S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

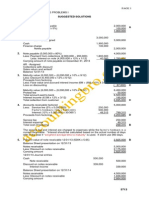

- Installment SalesDocument3 paginiInstallment SalesEpal Ako67% (3)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- 5747Document3 pagini5747cutieaikoÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- HobDocument5 paginiHobcutieaikoÎncă nu există evaluări

- 5765Document4 pagini5765cutieaikoÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- HOB SolutionsDocument5 paginiHOB SolutionscutieaikoÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- 5764Document4 pagini5764cutieaikoÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- 5715 5716Document2 pagini5715 5716cutieaikoÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- HOB SolutionsDocument5 paginiHOB SolutionscutieaikoÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Suggested Solutions Share Based Payment Compensation 5745 1Document1 paginăSuggested Solutions Share Based Payment Compensation 5745 1cutieaikoÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Formation & OperationDocument4 paginiFormation & OperationcutieaikoÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- HobDocument5 paginiHobcutieaikoÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Audit Evidence and Audit ProgramsDocument9 paginiAudit Evidence and Audit ProgramscutieaikoÎncă nu există evaluări

- Tax 2Document11 paginiTax 2cutieaikoÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Its Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andDocument2 paginiIts Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andcutieaikoÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- HOB SolutionsDocument5 paginiHOB SolutionscutieaikoÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- SqueezedDocument1 paginăSqueezedcutieaikoÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Suggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"Document2 paginiSuggested Solutions Receivable Financing 1. A: "Weighted Average Time To Maturity"cutieaikoÎncă nu există evaluări

- Not Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivableDocument1 paginăNot Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivablecutieaikoÎncă nu există evaluări

- Suggested SolutionsDocument1 paginăSuggested SolutionscutieaikoÎncă nu există evaluări

- Suggested SolutionsDocument1 paginăSuggested SolutionscutieaikoÎncă nu există evaluări

- AttDocument8 paginiAttcutieaikoÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Business Combination and Date of AcquisitionDocument3 paginiBusiness Combination and Date of AcquisitioncutieaikoÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Suggested Solutions 5740 Deferred Income Tax 1Document1 paginăSuggested Solutions 5740 Deferred Income Tax 1cutieaikoÎncă nu există evaluări

- Suggested SolutionsDocument1 paginăSuggested SolutionscutieaikoÎncă nu există evaluări

- Avocado Production in The PhilippinesDocument20 paginiAvocado Production in The Philippinescutieaiko100% (1)

- Tax 2Document11 paginiTax 2cutieaikoÎncă nu există evaluări

- TaxDocument3 paginiTaxCess MelendezÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Auditing Theory Quiz Final PrintDocument6 paginiAuditing Theory Quiz Final Printnda0403Încă nu există evaluări

- 01 Glossary of Terms December 2002Document20 pagini01 Glossary of Terms December 2002Tracy KayeÎncă nu există evaluări

- Banking Law PresentationDocument15 paginiBanking Law PresentationSahana BalarajÎncă nu există evaluări

- Efu Life Assurance LTD.: Total 20,480 Provisional Sales Tax 0.0 0Document1 paginăEfu Life Assurance LTD.: Total 20,480 Provisional Sales Tax 0.0 0ASAD RAHMANÎncă nu există evaluări

- Culture and Sustainable Development - Final Proceedings - University of Arts Belgrade 2014Document364 paginiCulture and Sustainable Development - Final Proceedings - University of Arts Belgrade 2014Ljiljana Rogač MijatovićÎncă nu există evaluări

- Swot ShanDocument4 paginiSwot Shanq_burhan_a33% (3)

- Category Management GTDocument2 paginiCategory Management GTArun MaithaniÎncă nu există evaluări

- Eman Practice WordDocument6 paginiEman Practice WordArlene Abriza PunioÎncă nu există evaluări

- Uh Econ 607 NotesDocument255 paginiUh Econ 607 NotesDamla HacıÎncă nu există evaluări

