S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Pakistan AnnexuresDocument8 paginiPakistan AnnexuresUmair UddinÎncă nu există evaluări

- Cement NotationsDocument2 paginiCement NotationsGiequatÎncă nu există evaluări

- Emission Reduction CalculationsDocument51 paginiEmission Reduction CalculationsUmair UddinÎncă nu există evaluări

- TheCementPlantOperations B PDFDocument32 paginiTheCementPlantOperations B PDFUmair UddinÎncă nu există evaluări

- Du Annual Report English LR 160314 12.00Document44 paginiDu Annual Report English LR 160314 12.00Umair UddinÎncă nu există evaluări

- Problem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Document20 paginiProblem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Umair UddinÎncă nu există evaluări

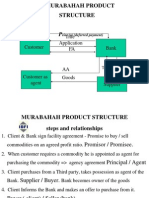

- Murabahah Product Structure: Title Application FADocument26 paginiMurabahah Product Structure: Title Application FAUmair UddinÎncă nu există evaluări

- Lab5 SPSS ChiSquareDocument14 paginiLab5 SPSS ChiSquareUmair UddinÎncă nu există evaluări

- Decision Making and Relevant Information - ch11Document49 paginiDecision Making and Relevant Information - ch11Umair UddinÎncă nu există evaluări

- Problem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Document20 paginiProblem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Umair UddinÎncă nu există evaluări

- Tax ExpenditureDocument3 paginiTax ExpenditureUmair UddinÎncă nu există evaluări

- Chi Square Test For IndependeceDocument40 paginiChi Square Test For IndependeceNaman Bansal100% (1)

- Al-Faysal Bank LTDDocument44 paginiAl-Faysal Bank LTDqalander abbasÎncă nu există evaluări

- Pub Blic D Debt: CH Apter 9Document21 paginiPub Blic D Debt: CH Apter 9Umair UddinÎncă nu există evaluări

- Pakistan, The United States and The IMF: Great Game or A Curious Case of Dutch Disease Without The Oil?Document23 paginiPakistan, The United States and The IMF: Great Game or A Curious Case of Dutch Disease Without The Oil?Umair UddinÎncă nu există evaluări

- InterviewsDocument13 paginiInterviewsUmair UddinÎncă nu există evaluări

- Schiffman CB10 PPT 05Document55 paginiSchiffman CB10 PPT 05Syed Wahaj100% (1)

- How To Develop Presentation SkillsDocument29 paginiHow To Develop Presentation Skillsppinku0003100% (1)

- Chemical Resistance of PlasticsDocument4 paginiChemical Resistance of PlasticsUmair UddinÎncă nu există evaluări

- IcIDocument39 paginiIcIUmair UddinÎncă nu există evaluări

- IcIDocument39 paginiIcIUmair UddinÎncă nu există evaluări

- Kinds of ContractsDocument10 paginiKinds of ContractsUmair UddinÎncă nu există evaluări

- Discharge of ContractDocument14 paginiDischarge of ContractherhamÎncă nu există evaluări

- Chapter 1 - HRM - Introduction To HRM 120609Document64 paginiChapter 1 - HRM - Introduction To HRM 120609Umair UddinÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Basic Concepts in Criminal LawDocument39 paginiBasic Concepts in Criminal LawPrecylyn Garcia Buñao100% (1)

- 70.tolentino Vs COMELEC Case DigestDocument2 pagini70.tolentino Vs COMELEC Case DigestA M I R AÎncă nu există evaluări

- Bill of Rights ScrapbookDocument8 paginiBill of Rights ScrapbooksambaÎncă nu există evaluări

- Labor Law Lecture Bar Ops 2017 (Arranged)Document18 paginiLabor Law Lecture Bar Ops 2017 (Arranged)Eleasar Banasen Pido100% (1)

- M8 - Abinales and Amoroso - State and Society in The Philippines - All Politics Is Local PDFDocument14 paginiM8 - Abinales and Amoroso - State and Society in The Philippines - All Politics Is Local PDFolaf faloÎncă nu există evaluări

- German Challenges To Post-War Settlements (3.2.4) - IB History - TutorChaseDocument10 paginiGerman Challenges To Post-War Settlements (3.2.4) - IB History - TutorChaseMartina ColeÎncă nu există evaluări

