clearing Systemare_rool86Încă nu există evaluări

- Overview-US Payment Systems 5122019 313PMDocument16 paginiOverview-US Payment Systems 5122019 313PMMartin HardingÎncă nu există evaluări

- Treasury BillsDocument35 paginiTreasury BillsPatel Akki100% (1)

- What Is SWIFT in International Banking?Document15 paginiWhat Is SWIFT in International Banking?forcetenÎncă nu există evaluări

- Int RemittanceDocument7 paginiInt Remittanceግሩም ሽ.Încă nu există evaluări

- Payment Message PDFDocument9 paginiPayment Message PDFPrachi SaxenaÎncă nu există evaluări

- SWIFTDocument15 paginiSWIFTArushi Gupta100% (2)

- Certification in Payment Systems Part 2Document159 paginiCertification in Payment Systems Part 2ashimadania100% (3)

- Borrower in Custody (BIC) ArrangementsDocument15 paginiBorrower in Custody (BIC) ArrangementsMichael Focia100% (1)

- US Internal Revenue Service: p3381Document3 paginiUS Internal Revenue Service: p3381IRSÎncă nu există evaluări

- Features of Credit CardDocument11 paginiFeatures of Credit CardBipin ThakorÎncă nu există evaluări

- Client Manual Consumer Banking - CitibankDocument29 paginiClient Manual Consumer Banking - CitibankNGUYEN HUU THUÎncă nu există evaluări

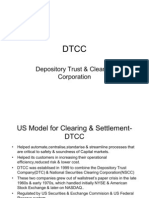

- DTCCDocument10 paginiDTCCpoojasengar100% (1)

- Plastic MoneyDocument39 paginiPlastic Moneydakshaangel100% (3)

- Erma AND MICR PowerpointDocument13 paginiErma AND MICR PowerpointJonathan Realis Capilo100% (1)

- Bank Draw Down Request 1031 Fedwire Definition Info The DifferenceDocument2 paginiBank Draw Down Request 1031 Fedwire Definition Info The DifferenceMikeDouglas0% (1)

- Credit Card Operations of BanksDocument11 paginiCredit Card Operations of Bankssantucan2Încă nu există evaluări

- Moving To E-PaymentsDocument8 paginiMoving To E-PaymentsJulieth Alejandra Vargas OchoaÎncă nu există evaluări

- Commercial Credit InstrumentsDocument7 paginiCommercial Credit Instrumentsinnnaaahhh1234567100% (3)

- Assignment ON Bills DiscountingDocument9 paginiAssignment ON Bills DiscountingparuljainibmrÎncă nu există evaluări

- DEBT Tutoria BankingDocument21 paginiDEBT Tutoria BankingJenniferÎncă nu există evaluări

- Electric Funds Transfer PDFDocument93 paginiElectric Funds Transfer PDFlifeisgrand100% (1)

- Check List of Foreign Exchange Transaction in BankDocument20 paginiCheck List of Foreign Exchange Transaction in BankMohammad RokunuzzamanÎncă nu există evaluări

- Digital Transformation of U.S. Private BankingDocument9 paginiDigital Transformation of U.S. Private BankingCognizantÎncă nu există evaluări

- SAR InstructionsDocument3 paginiSAR InstructionsMikeDouglas100% (2)

- Electronic Funds TransferDocument14 paginiElectronic Funds TransferRaj KumarÎncă nu există evaluări

- Electronic Payment Systems: Presented By: Salman Touheed Tariq Rashid Faizan ZafarDocument45 paginiElectronic Payment Systems: Presented By: Salman Touheed Tariq Rashid Faizan ZafarsalmantouheedÎncă nu există evaluări

- Banking Operations (MAIN TOPICS)Document32 paginiBanking Operations (MAIN TOPICS)Saqib ShahzadÎncă nu există evaluări

- Legal Entity IdentifierDocument1 paginăLegal Entity IdentifierRaja SekharÎncă nu există evaluări

- Federal Reserve Personal Finance 2017Document16 paginiFederal Reserve Personal Finance 2017api-354625480Încă nu există evaluări

- My - Bill - 11 Apr, 2023 - 10 May, 2023 - 300886936899-1Document2 paginiMy - Bill - 11 Apr, 2023 - 10 May, 2023 - 300886936899-1Abhijnyan ChandraÎncă nu există evaluări

