Chapter 7 Statement of Cash Flows Purpose of a statement of cash flows Statement of Cash Flows = reports an entitys cash inflows

ows & outflows for a specific period. Prepared on a cash basis & IS is prepared on an accrual basis. Important for working capital management of an entity. Working capital is needed to fund inventory & debtors while awaiting receipts from sales. o Working capital = difference b/w amounts of current assets & current liabilities

o o The # of times an entity can cycle through ^ process generally the more profit it can make (@ appropriate prices)

Chapter 7 Statement of Cash Flows

Difference b/w cash & accrual accounting

According to the income statement, profit made = $7900. Alexandra also purchased & paid $6000 worth of hair products, but the cost of products sold during the month = $5600. (The other $400 will form part of inventory & be recorded as an asset)

The statement of cash flows shows that the entitys cash position is -$4000 (i.e. the bank acc is in overdraft). A comparison shows that although the company was quite profitable, the business will have trouble meeting its financial obligations. Although income of $20,000 was generated, only $5000 of sales were collected in cash.

For an entity to survive, the net cash flows from OPERATING ACTIVITIES should be positive.

Why is a statement of cash flows needed?

It summarizes the cash & types of cash flows coming into and flowing out of the entity . For instance, if the entity received cash from bank loans but no cash as coming into the entity through normal operations, it would indicate that the business isnt a good investment. Likewise, if ample cash came in through its normal operations, therefore had no need for cash from borrowing a good entity to invest in.

Chapter 7 Statement of Cash Flows

Relationship of the statement of cash flows to other financial statements

It helps identify changes in balance sheet items. E.g. the sale or purchase of an asset for cash would have an effect on both the BS & the statement of cash flows. Borrowing money & paying a dividend will also affect both statements.

Its purpose is to give additional info to that provided by other statements. Generally, info provided should assist decision makers in assessing an entitys ability to: o o o o Generate cash flows Meet financial commitments, including servicing of borrowings + payment of dividends Fund changes in scope of its activities Obtain external finance

Relationship between items in the statement of cash flows & the income statement & BS

Chapter 7 Statement of Cash Flows CASH = cash and cash equivalents Cash on hand notes & coins & deposits at call w/ a financial institution Cash equivalents highly liquid investments & short-term borrowings

Format & classification of cash flows in the statement of cash flows

Operating activities activities relate to the provision of G+S and other activities that are neither investing nor financing activities. E.g. cash sale of G+S, cash received from customers, receipt of interest/dividends, payment to suppliers, payment of salaries & wages, payment of tax & interest o Normally profit would be lower than cash from operating activities as profit includes non-cash deductions e.g. depreciation & amortisation

Investing activities activities relate to the acquisition and/or disposal of non-current assets (e.g. PPE) not falling within the definition of cash o E.g. sale of PPE, sale of shares, collection of loans from other entities, purchase of PPE, purchase of shares, lending of money o o An entity has to invest in order to generate future income & cash flows. If an entity has a desire to grow, net cash flow from investing activity would be negative

Financing activities activities that change the size and/or composition of the financial structure of the entity (including equity) and borrowings not falling within the definition of cash. o Activities generally associated w/ changes in non-current liabilities & equity (i.e. cash received from the issue of shares/debt MINUS cash paid to shareholders/to repay debt) o E.g. issue of the entitys own shares, cash from borrowings, dividends paid to shareholders, repurchase of shares from shareholders etc. o Usually +ve inflow of cash from financing activities as generally entities borrow cash to fund expansion healthy step to growth o If over a long period of time borrowings are significant & the cash from operating activities is struggling to pay interest costs solvency problem o Paying cash out to owners weakens financial position of entity as it results in less money being available for creditors & for the purchase of investments o Why do entities buy back shares? Generally entities buy back shares if they have surplus funds & there are no immediate worthwhile investments that could earn the required rate of return Having excess cash sitting on the BS earning minimal interest from a financial institution decreases the overall return on equity for the entity

Chapter 7 Statement of Cash Flows

Reconciliation of cash from operating activities w/ operating profit

The reconciliation of cash from operating activities w/ profit from income statement is presented to reinforce the link b/w the cash received from operating activities & the profit/loss reported in the income statement

Producing a statement of cash flows using the direct method & a reconciliation using the indirect method

Direct method discloses major classes of gross cash receipts & gross cash payments Indirect method adjusts profit/loss for the effects of transactions of a non-cash nature & deferrals/accruals of operating revenue & expense.