- Review On Aw 1,2,28,54-97 & 105-110Document11 paginiReview On Aw 1,2,28,54-97 & 105-110darwin bangaoilÎncă nu există evaluări

- Simple Notes of CPCDocument23 paginiSimple Notes of CPCEeshank Gaur100% (13)

- Letter To City of Miami Mayor and Commissioners - Sept. 12, 2018Document29 paginiLetter To City of Miami Mayor and Commissioners - Sept. 12, 2018al_crespoÎncă nu există evaluări

- John Giduck List of False Military Claims - FINALDocument12 paginiJohn Giduck List of False Military Claims - FINALma91c1anÎncă nu există evaluări

- The Legum Wire: Connecting CornersDocument7 paginiThe Legum Wire: Connecting CornersAditya MaheshwariÎncă nu există evaluări

- Napocor Vs Agro DigestDocument6 paginiNapocor Vs Agro DigestJan Jason Guerrero LumanagÎncă nu există evaluări

- People Vs LamahangDocument2 paginiPeople Vs LamahangbmlÎncă nu există evaluări

- 01B - Fetalino vs. Commission On ElectionsDocument1 pagină01B - Fetalino vs. Commission On ElectionsRenard EnrileÎncă nu există evaluări

- History of Sri LankaDocument20 paginiHistory of Sri LankaShenu MihilshiÎncă nu există evaluări

- EXAMPLE - Affidavitt of Fact and NoticeDocument2 paginiEXAMPLE - Affidavitt of Fact and Noticemystagog_inc86% (7)

- Notice of CessationDocument3 paginiNotice of CessationAure CarilloÎncă nu există evaluări

- Public Officer and Election Laws Related CasesDocument225 paginiPublic Officer and Election Laws Related CasesLei Bataller BautistaÎncă nu există evaluări

- Cpa f1.2 - Introduction To Law - Study ManualDocument140 paginiCpa f1.2 - Introduction To Law - Study Manualcamli kamlicius100% (1)

- Predicaments of DemocracyDocument3 paginiPredicaments of DemocracyVivek KaushikÎncă nu există evaluări

- Anlud Metal Recycling Corporation Vs AngDocument4 paginiAnlud Metal Recycling Corporation Vs AngHaze Q.Încă nu există evaluări

- Michigan Supreme Court Opinion On Child Support and PovertyDocument80 paginiMichigan Supreme Court Opinion On Child Support and PovertyBeverly TranÎncă nu există evaluări

- Alphonso Bax and Alice Corrine Bax, Deceased, and Alphonso L. Bax, Administrator v. Commissioner of Internal Revenue, 13 F.3d 54, 2d Cir. (1993)Document6 paginiAlphonso Bax and Alice Corrine Bax, Deceased, and Alphonso L. Bax, Administrator v. Commissioner of Internal Revenue, 13 F.3d 54, 2d Cir. (1993)Scribd Government DocsÎncă nu există evaluări

- Kenya LootersDocument667 paginiKenya Lootersjimrosenberg100% (3)

- Salient Features of Adr ActDocument8 paginiSalient Features of Adr ActLhai Tabajonda-Mallillin0% (1)

- Proposed Rule: Mergers, Conversion From Credit Union Charter, and Account Insurance Termination Extension of Comment PeriodDocument1 paginăProposed Rule: Mergers, Conversion From Credit Union Charter, and Account Insurance Termination Extension of Comment PeriodJustia.comÎncă nu există evaluări

- Responding To Harvey: It's All About Organizing: Benjamin ShepardDocument11 paginiResponding To Harvey: It's All About Organizing: Benjamin ShepardMarc Allen HerbstÎncă nu există evaluări

- Obama DoctrineDocument25 paginiObama DoctrineDaniela R. EduardoÎncă nu există evaluări

- Permanent Lok Adalat (Other Terms and Conditions of Appointment of Chairman and Other Persons) Rules, 2003Document4 paginiPermanent Lok Adalat (Other Terms and Conditions of Appointment of Chairman and Other Persons) Rules, 2003Latest Laws Team100% (1)

- Ratio DecidendiDocument24 paginiRatio DecidendiJenny Habas100% (1)