S-ar putea să vă placă și

- Amex Global Credit Auth Guide ISO Apr2011Document350 paginiAmex Global Credit Auth Guide ISO Apr2011Hafedh Trimeche100% (2)

- Amex Global Credit Auth Guide ISO Apr2011Document350 paginiAmex Global Credit Auth Guide ISO Apr2011Hafedh Trimeche100% (2)

- AcronymsDocument11 paginiAcronymssteelman887160Încă nu există evaluări

- Core Banking ProjectDocument25 paginiCore Banking ProjectKamlesh Negi55% (11)

- Ovum Selecting A Card Management SystemDocument59 paginiOvum Selecting A Card Management SystemTedh ShinÎncă nu există evaluări

- Base 24Document19 paginiBase 24Mohd Atif100% (1)

- Core Banking Solutions FinalDocument6 paginiCore Banking Solutions FinalShashank VarmaÎncă nu există evaluări

- Core Banking EDITINGDocument19 paginiCore Banking EDITINGmuralidancesÎncă nu există evaluări

- Computer-Managed Maintenance Systems: A Step-by-Step Guide to Effective Management of Maintenance, Labor, and InventoryDe la EverandComputer-Managed Maintenance Systems: A Step-by-Step Guide to Effective Management of Maintenance, Labor, and InventoryEvaluare: 3 din 5 stele3/5 (1)

- Bank ServDocument16 paginiBank ServaÎncă nu există evaluări

- Black BookDocument72 paginiBlack BookVikash Maurya0% (1)

- Temenos Payments EbrochureDocument14 paginiTemenos Payments EbrochureralragobiÎncă nu există evaluări

- International Banking For A New Century (2015, Routledge)Document269 paginiInternational Banking For A New Century (2015, Routledge)Tuấn ĐinhÎncă nu există evaluări

- Online Banking System: A Review of Its History, Features and Technical RequirementsDocument23 paginiOnline Banking System: A Review of Its History, Features and Technical RequirementsMuzaFarÎncă nu există evaluări

- Core Banking SolutionDocument30 paginiCore Banking SolutionNidhi ShrivastavaÎncă nu există evaluări

- Core BankingDocument3 paginiCore BankingRekha Raghavan NandakumarÎncă nu există evaluări

- Core Banking SystemDocument7 paginiCore Banking SystemKiruba KaranÎncă nu există evaluări

- Remote Key LoadDocument8 paginiRemote Key LoadHafedh TrimecheÎncă nu există evaluări

- Remote Key LoadDocument8 paginiRemote Key LoadHafedh TrimecheÎncă nu există evaluări

- Remote Key LoadDocument8 paginiRemote Key LoadHafedh TrimecheÎncă nu există evaluări

- Payment System HubsDocument27 paginiPayment System HubsgautamojhaÎncă nu există evaluări

- BPC SmartVista Instant Payments BrochureDocument4 paginiBPC SmartVista Instant Payments BrochureVivekÎncă nu există evaluări

- A Case For A Single Loan Origination System For Core Banking ProductsDocument5 paginiA Case For A Single Loan Origination System For Core Banking ProductsCognizant100% (1)

- Core Banking RajeshDocument8 paginiCore Banking RajeshRajeev SinghÎncă nu există evaluări

- Nazi Monetary PolicyDocument5 paginiNazi Monetary Policyapi-268107541Încă nu există evaluări

- E-Banking Delivery Channels and ApplicationsDocument45 paginiE-Banking Delivery Channels and ApplicationsAditi MangalÎncă nu există evaluări

- New World Order PG 10Document1 paginăNew World Order PG 10Daniel Paes de SouzaÎncă nu există evaluări

- Management Information System (MIS) in Banking SectorDocument20 paginiManagement Information System (MIS) in Banking Sectorsaxena95% (21)

- Union Bank of India's Core Banking SystemDocument36 paginiUnion Bank of India's Core Banking SystemRakesh Prabhakar Shrivastava100% (2)

- CBS ManualDocument495 paginiCBS Manualhimadri_bhattacharje90% (50)

- Huawie - Online Charging System (OCS)Document9 paginiHuawie - Online Charging System (OCS)ghisuddin100% (1)

- Tokenization Best PracticesDocument4 paginiTokenization Best PracticesHafedh TrimecheÎncă nu există evaluări