If the balance of prepayments increases then we have paid more for expenses, thus decreasing cash flow If the balance of accruals increases then we have a greater amount owing and have therefore paid less, thus increasing cash flow

S-ar putea să vă placă și

- Farparcor 2 Chapter 1 Exercises Problem AnswersDocument10 paginiFarparcor 2 Chapter 1 Exercises Problem AnswersWillnie Shane LabaroÎncă nu există evaluări

- Diagnostic AssessmentDocument7 paginiDiagnostic AssessmentChristine JoyceÎncă nu există evaluări

- Jeremeh V Querol Bachelor of Science in Tourism ManagementDocument8 paginiJeremeh V Querol Bachelor of Science in Tourism ManagementJasmine ActaÎncă nu există evaluări

- Partnership FormationDocument3 paginiPartnership Formationmiss independent100% (1)

- ACCOUNTING123Document5 paginiACCOUNTING123April Vinas SabusapÎncă nu există evaluări

- Ch. 1 HW Solutions-9eDocument19 paginiCh. 1 HW Solutions-9eNgÎncă nu există evaluări

- PARTNERSHIPDocument84 paginiPARTNERSHIPJohn Rey LabasanÎncă nu există evaluări

- IM3 Partnership Operations ProblemsDocument4 paginiIM3 Partnership Operations ProblemsXivaughn Sebastian0% (1)

- AdjustmentDocument5 paginiAdjustmentBeta TesterÎncă nu există evaluări

- The Partnership OperationDocument24 paginiThe Partnership OperationMarieCuÎncă nu există evaluări

- Chapter 1 Problem 5 To 7Document2 paginiChapter 1 Problem 5 To 7XienaÎncă nu există evaluări

- Midterm Bi ADocument13 paginiMidterm Bi AFabiana BarbeiroÎncă nu există evaluări

- Cost of Capital NotesDocument34 paginiCost of Capital Notesyahspal singhÎncă nu există evaluări

- Discussion Questions On Partnership OperationsDocument1 paginăDiscussion Questions On Partnership OperationsCeejay MancillaÎncă nu există evaluări

- Far Deptals ReviewerDocument6 paginiFar Deptals Revieweranon_127895200Încă nu există evaluări

- Final Term Assignment 2 On Financial Accounting and Reporting - Partnership OperationsDocument2 paginiFinal Term Assignment 2 On Financial Accounting and Reporting - Partnership OperationsAnne AlagÎncă nu există evaluări

- Hbo Chapter 18Document6 paginiHbo Chapter 18Diosdado IV GALVEZÎncă nu există evaluări

- Accounting For Special TransactionsDocument43 paginiAccounting For Special TransactionsNezer VergaraÎncă nu există evaluări

- Installment Liquidation 2Document3 paginiInstallment Liquidation 2Jamie RamosÎncă nu există evaluări

- Conceptual Framework Qualitative CharacteristicDocument99 paginiConceptual Framework Qualitative CharacteristicXander Clock0% (1)

- Chapter 2 Cost Concepts and ClassificationDocument40 paginiChapter 2 Cost Concepts and ClassificationJean Rae RemiasÎncă nu există evaluări

- Acquirer Obtains Control of One or More Businesses.: ConceptDocument6 paginiAcquirer Obtains Control of One or More Businesses.: ConceptJohn Lexter MacalberÎncă nu există evaluări

