S-ar putea să vă placă și

- The Study of Dividend Policies of Indian CompaniesDocument41 paginiThe Study of Dividend Policies of Indian CompaniesKushaal Chaudhary67% (3)

- Amalgamation of CompaniesDocument8 paginiAmalgamation of CompaniesVikram NaniÎncă nu există evaluări

- "Merger and Consolidation of Icici Ltd. and Icici Bank": A Project Report ONDocument90 pagini"Merger and Consolidation of Icici Ltd. and Icici Bank": A Project Report ONRidhima SharmaÎncă nu există evaluări

- Banking Sector Reforms in IndiaDocument8 paginiBanking Sector Reforms in IndiaJashan Singh GillÎncă nu există evaluări

- MBA Thesis Literature ReviewDocument2 paginiMBA Thesis Literature ReviewHasibul IslamÎncă nu există evaluări

- Impact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorDocument9 paginiImpact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorHarish.PÎncă nu există evaluări

- Work Life BalanceDocument4 paginiWork Life BalancePriya RKÎncă nu există evaluări

- Abstract:: A Study On Mergers and Acquisition in Banking Industry of IndiaDocument4 paginiAbstract:: A Study On Mergers and Acquisition in Banking Industry of IndiaPotlamarri SumanthÎncă nu există evaluări

- Working Capital Management India InfolineDocument83 paginiWorking Capital Management India Infolinearjunmba119624100% (1)

- Comperative Analysis of Products & Services of Axis Bank Wiith Its Competitors Ayushi AgarwalDocument62 paginiComperative Analysis of Products & Services of Axis Bank Wiith Its Competitors Ayushi AgarwalAnonymous CUwjARÎncă nu există evaluări

- 6 - Research MethodologyDocument6 pagini6 - Research Methodologytrushna19Încă nu există evaluări

- Risk and Return Analysis of Mutual FundsDocument3 paginiRisk and Return Analysis of Mutual FundsRoshni MishraÎncă nu există evaluări

- Final Project Report (Pooja) PDFDocument54 paginiFinal Project Report (Pooja) PDFRinkesh K MistryÎncă nu există evaluări

- Central Bank (Final) - 7Document76 paginiCentral Bank (Final) - 7HARSHITA CHAURASIYAÎncă nu există evaluări

- Investment Management - KarvyDocument73 paginiInvestment Management - KarvyAbdul Rahman0% (1)

- Ibc FinalsDocument51 paginiIbc FinalsMALKANI DISHA DEEPAKÎncă nu există evaluări

- Ankit Project Report of EmsopDocument50 paginiAnkit Project Report of EmsopAnkit JainÎncă nu există evaluări

- Indian Automobile Industry PDFDocument28 paginiIndian Automobile Industry PDFAbel JohnÎncă nu există evaluări

- Money Market in India: A Project Report ONDocument35 paginiMoney Market in India: A Project Report ONLovely SharmaÎncă nu există evaluări

- Capital Structure of Banking Companies in IndiaDocument21 paginiCapital Structure of Banking Companies in IndiaAbhishek Soni43% (7)

- M&a of BanksDocument65 paginiM&a of BanksGupte Ruchir0% (1)

- A Study On An Analysis On Mutual Fund of India: Synopsis Submitted To TheDocument10 paginiA Study On An Analysis On Mutual Fund of India: Synopsis Submitted To TheAsit kumar BeheraÎncă nu există evaluări

- A Comparative Study On Services Provided by Different Broking FirmsDocument53 paginiA Comparative Study On Services Provided by Different Broking Firmsbalvendra03Încă nu există evaluări

- Institute of Management, Nirma University: Group Assignment-Reliance Power's IPODocument7 paginiInstitute of Management, Nirma University: Group Assignment-Reliance Power's IPOCJKÎncă nu există evaluări

- Project On Impact of Dividends PolicyDocument45 paginiProject On Impact of Dividends Policyarjunmba119624100% (1)

- A Study On Asset Liability ManagementDocument56 paginiA Study On Asset Liability ManagementMisraÎncă nu există evaluări

- ApmcDocument17 paginiApmcSugandha BishtÎncă nu există evaluări

- Rajkot People's Co-Op - Bank Ltd.Document72 paginiRajkot People's Co-Op - Bank Ltd.Kishan Gokani100% (1)

- Working Capital Management Indian Cements LTDDocument63 paginiWorking Capital Management Indian Cements LTDSri NivasÎncă nu există evaluări

