S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Analysis and Estimation of The US Oil ProductionDocument1 paginăAnalysis and Estimation of The US Oil ProductionEduardo PetazzeÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- India - Index of Industrial ProductionDocument1 paginăIndia - Index of Industrial ProductionEduardo PetazzeÎncă nu există evaluări

- Germany - Renewable Energies ActDocument1 paginăGermany - Renewable Energies ActEduardo PetazzeÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

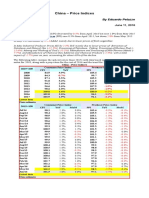

- China - Price IndicesDocument1 paginăChina - Price IndicesEduardo PetazzeÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

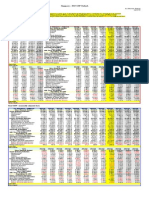

- Highlights, Wednesday June 8, 2016Document1 paginăHighlights, Wednesday June 8, 2016Eduardo PetazzeÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Turkey - Gross Domestic Product, Outlook 2016-2017Document1 paginăTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- U.S. New Home Sales and House Price IndexDocument1 paginăU.S. New Home Sales and House Price IndexEduardo PetazzeÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Reflections On The Greek Crisis and The Level of EmploymentDocument1 paginăReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

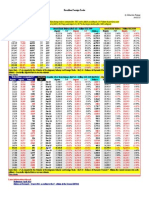

- WTI Spot PriceDocument4 paginiWTI Spot PriceEduardo Petazze100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- U.S. Employment Situation - 2015 / 2017 OutlookDocument1 paginăU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Document1 paginăCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Brazilian Foreign TradeDocument1 paginăBrazilian Foreign TradeEduardo PetazzeÎncă nu există evaluări

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocument1 paginăChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- India 2015 GDPDocument1 paginăIndia 2015 GDPEduardo PetazzeÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocument1 paginăUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Singapore - 2015 GDP OutlookDocument1 paginăSingapore - 2015 GDP OutlookEduardo PetazzeÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- South Africa - 2015 GDP OutlookDocument1 paginăSouth Africa - 2015 GDP OutlookEduardo PetazzeÎncă nu există evaluări

- China - Power GenerationDocument1 paginăChina - Power GenerationEduardo PetazzeÎncă nu există evaluări

- US Mining Production IndexDocument1 paginăUS Mining Production IndexEduardo PetazzeÎncă nu există evaluări

- México, PBI 2015Document1 paginăMéxico, PBI 2015Eduardo PetazzeÎncă nu există evaluări

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocument1 paginăEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

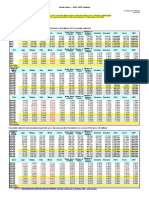

- Chile, Monthly Index of Economic Activity, IMACECDocument2 paginiChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeÎncă nu există evaluări

- Highlights in Scribd, Updated in April 2015Document1 paginăHighlights in Scribd, Updated in April 2015Eduardo PetazzeÎncă nu există evaluări

- U.S. Federal Open Market Committee: Federal Funds RateDocument1 paginăU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzeÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Mainland China - Interest Rates and InflationDocument1 paginăMainland China - Interest Rates and InflationEduardo PetazzeÎncă nu există evaluări

- US - Personal Income and Outlays - 2015-2016 OutlookDocument1 paginăUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeÎncă nu există evaluări

- Japan, Population and Labour Force - 2015-2017 OutlookDocument1 paginăJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeÎncă nu există evaluări

- United States - Gross Domestic Product by IndustryDocument1 paginăUnited States - Gross Domestic Product by IndustryEduardo PetazzeÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- South Korea, Monthly Industrial StatisticsDocument1 paginăSouth Korea, Monthly Industrial StatisticsEduardo PetazzeÎncă nu există evaluări

- Japan, Indices of Industrial ProductionDocument1 paginăJapan, Indices of Industrial ProductionEduardo PetazzeÎncă nu există evaluări

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAishwarya SenthilÎncă nu există evaluări

- LK BMHS 30 September 2021Document71 paginiLK BMHS 30 September 2021samudraÎncă nu există evaluări

- FundamentalsOfFinancialManagement Chapter8Document17 paginiFundamentalsOfFinancialManagement Chapter8Adoree RamosÎncă nu există evaluări

- Families With Children 2021Document2 paginiFamilies With Children 2021Finn KevinÎncă nu există evaluări