- Book 1Document57 paginiBook 1Alex Richard CarlosÎncă nu există evaluări

- Capital Budgeting - NotesDocument7 paginiCapital Budgeting - NotesnerieroseÎncă nu există evaluări

- Semi Final Exam (Accounting)Document4 paginiSemi Final Exam (Accounting)MyyMyy JerezÎncă nu există evaluări

- Diagnostic Test CashDocument2 paginiDiagnostic Test CashJoannah maeÎncă nu există evaluări

- 2020 T3 GSBS6410 Lecture Notes For Week 1 IntroductionDocument35 pagini2020 T3 GSBS6410 Lecture Notes For Week 1 IntroductionRenu JhaÎncă nu există evaluări

- This Study Resource Was: B. Increase in Asset and Decrease in AssetDocument5 paginiThis Study Resource Was: B. Increase in Asset and Decrease in Assetvworldpeace yanibÎncă nu există evaluări

- Actor Si RizalDocument6 paginiActor Si RizalRezzmah Alicia Tomon KhadrawyÎncă nu există evaluări

- MMW-Activity 2 - MathLLogicDocument1 paginăMMW-Activity 2 - MathLLogicKris CruzÎncă nu există evaluări

- Financial Transaction WorksheetDocument3 paginiFinancial Transaction Worksheetjen 01Încă nu există evaluări

- Interest Rates and Bond ValuationDocument75 paginiInterest Rates and Bond ValuationOday Ru100% (1)

- Advanced Pricing Techniques: Ninth Edition Ninth EditionDocument28 paginiAdvanced Pricing Techniques: Ninth Edition Ninth EditionMosiur RahmanÎncă nu există evaluări

- Stratma Quiz1Document4 paginiStratma Quiz1Patricia CruzÎncă nu există evaluări

- Errors of Trial BalanceDocument2 paginiErrors of Trial BalanceCaitlene Lee UyÎncă nu există evaluări

- CH 5 - AdjustmentsDocument24 paginiCH 5 - Adjustmentsmuhamad elmiÎncă nu există evaluări

- CFAS - Chapter 26Document49 paginiCFAS - Chapter 26Syrell NaborÎncă nu există evaluări

- M03 Gitman50803X 14 MF C03Document65 paginiM03 Gitman50803X 14 MF C03layan123456Încă nu există evaluări

- Suggested AnswersDocument18 paginiSuggested AnswersEl YangÎncă nu există evaluări

- Accounting For Partnership FormationDocument28 paginiAccounting For Partnership FormationKrislyn Audrey Chan CresciniÎncă nu există evaluări

- CH 07Document39 paginiCH 07Shahnawaz KhanÎncă nu există evaluări

- Darantan, KC T. - FAR Module 6Document3 paginiDarantan, KC T. - FAR Module 6Li LiÎncă nu există evaluări

- Gratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: AnDocument5 paginiGratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: Ankristine torresÎncă nu există evaluări

- PartnershipDocument20 paginiPartnershipYudna YuÎncă nu există evaluări

- Quiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeDocument6 paginiQuiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeJOHN MITCHELL GALLARDOÎncă nu există evaluări

- Property, Plant, and Equipment: Acquisition and Disposal: Chapter ObjectivesDocument20 paginiProperty, Plant, and Equipment: Acquisition and Disposal: Chapter ObjectivesCatherine Joy MoralesÎncă nu există evaluări

- Getalado, Jericho M.Document18 paginiGetalado, Jericho M.Ruth Getalado0% (1)

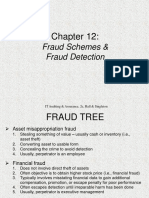

- Ch12 Fraud Scheme DetectionDocument18 paginiCh12 Fraud Scheme DetectionPanda BoarsÎncă nu există evaluări

- Wala LangDocument8 paginiWala LangMax Dela TorreÎncă nu există evaluări

- Essay 1 - Non-Financial InformationDocument3 paginiEssay 1 - Non-Financial InformationSeiniÎncă nu există evaluări