- Statement of Account For Period:: AOCPM7203D Yes Registered ## LinkedDocument2 paginiStatement of Account For Period:: AOCPM7203D Yes Registered ## LinkedAnonymous CbpO95CÎncă nu există evaluări

- Cash Management SOPDocument13 paginiCash Management SOPnisha100% (3)

- OjhaDocument84 paginiOjhaRishu OjhaÎncă nu există evaluări

- Bank Service PricingDocument12 paginiBank Service PricingworkulemaÎncă nu există evaluări

- CBS P2Document11 paginiCBS P2sam vargheseÎncă nu există evaluări

- Personal Account Opening Form - 221219 - 113037Document6 paginiPersonal Account Opening Form - 221219 - 113037Tounkara MohamedÎncă nu există evaluări

- TeplateDocument8 paginiTeplatejigyasha oarmarÎncă nu există evaluări

- Gap Analysis of Services Offered in Retail BankingDocument92 paginiGap Analysis of Services Offered in Retail Bankingjignay100% (18)

- BillDocument10 paginiBillHimanshu PandeyÎncă nu există evaluări

- Fluoride: Quarterly Journal of The International Society For Fluoride Research IncDocument6 paginiFluoride: Quarterly Journal of The International Society For Fluoride Research IncNain NoorÎncă nu există evaluări

- MembershipContract PDFDocument2 paginiMembershipContract PDFbobgreen19870% (1)

- Africa Sugar 2014 WEBDocument6 paginiAfrica Sugar 2014 WEBanilmeherÎncă nu există evaluări

- Rajesh Agarwal V StateDocument11 paginiRajesh Agarwal V StateChaitanya AroraÎncă nu există evaluări

- FM - Amreli Nagrik Bank - 2Document84 paginiFM - Amreli Nagrik Bank - 2jagrutisolanki01Încă nu există evaluări

- Final OCP ReportDocument42 paginiFinal OCP ReportsaifulrizviÎncă nu există evaluări

- Ting Pua V Spouses Tiong and Teng (2013)Document3 paginiTing Pua V Spouses Tiong and Teng (2013)caaam823Încă nu există evaluări

- College Information Sheet Medical 05.11.2020Document23 paginiCollege Information Sheet Medical 05.11.2020kvpy iisc bangloreÎncă nu există evaluări

- Travellers ChequeDocument4 paginiTravellers ChequeVinod Yb0% (1)

- 2nd Phase Challan NH - MP FinalDocument1 pagină2nd Phase Challan NH - MP FinalBilalTariqÎncă nu există evaluări

- Opening Balance - 3776793.50Document40 paginiOpening Balance - 3776793.50DIVYANSHU CHATURVEDIÎncă nu există evaluări

- MS Parent Bulletin (Week of May 22 To 26)Document11 paginiMS Parent Bulletin (Week of May 22 To 26)International School ManilaÎncă nu există evaluări

- 157 GDocument14 pagini157 GMedo SaeediÎncă nu există evaluări

- Trisakti School of Management Sekolah Tinggi Ilmu Ekonomi Trisakti Jakarta Course DescriptionDocument4 paginiTrisakti School of Management Sekolah Tinggi Ilmu Ekonomi Trisakti Jakarta Course Descriptiondea AudreylaÎncă nu există evaluări

- DG Rental Structure - 01-Mar-2022Document2 paginiDG Rental Structure - 01-Mar-2022Hozayfa Abdel RahimÎncă nu există evaluări

- Liberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationDocument3 paginiLiberty General Insurance Limited: Insured Motor Vehicle Details and Premium ComputationAbcÎncă nu există evaluări

- Garlic Jim's Opening Closing ProceduresDocument13 paginiGarlic Jim's Opening Closing ProceduresRedondo Bruno100% (1)

- Agricultural Produce Marketing Committee, Srinivasapura Telephone: FaxDocument46 paginiAgricultural Produce Marketing Committee, Srinivasapura Telephone: FaxTender TenderÎncă nu există evaluări

- Iphone 11 Imagine PDFDocument2 paginiIphone 11 Imagine PDFJonassy SumaïliÎncă nu există evaluări

- CPAR AP - Audit of CashDocument9 paginiCPAR AP - Audit of CashJohn Carlo CruzÎncă nu există evaluări