- Lesson 1.1 Simple Interest Visual AidDocument13 paginiLesson 1.1 Simple Interest Visual AidJerald SamsonÎncă nu există evaluări

- Sample Loan Mod Package W ProposalDocument12 paginiSample Loan Mod Package W ProposalJules Caesar VallezÎncă nu există evaluări

- Tax Invoice: Dtwelve Spaces Pvt. LTDDocument3 paginiTax Invoice: Dtwelve Spaces Pvt. LTDChanchal MadankarÎncă nu există evaluări

- Virtual Assets Red Flag IndicatorsDocument24 paginiVirtual Assets Red Flag IndicatorsSubrahmanyam SiriÎncă nu există evaluări

- Top 50 RulesDocument53 paginiTop 50 RulesShaji HakeemÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Average Daily FloatDocument4 paginiAverage Daily FloatAn DoÎncă nu există evaluări

- Financial Reporting Standards Council (FRSC)Document43 paginiFinancial Reporting Standards Council (FRSC)Pam G.Încă nu există evaluări

- 2014 12 Mercer Risk Premia Investing From The Traditional To Alternatives PDFDocument20 pagini2014 12 Mercer Risk Premia Investing From The Traditional To Alternatives PDFArnaud AmatoÎncă nu există evaluări

- Money, Banking, and Monetary Policy: ObjectivesDocument9 paginiMoney, Banking, and Monetary Policy: ObjectivesKamalpreetÎncă nu există evaluări

- Relative Purchasing Power Parity Relative Purchasing Power ParityDocument2 paginiRelative Purchasing Power Parity Relative Purchasing Power ParityMohammad HammoudehÎncă nu există evaluări

- Introduction To Private and Public BankDocument17 paginiIntroduction To Private and Public BankAbhishek JohariÎncă nu există evaluări

- Inner Circle Trader Ict Forex Ict NotesDocument110 paginiInner Circle Trader Ict Forex Ict NotesjcferreiraÎncă nu există evaluări

- Handout 018Document1 paginăHandout 018Caryl May Esparrago MiraÎncă nu există evaluări

- Business Plan For Startup BusinessDocument25 paginiBusiness Plan For Startup BusinessLigia PopescuÎncă nu există evaluări

- The SPACE Matrix AnalysisDocument6 paginiThe SPACE Matrix AnalysisMarwan Al-Asbahi100% (1)

- Thank You For Paying On-Time: Basic Housing Solutions, IncDocument1 paginăThank You For Paying On-Time: Basic Housing Solutions, IncMarcelo AnfoneÎncă nu există evaluări

- CPA Adeel ResumeDocument2 paginiCPA Adeel ResumeMH ULTRAÎncă nu există evaluări

- Moody's On US Bank RisksDocument13 paginiMoody's On US Bank RisksTim MooreÎncă nu există evaluări

- Compensation Options For Early Contributors Wolfpackbot: OriginalDocument1 paginăCompensation Options For Early Contributors Wolfpackbot: OriginalMohamed FathiÎncă nu există evaluări

- Chapter 13 SolutionsDocument26 paginiChapter 13 SolutionsMathew Idanan0% (1)

- Risk Management Solution Manual Chapter 01Document7 paginiRisk Management Solution Manual Chapter 01DanielLam100% (5)

- Robert Mundel & Mercus Fleming Model (IS LM BP Model) PDFDocument11 paginiRobert Mundel & Mercus Fleming Model (IS LM BP Model) PDFSukumar SarkarÎncă nu există evaluări

- F.Lundberg - The Rich and The Super-Rich (1968)Document632 paginiF.Lundberg - The Rich and The Super-Rich (1968)Bob100% (1)

- Quiz 8 - BTX 113Document3 paginiQuiz 8 - BTX 113Rae Vincent Revilla100% (1)

- Lecture 12 Equity Analysis and ValuationDocument31 paginiLecture 12 Equity Analysis and ValuationKhushbooÎncă nu există evaluări

- DeliveryHeroSE Annual Financial Statement FinalDocument108 paginiDeliveryHeroSE Annual Financial Statement FinalimranÎncă nu există evaluări

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationDe la EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationEvaluare: 4 din 5 stele4/5 (11)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDe la EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassÎncă nu există evaluări

- The New Elite: Inside the Minds of the Truly WealthyDe la EverandThe New Elite: Inside the Minds of the Truly WealthyEvaluare: 4 din 5 stele4/5 (10)