- INVESTOR S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportDocument53 paginiINVESTOR S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportPallavi Pallu100% (1)

- Reforms and Recent Changes in Derivatives MarketsDocument19 paginiReforms and Recent Changes in Derivatives MarketsprathibakbÎncă nu există evaluări

- Article On Financial PlanningDocument16 paginiArticle On Financial PlanningShyam KumarÎncă nu există evaluări

- Foreign Exchange and Risk ManagementDocument43 paginiForeign Exchange and Risk ManagementAmit SinghÎncă nu există evaluări

- Dividend PolicyDocument23 paginiDividend Policyh3llrazr100% (1)

- Observation Commercial Banks PDFDocument52 paginiObservation Commercial Banks PDFyash_dalal123Încă nu există evaluări

- A Report On The Credit Rating Agencies in India 1618161061Document18 paginiA Report On The Credit Rating Agencies in India 1618161061mohit ranaÎncă nu există evaluări

- Mutual Funds Industry in IndiaDocument51 paginiMutual Funds Industry in IndiaSakshi BathlaÎncă nu există evaluări

- BancassuranceDocument62 paginiBancassuranceAkanksha KediaÎncă nu există evaluări

- "Fundamental Analysis of Script Under Pharmaceutical Sector"Document82 pagini"Fundamental Analysis of Script Under Pharmaceutical Sector"sg31Încă nu există evaluări

- Indian Banking Sector ReformsDocument131 paginiIndian Banking Sector Reformsanikettt50% (2)

- Amalgamation of Firms ProjectDocument5 paginiAmalgamation of Firms ProjectkalaswamiÎncă nu există evaluări

- Project Report On Basel IIIDocument8 paginiProject Report On Basel IIICharles DeoraÎncă nu există evaluări

- Kotak Mahindra BankDocument9 paginiKotak Mahindra BankPrajwal KaDwad100% (1)

- Synopsis of Derivative ProjectDocument11 paginiSynopsis of Derivative ProjectSHAIK YASINÎncă nu există evaluări

- A Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byDocument44 paginiA Study On Deposit Mobilization With Reference To Indian Overseas Bank, Velachery byvinoth_17588Încă nu există evaluări

- Industry Profile For Capital MarketDocument31 paginiIndustry Profile For Capital MarketvaibhavchitaleÎncă nu există evaluări

- Role of Credit Rating Agencies in IndiaDocument14 paginiRole of Credit Rating Agencies in IndiaPriyaranjan SinghÎncă nu există evaluări

- Trends in Mergers & Acquisitions in IndiaDocument30 paginiTrends in Mergers & Acquisitions in Indiauma mishraÎncă nu există evaluări

- Merger and AcqisitionDocument38 paginiMerger and AcqisitionPratiksha GaikwadÎncă nu există evaluări

- The Indian Partnership Act, 1932Document17 paginiThe Indian Partnership Act, 1932Engineer100% (1)

- Project ReportDocument53 paginiProject ReportAbhishek MishraÎncă nu există evaluări

- Gamification in Consumer Research A Clear and Concise ReferenceDe la EverandGamification in Consumer Research A Clear and Concise ReferenceÎncă nu există evaluări

- DividendDocument32 paginiDividendprincerattanÎncă nu există evaluări

- Dividend Policy WikipidiaDocument12 paginiDividend Policy WikipidiaAnonymous NSNpGa3T93Încă nu există evaluări

- Dividend PolicyDocument4 paginiDividend PolicyKiran Rajashekaran NairÎncă nu există evaluări

- Relevance N Irrelevance of Dividend PlicyDocument8 paginiRelevance N Irrelevance of Dividend PlicyGagandeep VermaÎncă nu există evaluări

- Financial ManagementDocument8 paginiFinancial ManagementAayush JainÎncă nu există evaluări

- FM Notes - Unit - 5Document7 paginiFM Notes - Unit - 5Shiva JohriÎncă nu există evaluări

- Dividend Policy: Dividend Decision and Valuation of FirmsDocument10 paginiDividend Policy: Dividend Decision and Valuation of FirmsudhavanandÎncă nu există evaluări

- Dividend DecisionDocument25 paginiDividend Decisionva1612315Încă nu există evaluări

- Khemchand Kishinchand NirmalaniDocument2 paginiKhemchand Kishinchand NirmalaniMukesh ManwaniÎncă nu există evaluări