- The Global EconomyDocument17 paginiThe Global EconomyAlliana HaneÎncă nu există evaluări

- BroadeningDocument6 paginiBroadeningmarketingbufordrdÎncă nu există evaluări

- ACCY 301 Day 19 Class Notes CompleteDocument11 paginiACCY 301 Day 19 Class Notes Completekk sdfÎncă nu există evaluări

- Catherine-: Thank You Miss Christal. So What Is Net Present ValueDocument4 paginiCatherine-: Thank You Miss Christal. So What Is Net Present Valueenircm etsomalÎncă nu există evaluări

- ABM 002 Teacher Day 17Document9 paginiABM 002 Teacher Day 17Darelle Hannah MarquezÎncă nu există evaluări

- ACC 1802 Partneship OperationsDocument3 paginiACC 1802 Partneship OperationsronnelÎncă nu există evaluări

- Cash Flow StatementDocument10 paginiCash Flow Statementhitesh26881Încă nu există evaluări

- Fund Flow StatementDocument16 paginiFund Flow StatementRavi RajputÎncă nu există evaluări

- Operating Activities:: What Are The Classification of Cash Flow?Document5 paginiOperating Activities:: What Are The Classification of Cash Flow?samm yuuÎncă nu există evaluări

- Music Makes You SmarterDocument9 paginiMusic Makes You SmarterkajsdkjqwelÎncă nu există evaluări

- Investments Revision NotesDocument3 paginiInvestments Revision NoteskajsdkjqwelÎncă nu există evaluări

- Formula SheetDocument1 paginăFormula SheetkajsdkjqwelÎncă nu există evaluări

- BSBMGT401A Assess Part B Element 3Document1 paginăBSBMGT401A Assess Part B Element 3kajsdkjqwelÎncă nu există evaluări

- Student Example Report DellDocument42 paginiStudent Example Report DellkajsdkjqwelÎncă nu există evaluări

- TUTORIAL 3 - Case & Questions (PEDIGREE Adoption Drive)Document7 paginiTUTORIAL 3 - Case & Questions (PEDIGREE Adoption Drive)kajsdkjqwelÎncă nu există evaluări

- Chapter 2 Business SustainabilityDocument4 paginiChapter 2 Business SustainabilitykajsdkjqwelÎncă nu există evaluări

- French HistoriographyDocument5 paginiFrench Historiographykajsdkjqwel100% (1)

- Chapter 5 Balance SheetDocument9 paginiChapter 5 Balance SheetkajsdkjqwelÎncă nu există evaluări

- Chapter 1 Introduction To AccountingDocument7 paginiChapter 1 Introduction To AccountingkajsdkjqwelÎncă nu există evaluări

- IFA Week 3 Tutorial Solutions Brockville SolutionsDocument9 paginiIFA Week 3 Tutorial Solutions Brockville SolutionskajsdkjqwelÎncă nu există evaluări

- French HistoriographyDocument5 paginiFrench Historiographykajsdkjqwel100% (1)

- BSBITU402A Dev Use Complex Spreadsheets Assess4Document6 paginiBSBITU402A Dev Use Complex Spreadsheets Assess4kajsdkjqwelÎncă nu există evaluări

- Sample Completed OHS TrainingNeedsPlanDocument1 paginăSample Completed OHS TrainingNeedsPlankajsdkjqwelÎncă nu există evaluări

- Summary SheetDocument4 paginiSummary SheetkajsdkjqwelÎncă nu există evaluări

- Answering Assignment QuestionsDocument4 paginiAnswering Assignment Questionskajsdkjqwel100% (1)

- ThemesDocument2 paginiThemeskajsdkjqwelÎncă nu există evaluări

- Task 4 - Employee Performance AppraisalDocument1 paginăTask 4 - Employee Performance AppraisalkajsdkjqwelÎncă nu există evaluări

- Safe Work Procedure Step LadderDocument1 paginăSafe Work Procedure Step LadderkajsdkjqwelÎncă nu există evaluări