- Bank Chains Process in SAPDocument12 paginiBank Chains Process in SAPManish BhasinÎncă nu există evaluări

- Management Information System in Banking SoftwareDocument14 paginiManagement Information System in Banking SoftwareTuhin Subhra RoyÎncă nu există evaluări

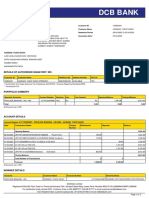

- DCB Bank: Statement of AccountDocument2 paginiDCB Bank: Statement of AccounthasnainÎncă nu există evaluări

- Core Banking SystemsDocument25 paginiCore Banking SystemsSaravananSrvnÎncă nu există evaluări

- Core BankingDocument37 paginiCore Bankingnwani25Încă nu există evaluări

- Use of IS & Latest Trends in Banking: Presented By: Group 1Document43 paginiUse of IS & Latest Trends in Banking: Presented By: Group 1tyrdofitÎncă nu există evaluări

- The National Teachers CollegeDocument7 paginiThe National Teachers CollegeShane BenitezÎncă nu există evaluări

- Scope of IT in Credit Card and Debit Card Transaction System in Indian Banking SectorDocument20 paginiScope of IT in Credit Card and Debit Card Transaction System in Indian Banking SectorSouvik SarkarÎncă nu există evaluări

- What Is Core BankingDocument4 paginiWhat Is Core BankingKennaa BonsaÎncă nu există evaluări

- Centralised Banking Solution - An OverviewDocument4 paginiCentralised Banking Solution - An OverviewAtul RajputÎncă nu există evaluări

- Core BankingDocument4 paginiCore BankingndledpÎncă nu există evaluări

- IT Infrastructure of Basic Bank LimitedDocument7 paginiIT Infrastructure of Basic Bank Limitedashraul islamÎncă nu există evaluări

- Banking MIS Systems & Digital Payment MethodsDocument5 paginiBanking MIS Systems & Digital Payment MethodsOmair Attari QadriÎncă nu există evaluări

- What Is Core Banking Solution ?Document36 paginiWhat Is Core Banking Solution ?Praveen KumarÎncă nu există evaluări

- Management Information System (MIS)Document10 paginiManagement Information System (MIS)Md ImranÎncă nu există evaluări

- Synopsis Mobile Banking AdministrationDocument24 paginiSynopsis Mobile Banking AdministrationRaj BangaloreÎncă nu există evaluări

- Black BookDocument5 paginiBlack BookVikash MauryaÎncă nu există evaluări

- Microsoft Information System in Habib Bank LimitedDocument10 paginiMicrosoft Information System in Habib Bank LimitedUsman BhattiÎncă nu există evaluări

- Ecommerce & Internet Based Compnaies OfferingsDocument16 paginiEcommerce & Internet Based Compnaies OfferingsVishwanath ShettyÎncă nu există evaluări

- Management Information System MIS in Banking Sector PDFDocument20 paginiManagement Information System MIS in Banking Sector PDFJay GudhkaÎncă nu există evaluări

- Retail Banking Products and ServicesDocument8 paginiRetail Banking Products and ServicesankitasankitaÎncă nu există evaluări

- Core Banking SolutionDocument10 paginiCore Banking SolutionHina SinghviÎncă nu există evaluări

- Emergence of Doorstep Banking - Merits and DemeritsDocument11 paginiEmergence of Doorstep Banking - Merits and Demeritsmani100% (1)

- E-Banking HDFC BankDocument24 paginiE-Banking HDFC BankAmit JangirÎncă nu există evaluări

- E-Learning Lesson on Alternate Delivery ChannelsDocument36 paginiE-Learning Lesson on Alternate Delivery ChannelsRISHI KESHÎncă nu există evaluări

- HBL IPG FAQs PDFDocument5 paginiHBL IPG FAQs PDFAbbas HussainÎncă nu există evaluări

- Q&A - Atul KhirwadkarDocument4 paginiQ&A - Atul KhirwadkarPooja GuptaÎncă nu există evaluări

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDocument5 paginiInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingSÎncă nu există evaluări

- NPS Offering Proposal!Document23 paginiNPS Offering Proposal!Simon ShresthaÎncă nu există evaluări

- New Microsoft Word DocumentDocument9 paginiNew Microsoft Word DocumentTejaswi AssuÎncă nu există evaluări

