S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Nebosh: Management of Health and Safety Unit Ig1Document5 paginiNebosh: Management of Health and Safety Unit Ig1shaynad binsharaf100% (3)

- 6 - Lecture - The 8 Es in AuditingDocument11 pagini6 - Lecture - The 8 Es in AuditingKris MendezÎncă nu există evaluări

- AIC 4.3 Key QuotationsDocument10 paginiAIC 4.3 Key QuotationsJasmine SahotaÎncă nu există evaluări

- The Five Paragraph Essay: Week Four, Part TwoDocument29 paginiThe Five Paragraph Essay: Week Four, