S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- KPMGDocument29 paginiKPMGLauren ObrienÎncă nu există evaluări

- Acu 08108 - Assignment International FinanceDocument3 paginiAcu 08108 - Assignment International FinancecalipharamadhaniÎncă nu există evaluări

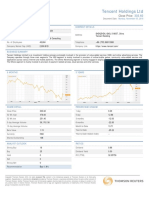

- Tencent Holdings LTD: Close PriceDocument2 paginiTencent Holdings LTD: Close PricetrungÎncă nu există evaluări

- Solution Aassignments CH 14Document9 paginiSolution Aassignments CH 14RuturajPatilÎncă nu există evaluări

- Chapter 1 FR IntroductionDocument12 paginiChapter 1 FR Introductionvijas ahamedÎncă nu există evaluări

- Calculate Your Federal TaxesDocument4 paginiCalculate Your Federal Taxesapi-718873824Încă nu există evaluări

- TUTORIAL 9 BlawDocument4 paginiTUTORIAL 9 BlawTrang Dư Thị HiềnÎncă nu există evaluări

- Assertions in The Audit of Financial StatementsDocument3 paginiAssertions in The Audit of Financial StatementsBirei GonzalesÎncă nu există evaluări

- GreeksDocument19 paginiGreeksTafadzwa bee MasumbukoÎncă nu există evaluări

- Analysis of Financial StatementsDocument36 paginiAnalysis of Financial StatementsvasuuumÎncă nu există evaluări

- Common Stock ValuationDocument34 paginiCommon Stock ValuationSatria DeniÎncă nu există evaluări

- What Is The Difference Between Vertical Analysis and Horizontal AnalysisDocument2 paginiWhat Is The Difference Between Vertical Analysis and Horizontal AnalysisfranklinÎncă nu există evaluări

- Ch. 3 Financial Statement AnalysisDocument3 paginiCh. 3 Financial Statement AnalysishaleeÎncă nu există evaluări

- Excel Workbook For In-Class Demonstrations and Self-Practice With Solutions - Chapter 9 Part 2 of 8Document4 paginiExcel Workbook For In-Class Demonstrations and Self-Practice With Solutions - Chapter 9 Part 2 of 8Dante CardonaÎncă nu există evaluări

- Bidvest Bank Sable InternationalDocument4 paginiBidvest Bank Sable InternationalBD MahamudÎncă nu există evaluări

- 6 Weeks Investment Banking Training (11 October 2010)Document19 pagini6 Weeks Investment Banking Training (11 October 2010)triptinavaniÎncă nu există evaluări

- 1 - Cfa-2018-Quest-Bank-R21-Financial-Statement-Analysis-An-Introduction-Q-BankDocument7 pagini1 - Cfa-2018-Quest-Bank-R21-Financial-Statement-Analysis-An-Introduction-Q-BankQuyen Thanh NguyenÎncă nu există evaluări

- Cost Accounting QuestionsDocument5 paginiCost Accounting QuestionsAdilHayatÎncă nu există evaluări

- Bab 2 MateriDocument4 paginiBab 2 MateriAndikaÎncă nu există evaluări

- CAPITAL BUDGETING AssignmentDocument4 paginiCAPITAL BUDGETING Assignmentqurban baloch100% (1)

- Vatsal Changoiwala - Bajaj Auto Ltd.Document12 paginiVatsal Changoiwala - Bajaj Auto Ltd.Vatsal ChangoiwalaÎncă nu există evaluări

- WRD 27e Se PPT Ch01 AdaDocument23 paginiWRD 27e Se PPT Ch01 AdaNovrissa DianiÎncă nu există evaluări

- Valuation 101: How To Do A Discounted Cashflow AnalysisDocument3 paginiValuation 101: How To Do A Discounted Cashflow AnalysisdevÎncă nu există evaluări

- Cipla Balance SheetDocument2 paginiCipla Balance SheetNEHA LAL100% (1)

- 2022 Endeavor Impact Report Spreads 1Document39 pagini2022 Endeavor Impact Report Spreads 1Abrar RattuÎncă nu există evaluări

- Invesrment in Debt InstrumentsDocument2 paginiInvesrment in Debt InstrumentsElla MontefalcoÎncă nu există evaluări

- Role Play 20204 - Fin242Document2 paginiRole Play 20204 - Fin242Muhd Arreif Mohd AzzarainÎncă nu există evaluări

- 8401Document15 pagini8401Naeem AnwarÎncă nu există evaluări

- Learn To Communicate With Accounting Staff: Cle - Creative Learning ExerciseDocument108 paginiLearn To Communicate With Accounting Staff: Cle - Creative Learning ExercisepasinÎncă nu există evaluări

- Cantabil PresentationDocument37 paginiCantabil PresentationRajiv HandaÎncă nu există evaluări