- CommWeb - Payment Client Integration GuideDocument133 paginiCommWeb - Payment Client Integration GuideNiño Francisco AlamoÎncă nu există evaluări

- Core Banking Project On Union BankDocument36 paginiCore Banking Project On Union Bankkushal8120% (1)

- Mobile Banking SysnopsisDocument8 paginiMobile Banking SysnopsisArvind PokhariyaÎncă nu există evaluări

- Core Banking PDFDocument2 paginiCore Banking PDFsrimkbÎncă nu există evaluări

- Pioneering Views: Pushing the Limits of Your C/ETRM - Volume 2De la EverandPioneering Views: Pushing the Limits of Your C/ETRM - Volume 2Încă nu există evaluări

- Pioneering Views: Pushing the Limits of Your C/ETRM – Volume 1De la EverandPioneering Views: Pushing the Limits of Your C/ETRM – Volume 1Încă nu există evaluări

- Net Profit (Review and Analysis of Cohan's Book)De la EverandNet Profit (Review and Analysis of Cohan's Book)Încă nu există evaluări

- Passport Reader SDK User ManualDocument6 paginiPassport Reader SDK User ManualHafedh TrimecheÎncă nu există evaluări

- User Manual: 4-4-2 Enrollment ScannerDocument11 paginiUser Manual: 4-4-2 Enrollment ScannerHafedh TrimecheÎncă nu există evaluări

- Itrack Gold ManualDocument27 paginiItrack Gold ManualHafedh TrimecheÎncă nu există evaluări

- Intelligent Portable Control System: Project PresentationDocument14 paginiIntelligent Portable Control System: Project PresentationHafedh TrimecheÎncă nu există evaluări

- CP864Document10 paginiCP864Hafedh TrimecheÎncă nu există evaluări

- Kelio V14Document36 paginiKelio V14Hafedh TrimecheÎncă nu există evaluări

- Issuer Implementation Quick Reference For 3-D Secure 2.0: Emvco'S 3Ds TestingDocument2 paginiIssuer Implementation Quick Reference For 3-D Secure 2.0: Emvco'S 3Ds TestingHafedh TrimecheÎncă nu există evaluări

- Essentials API - v1.1 - ENDocument24 paginiEssentials API - v1.1 - ENHafedh TrimecheÎncă nu există evaluări

- Develop ActiveX Controls in DelphiDocument6 paginiDevelop ActiveX Controls in DelphiHafedh TrimecheÎncă nu există evaluări

- ISO 8583 Lesson1Document6 paginiISO 8583 Lesson1Hafedh TrimecheÎncă nu există evaluări

- Mightygps Itrack Gold: Gps Tracking For Fleet & SecurityDocument32 paginiMightygps Itrack Gold: Gps Tracking For Fleet & SecurityHafedh TrimecheÎncă nu există evaluări

- Mightygps Itrack Gold: Gps Tracking For Fleet & SecurityDocument32 paginiMightygps Itrack Gold: Gps Tracking For Fleet & SecurityHafedh TrimecheÎncă nu există evaluări

- Activex Delphi Invisible Component LibraryDocument15 paginiActivex Delphi Invisible Component Librarycarlos_saÎncă nu există evaluări

- Develop ActiveX Controls in DelphiDocument6 paginiDevelop ActiveX Controls in DelphiHafedh TrimecheÎncă nu există evaluări

- 3D Secure Test Cardsv1.2.3Document5 pagini3D Secure Test Cardsv1.2.3Hafedh TrimecheÎncă nu există evaluări

- U2500Document4 paginiU2500Hafedh TrimecheÎncă nu există evaluări

- Arabic GlyphsDocument4 paginiArabic GlyphsHafedh TrimecheÎncă nu există evaluări

- Mfvisualcobol Eclipse R4u1 Release NotesDocument28 paginiMfvisualcobol Eclipse R4u1 Release NotesHafedh TrimecheÎncă nu există evaluări

- Merchant GuidelinesDocument11 paginiMerchant GuidelinesHafedh TrimecheÎncă nu există evaluări

- Merchant GuidelinesDocument11 paginiMerchant GuidelinesHafedh TrimecheÎncă nu există evaluări