- Brand Impact TitanDocument57 paginiBrand Impact TitanMukesh ManwaniÎncă nu există evaluări

- Fssai NocDocument1 paginăFssai NocMukesh Manwani0% (2)

- Brand Impact Titan FinalDocument57 paginiBrand Impact Titan FinalMukesh ManwaniÎncă nu există evaluări

- Manwani TutorialsDocument3 paginiManwani TutorialsMukesh ManwaniÎncă nu există evaluări

- Comoditiy MarketDocument57 paginiComoditiy MarketMukesh ManwaniÎncă nu există evaluări

- Rahul ResumeDocument1 paginăRahul ResumeMukesh ManwaniÎncă nu există evaluări

- Ulhasnagar Municipal Corporation: E-Pay OnlineDocument1 paginăUlhasnagar Municipal Corporation: E-Pay OnlineMukesh ManwaniÎncă nu există evaluări

- Request For Major Revival of Policy: Life Insured: ProposerDocument5 paginiRequest For Major Revival of Policy: Life Insured: ProposerMukesh ManwaniÎncă nu există evaluări

- Financial Statement and Ratio Analysis of Tata MotorsDocument75 paginiFinancial Statement and Ratio Analysis of Tata MotorsAMIT K SINGH0% (1)

- Financial Statement and Ratio Analysis of Tata MotorsDocument75 paginiFinancial Statement and Ratio Analysis of Tata MotorsAMIT K SINGH0% (1)

- Project On Process CostingDocument11 paginiProject On Process CostingMukesh ManwaniÎncă nu există evaluări

- Job Seeker Registration SlipDocument1 paginăJob Seeker Registration Slipmanwanimuki12100% (1)

- Curriculam Vitae: Career ObjectiveDocument2 paginiCurriculam Vitae: Career ObjectiveMukesh ManwaniÎncă nu există evaluări

- 12 Chapter 2 Review of LiteratureDocument66 pagini12 Chapter 2 Review of LiteratureMukesh ManwaniÎncă nu există evaluări

- Income Tax (Direct Tax) : Submitted By: Harsha Modi Roll No. 25Document1 paginăIncome Tax (Direct Tax) : Submitted By: Harsha Modi Roll No. 25Mukesh ManwaniÎncă nu există evaluări

- Basmati Rice Intl Case - SSRN PDFDocument1 paginăBasmati Rice Intl Case - SSRN PDFMukesh ManwaniÎncă nu există evaluări

- Plants in Cosmetology Cruciferous Vegetables:-: Vitamin CDocument7 paginiPlants in Cosmetology Cruciferous Vegetables:-: Vitamin CMukesh ManwaniÎncă nu există evaluări

- Bom CokDocument1 paginăBom CokMukesh ManwaniÎncă nu există evaluări

- IPO and Right Issue Final ProjectDocument33 paginiIPO and Right Issue Final ProjectMukesh ManwaniÎncă nu există evaluări

- R - Certificate Sir GivenDocument7 paginiR - Certificate Sir GivenMukesh ManwaniÎncă nu există evaluări

- University of MumbaiDocument4 paginiUniversity of MumbaiMukesh ManwaniÎncă nu există evaluări

- The Future of Ready-To-Eat Food in IndiaDocument8 paginiThe Future of Ready-To-Eat Food in IndiaMukesh ManwaniÎncă nu există evaluări

- Introduction To Intellectual PropertyDocument8 paginiIntroduction To Intellectual PropertyMukesh ManwaniÎncă nu există evaluări

- Medicliam InsuranceDocument60 paginiMedicliam InsuranceMukesh ManwaniÎncă nu există evaluări

- Chapter IIDocument26 paginiChapter IIMukesh ManwaniÎncă nu există evaluări

- Bank 12Document66 paginiBank 12Mukesh ManwaniÎncă nu există evaluări

- Foreign Exchange Market in IndiaDocument14 paginiForeign Exchange Market in IndiaMukesh ManwaniÎncă nu există evaluări

- 567Document53 pagini567Mukesh ManwaniÎncă nu există evaluări

- ANNENXUREDocument3 paginiANNENXUREMukesh ManwaniÎncă nu există evaluări

- Coursework: International Financial Management For Business AFE - 7 - IFMDocument11 paginiCoursework: International Financial Management For Business AFE - 7 - IFMPrajit ParajuliÎncă nu există evaluări