- Third Party Report: BSBLED401A Develop Teams and Individuals - Task 3Document2 paginiThird Party Report: BSBLED401A Develop Teams and Individuals - Task 3kajsdkjqwelÎncă nu există evaluări

- Chapter 6 Income Statement & Statement of Changes in EquityDocument7 paginiChapter 6 Income Statement & Statement of Changes in EquitykajsdkjqwelÎncă nu există evaluări

- Intro Micro Assignment 1Document12 paginiIntro Micro Assignment 1kajsdkjqwelÎncă nu există evaluări

- Sample OHS TrainingNeedsAnalysisDocument2 paginiSample OHS TrainingNeedsAnalysiskajsdkjqwelÎncă nu există evaluări

- ECON10005 Lecture 3Document11 paginiECON10005 Lecture 3kajsdkjqwelÎncă nu există evaluări

- Training Plan BSB40207Document1 paginăTraining Plan BSB40207kajsdkjqwelÎncă nu există evaluări

- Sample OHS TrainingNeedsAnalysisDocument2 paginiSample OHS TrainingNeedsAnalysiskajsdkjqwelÎncă nu există evaluări

- Sample Completed OHS TrainingNeedsPlanDocument1 paginăSample Completed OHS TrainingNeedsPlankajsdkjqwelÎncă nu există evaluări

- MSFW13 Volunteer Position Description - Event AssistantDocument1 paginăMSFW13 Volunteer Position Description - Event AssistantkajsdkjqwelÎncă nu există evaluări

- Chapter 1 Introduction To AccountingDocument7 paginiChapter 1 Introduction To AccountingkajsdkjqwelÎncă nu există evaluări

- Working Capital Management Analysis PreentationDocument29 paginiWorking Capital Management Analysis PreentationREYNARD CATAQUEZÎncă nu există evaluări

- 아너스기출 고2 천재이재영3과 - 답지Document5 pagini아너스기출 고2 천재이재영3과 - 답지채린Încă nu există evaluări

- Going To The BeachDocument3 paginiGoing To The BeachIndah Dwi CahayanyÎncă nu există evaluări

- Credit Skills For Bankers Certificate Sme IndiaDocument4 paginiCredit Skills For Bankers Certificate Sme IndiaitsurarunÎncă nu există evaluări

- Mensah EvansDocument85 paginiMensah EvansHadyan WidyadhanaÎncă nu există evaluări

- Ace of Capital MarketsDocument4 paginiAce of Capital MarketsAmit GuptaÎncă nu există evaluări

- HFO HomeworkDocument2 paginiHFO HomeworkAna May Durante BaldelomarÎncă nu există evaluări

- Project Manager Construction Real Estate Development in Los Angeles CA Resume Rey AdalinDocument2 paginiProject Manager Construction Real Estate Development in Los Angeles CA Resume Rey AdalinReyAdalinÎncă nu există evaluări

- Indian CEO's List in Big U.S. Companies: Indira NooyiDocument12 paginiIndian CEO's List in Big U.S. Companies: Indira Nooyishubham_garg_15100% (1)

- Aspiration Bank 2020Document6 paginiAspiration Bank 2020SAM0% (1)

- ZM Ez 0 WSC LMR IzuzaDocument5 paginiZM Ez 0 WSC LMR IzuzaRama KrishnaÎncă nu există evaluări

- KOBIL - PSD2 - 7 Layers of SecurityDocument4 paginiKOBIL - PSD2 - 7 Layers of Securityvlado10305Încă nu există evaluări

- Compoun Interest LessonDocument6 paginiCompoun Interest Lessonsonamaegarcia23Încă nu există evaluări

- Anitha HDFCDocument84 paginiAnitha HDFCchaluvadiinÎncă nu există evaluări

- Banking Customer SatisfactionDocument34 paginiBanking Customer SatisfactionMohan kumar K.SÎncă nu există evaluări