- Mfvisualcobol Eclipse R4u1 Release NotesDocument28 paginiMfvisualcobol Eclipse R4u1 Release NotesHafedh TrimecheÎncă nu există evaluări

- IATA Aviation Invoice Standard V100Document21 paginiIATA Aviation Invoice Standard V100Hafedh Trimeche100% (1)

- World-Text API SMPP Intergration SpecificationDocument8 paginiWorld-Text API SMPP Intergration SpecificationHafedh TrimecheÎncă nu există evaluări

- Birefps User Guide UpdatedDocument20 paginiBirefps User Guide UpdatedIreneMackay GiraoÎncă nu există evaluări

- Hotel Grand Park Barisal: Receipts & PaymentsDocument2 paginiHotel Grand Park Barisal: Receipts & PaymentsNahid HossainÎncă nu există evaluări

- Gitex - Shopper - 2019 - 1 of 1 PDFDocument1 paginăGitex - Shopper - 2019 - 1 of 1 PDFJishnu CheemenÎncă nu există evaluări

- Importance of Time Value of Money in Financial ManagementDocument16 paginiImportance of Time Value of Money in Financial Managementtanmayjoshi969315Încă nu există evaluări

- BoG On Revision On The Suspension of DividendsDocument2 paginiBoG On Revision On The Suspension of DividendsJoseph Appiah-DolphyneÎncă nu există evaluări

- Cityam 2011-09-12Document44 paginiCityam 2011-09-12City A.M.Încă nu există evaluări

- FMA Sues Akin GumpDocument67 paginiFMA Sues Akin GumpDomainNameWireÎncă nu există evaluări

- MSE Pakistan Limited Statement of Financial PositionDocument1 paginăMSE Pakistan Limited Statement of Financial Positionmirza fawadÎncă nu există evaluări

- Lucid Software Inc.: InvoiceDocument2 paginiLucid Software Inc.: InvoiceHenry M Gutièrrez SÎncă nu există evaluări

- BMO Annual Report 2020Document218 paginiBMO Annual Report 2020Bilal MustafaÎncă nu există evaluări

- Financial InclusionDocument6 paginiFinancial InclusionsignÎncă nu există evaluări

- Manana Mobile International SIM CardDocument9 paginiManana Mobile International SIM CardManana Mobile International SIMÎncă nu există evaluări

- Synopsis On Home LoanDocument9 paginiSynopsis On Home Loanyash jejaniÎncă nu există evaluări

- Chapter-2 Review of Literature 110-143Document34 paginiChapter-2 Review of Literature 110-143city9848835243 cyberÎncă nu există evaluări

- 10.28.2017 MT (Audit of Receivables)Document7 pagini10.28.2017 MT (Audit of Receivables)PatOcampo100% (1)

- Large Numbers in EnglishDocument1 paginăLarge Numbers in EnglishAustin DormanÎncă nu există evaluări

- Orban Co-Operative BankDocument27 paginiOrban Co-Operative BankYaadrahulkumar MoharanaÎncă nu există evaluări

- MCQ - BankingDocument4 paginiMCQ - Bankingbhaskar51178Încă nu există evaluări

- Regional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerDocument2 paginiRegional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerCynthia ChandlerÎncă nu există evaluări

- False Alarm Bjorn LomborgDocument2 paginiFalse Alarm Bjorn LomborgGraham DawsonÎncă nu există evaluări

- ACCT 3331 Exam 2 Review Chapter 18 - Revenue RecognitionDocument14 paginiACCT 3331 Exam 2 Review Chapter 18 - Revenue RecognitionXiaoying XuÎncă nu există evaluări

- Compare Home Loan Schemes of HDFC, ICICI & SBI BankDocument12 paginiCompare Home Loan Schemes of HDFC, ICICI & SBI Bankkunalyadav88Încă nu există evaluări

- BRD transaction reportDocument5 paginiBRD transaction reportDavid GeorgeÎncă nu există evaluări

- What Are The Important Functions of MoneyDocument3 paginiWhat Are The Important Functions of MoneyGanesh KaleÎncă nu există evaluări

- Lending Procedures at Standard BankDocument4 paginiLending Procedures at Standard BankAshraf Uddin AhmedÎncă nu există evaluări

- Dabur Balance SheetDocument30 paginiDabur Balance SheetKrishan TiwariÎncă nu există evaluări