- Audit of SHEDocument7 paginiAudit of SHEGille Rosa AbajarÎncă nu există evaluări

- Financial AnalysisDocument8 paginiFinancial Analysisneron hasaniÎncă nu există evaluări

- A Roadmap To Accounting For Share-Based Payment Awards - Third EditionDocument488 paginiA Roadmap To Accounting For Share-Based Payment Awards - Third EditionBeth Bush100% (1)

- NUST Business School: Introduction To Operations Management - OTM 351 Assignment 3Document7 paginiNUST Business School: Introduction To Operations Management - OTM 351 Assignment 3Zainab AftabÎncă nu există evaluări

- RAMID Souhail Final Exam Case StudyDocument38 paginiRAMID Souhail Final Exam Case Studyjean.jacquesÎncă nu există evaluări

- Law Notes by CA Ravi AgarwalDocument58 paginiLaw Notes by CA Ravi AgarwalJoystan MonisÎncă nu există evaluări

- "Financial Health of Reliance Industries Limited": A Project Report OnDocument52 pagini"Financial Health of Reliance Industries Limited": A Project Report Onsagar029Încă nu există evaluări

- Abl Model Work - MemoDocument4 paginiAbl Model Work - MemokartikÎncă nu există evaluări

- Department: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsDocument7 paginiDepartment: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsMhmdÎncă nu există evaluări

- CH 13 QuizDocument8 paginiCH 13 QuizTrentTravers100% (1)

- 6-ch 18Document38 pagini6-ch 18herueuxÎncă nu există evaluări

- JPM - XilinxDocument14 paginiJPM - XilinxAvid HikerÎncă nu există evaluări

- Valuation and Rates of Return: Foundations of Financial ManagementDocument42 paginiValuation and Rates of Return: Foundations of Financial ManagementBlack UnicornÎncă nu există evaluări

- How Securities Are TradedDocument15 paginiHow Securities Are TradedRazafinandrasanaÎncă nu există evaluări

- Far450 Fac450Document8 paginiFar450 Fac450aielÎncă nu există evaluări

- This Study Resource Was: Case: San Miguel in The New MillenniumDocument2 paginiThis Study Resource Was: Case: San Miguel in The New MillenniumBaby BabeÎncă nu există evaluări

- R05 - Financial Accounting and AnalysisDocument3 paginiR05 - Financial Accounting and AnalysisSrinivas NallamalliÎncă nu există evaluări

- Companies Act 28 of 2004Document117 paginiCompanies Act 28 of 2004Newaka DesireÎncă nu există evaluări

- Rieter Consolidated Balance Sheet 2020 enDocument3 paginiRieter Consolidated Balance Sheet 2020 enSachin ChourasiyaÎncă nu există evaluări

- Advanced Financial Management Test 1 May 2024 Solution 1701932012Document15 paginiAdvanced Financial Management Test 1 May 2024 Solution 1701932012shauryagupta20013007Încă nu există evaluări

- Chapter 14 Mas Agamata Answer KeyDocument21 paginiChapter 14 Mas Agamata Answer Keytae ah kimÎncă nu există evaluări

- CH 15 Anchoring On The Financial Statements Simple Forecasting and Simple ValuationDocument25 paginiCH 15 Anchoring On The Financial Statements Simple Forecasting and Simple ValuationRocky HunilaÎncă nu există evaluări

- F3ffa Examreport j13Document4 paginiF3ffa Examreport j13onyeonwuÎncă nu există evaluări

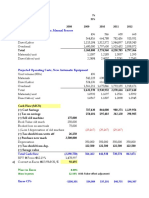

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Document4 paginiProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyÎncă nu există evaluări

- Company Analysis Report On DR - REDDY'SDocument49 paginiCompany Analysis Report On DR - REDDY'Ssirisha100% (3)

- FM RL 1.1.5Document14 paginiFM RL 1.1.5anandakumarÎncă nu există evaluări

- DPC9 1208180022450694 01022021210649Document2 paginiDPC9 1208180022450694 0102202121064928squashÎncă nu există evaluări

- Convertible Note Term SheetDocument2 paginiConvertible Note Term SheetVictorÎncă nu există evaluări

- V F Corporation NYSE VFC FinancialsDocument9 paginiV F Corporation NYSE VFC FinancialsAmalia MegaÎncă nu există evaluări