- The Philippine National Bank Was Established As A GovernmentDocument7 paginiThe Philippine National Bank Was Established As A GovernmentIris Valerie Bontia CabunilasÎncă nu există evaluări

- Chile 1970-1973, Economic Development and Its International Setting. Institute of Social StudiesDocument423 paginiChile 1970-1973, Economic Development and Its International Setting. Institute of Social StudiesdavidizanagiÎncă nu există evaluări

- Jones Finac Ce Ch02Document32 paginiJones Finac Ce Ch02AnindhytaÎncă nu există evaluări

- Philippine National Bank Vs DeeDocument3 paginiPhilippine National Bank Vs DeeJezenEstherB.PatiÎncă nu există evaluări

- Comprehensive NotesDocument13 paginiComprehensive NotesBelle Andrea GozonÎncă nu există evaluări

- Project ReportDocument68 paginiProject ReportPanav MohindraÎncă nu există evaluări

- Social Media As A Way of Fostering Financial Inclusion To Marginalized Rural CommunitiesDocument9 paginiSocial Media As A Way of Fostering Financial Inclusion To Marginalized Rural CommunitiesInternational Journal of Business Marketing and ManagementÎncă nu există evaluări

- Banking SectorDocument8 paginiBanking SectorSupreet KaurÎncă nu există evaluări

- Trends and Outlook For BNPLDocument47 paginiTrends and Outlook For BNPLBetsy Alexandra TaypeÎncă nu există evaluări

- Irda Forms - Ia / Ib / IcDocument15 paginiIrda Forms - Ia / Ib / IcSenthil KumarÎncă nu există evaluări

- 5.4 Statement of Financial PositionDocument4 pagini5.4 Statement of Financial PositionHiÎncă nu există evaluări

- Cash and Cash Equivalents: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriDocument66 paginiCash and Cash Equivalents: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriTessang OnongenÎncă nu există evaluări

- Presentation 4 Sales and LeaseDocument106 paginiPresentation 4 Sales and Leaselouise_canlas_1Încă nu există evaluări

- United States Geological Survey Certificate of Analysis: Green River Shale, SGR-1Document3 paginiUnited States Geological Survey Certificate of Analysis: Green River Shale, SGR-1GimpsÎncă nu există evaluări

- Research in Economics: Arkadiusz Siero NDocument10 paginiResearch in Economics: Arkadiusz Siero NJózsef PataiÎncă nu există evaluări

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe la EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindEvaluare: 5 din 5 stele5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De la EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Evaluare: 4.5 din 5 stele4.5/5 (13)

- Getting to Yes: How to Negotiate Agreement Without Giving InDe la EverandGetting to Yes: How to Negotiate Agreement Without Giving InEvaluare: 4 din 5 stele4/5 (652)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDe la EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsEvaluare: 5 din 5 stele5/5 (1)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)De la EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageDe la EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageEvaluare: 4.5 din 5 stele4.5/5 (109)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe la EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesÎncă nu există evaluări

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe la EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItEvaluare: 5 din 5 stele5/5 (13)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditDe la EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditEvaluare: 5 din 5 stele5/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)De la EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Evaluare: 4 din 5 stele4/5 (33)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDe la EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsEvaluare: 4 din 5 stele4/5 (7)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!De la EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Evaluare: 4.5 din 5 stele4.5/5 (14)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyDe la EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyEvaluare: 4.5 din 5 stele4.5/5 (37)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDe la EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineÎncă nu există evaluări

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCDe la EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCEvaluare: 5 din 5 stele5/5 (1)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDe la EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetÎncă nu există evaluări

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)De la EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Evaluare: 4.5 din 5 stele4.5/5 (24)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDe la EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsÎncă nu există evaluări

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDe la EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyEvaluare: 5 din 5 stele5/5 (1)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeDe la EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeEvaluare: 4 din 5 stele4/5 (21)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantDe la EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantEvaluare: 4.5 din 5 stele4.5/5 (146)