S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Internship ReportDocument27 paginiInternship ReportSrinivas PrabhuÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- MRF QTR 1 14 15 PDFDocument1 paginăMRF QTR 1 14 15 PDFdanielxx747Încă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Accounting For Religious Organization OrginalDocument20 paginiAccounting For Religious Organization Orginaltsedekselashi90Încă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Income StatementDocument13 paginiIncome StatementElleighn SaezÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Kunci Jawaban Soal Review InterDocument5 paginiKunci Jawaban Soal Review InterWinarto SudrajadÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Woodworking Business Plan ExampleDocument35 paginiWoodworking Business Plan ExampleSleshi Mekonnen100% (3)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Final Account With AnswersDocument23 paginiFinal Account With Answerskunjap0% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- (In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanDocument9 pagini(In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanAnamika NandiÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Relevant CostingDocument58 paginiRelevant CostingAlexanderJacobVielMartinezÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- NGO Audited Documents Balance Sheet and Profit and Loss A/cDocument27 paginiNGO Audited Documents Balance Sheet and Profit and Loss A/cMitesh Khatri100% (5)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- This Project Is Done by Karthik SP Based On Cash Flow Analysis For Union Bank of IndiaDocument105 paginiThis Project Is Done by Karthik SP Based On Cash Flow Analysis For Union Bank of IndiaKarthik Sp100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Travel Policy - India W IDC PDFDocument30 paginiTravel Policy - India W IDC PDFmahakagrawal3Încă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- P3-5a, p3-2b William 6081901032 FDocument13 paginiP3-5a, p3-2b William 6081901032 FWilliam Wihardja0% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- 3109 - Taxation of Non-Individual TaxpayersDocument9 pagini3109 - Taxation of Non-Individual TaxpayersMae Angiela TansecoÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- ............. Mgt602 Solved Mcqs Almost 700 Mcqs by VustudentsDocument135 pagini............. Mgt602 Solved Mcqs Almost 700 Mcqs by Vustudentsamirqasmi100% (4)

- CAPEX Planning Tutorial v2Document10 paginiCAPEX Planning Tutorial v2PrashantRanjan2010Încă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Ukay-Ukaya Ko Bi Feasibility StudyDocument68 paginiUkay-Ukaya Ko Bi Feasibility StudyPia Suril100% (3)

- Feasibility StudyDocument16 paginiFeasibility Studyrakesh varmaÎncă nu există evaluări

- NA Payroll TrainingDocument49 paginiNA Payroll TraininggrspavaniÎncă nu există evaluări

- Balance SheetDocument90 paginiBalance SheetRashedÎncă nu există evaluări

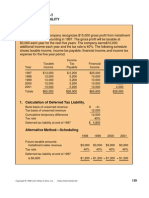

- Deferred Tax IllustrationDocument8 paginiDeferred Tax IllustrationFaseeh IqbalÎncă nu există evaluări

- ASP KIT - NewDocument16 paginiASP KIT - NewMa Victoria Dumapay Teleb100% (1)

- Financial Accounting SyllabusDocument2 paginiFinancial Accounting Syllabusp.sankaranarayananÎncă nu există evaluări

- Assurance IP 1 Week 1Document1 paginăAssurance IP 1 Week 1rui zhangÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Oracle Fusion FIN Using Allocations GLDocument30 paginiOracle Fusion FIN Using Allocations GLSrinivasa Rao AsuruÎncă nu există evaluări

- AUDITING PROB Activity 2Document4 paginiAUDITING PROB Activity 2Joody CatacutanÎncă nu există evaluări

- Presentation 2 - Audit of Intangible AssetsDocument27 paginiPresentation 2 - Audit of Intangible AssetsPaula De RuedaÎncă nu există evaluări

- Test Paper - 3 CA FinalDocument3 paginiTest Paper - 3 CA FinalyeidaindschemeÎncă nu există evaluări

- Ratio Analysis 1Document31 paginiRatio Analysis 1Avinash SahuÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Capital Gains Tax NEWDocument109 paginiCapital Gains Tax NEWRishi CharanÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)