- Globalization Is Changing: Jude Brian Mordeno BSTM 401ADocument4 paginiGlobalization Is Changing: Jude Brian Mordeno BSTM 401AAnon MousÎncă nu există evaluări

- Economic RRL Version 2.1Document8 paginiEconomic RRL Version 2.1Adrian Kenneth G. NervidaÎncă nu există evaluări

- Sınav 1Document27 paginiSınav 1denememdirbuÎncă nu există evaluări

- Marine Insurance QuestionnaireDocument4 paginiMarine Insurance QuestionnaireSuraj Theruvath100% (5)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Nomination Remuneration PolicyDocument6 paginiNomination Remuneration PolicyAbesh DebÎncă nu există evaluări

- GO Ms 17 2007Document4 paginiGO Ms 17 2007drlokeshreddy100% (1)

- Roof India Exhibition 2019Document6 paginiRoof India Exhibition 2019Jyotsna PandeyÎncă nu există evaluări

- Brief Industrial Profile Virudhunagar District: MSME-Development Institute, ChennaiDocument21 paginiBrief Industrial Profile Virudhunagar District: MSME-Development Institute, Chennai63070Încă nu există evaluări

- Ca Final DT (New) Chapterwise Abc & Marks Analysis - Ca Ravi AgarwalDocument5 paginiCa Final DT (New) Chapterwise Abc & Marks Analysis - Ca Ravi AgarwalROHIT JAIN100% (1)

- Globalization L7Document42 paginiGlobalization L7Cherrie Chu SiuwanÎncă nu există evaluări

- PC Depot (Accounting)Document4 paginiPC Depot (Accounting)Ange Buenaventura Salazar100% (2)

- Project Report of Research Methodology OnDocument44 paginiProject Report of Research Methodology OnMohit Sugandh100% (1)

- ProcessingDocument49 paginiProcessingFatih Aydin100% (1)

- Types of Raw MaterialsDocument27 paginiTypes of Raw MaterialsAppleCorpuzDelaRosaÎncă nu există evaluări

- Project DetailsDocument4 paginiProject DetailsSKSAIDINESHÎncă nu există evaluări

- OperatingReview2014 EngDocument37 paginiOperatingReview2014 EngBinduPrakashBhattÎncă nu există evaluări

- AwbDocument1 paginăAwbAnonymous RCM8aHgrPÎncă nu există evaluări

- Ac Far Quiz8Document4 paginiAc Far Quiz8Kristine Joy CutillarÎncă nu există evaluări

- How Are Wages Determined by The Marginal Productivity of LaborDocument4 paginiHow Are Wages Determined by The Marginal Productivity of LaborsukandeÎncă nu există evaluări

- (개정) 2021년 - 영어 - NE능률 (김성곤) - 2과 - 적중예상문제 1회 실전 - OKDocument11 pagini(개정) 2021년 - 영어 - NE능률 (김성곤) - 2과 - 적중예상문제 1회 실전 - OK김태석Încă nu există evaluări

- Behind Maori NationalismDocument8 paginiBehind Maori NationalismTricksy Mix100% (1)

- Daily Renewables WatchDocument2 paginiDaily Renewables WatchunitedmanticoreÎncă nu există evaluări

- Employment Productivity and Wages in The Philippine Labor Market An Analysis of Trends and PoliciesDocument93 paginiEmployment Productivity and Wages in The Philippine Labor Market An Analysis of Trends and PoliciesNabiel DarindigonÎncă nu există evaluări

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDe la EverandReady, Set, Growth hack:: A beginners guide to growth hacking successEvaluare: 4.5 din 5 stele4.5/5 (93)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDe la Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNEvaluare: 4.5 din 5 stele4.5/5 (3)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDe la EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingEvaluare: 4.5 din 5 stele4.5/5 (17)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)

- Value: The Four Cornerstones of Corporate FinanceDe la EverandValue: The Four Cornerstones of Corporate FinanceEvaluare: 4.5 din 5 stele4.5/5 (18)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDe la EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursEvaluare: 4.5 din 5 stele4.5/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)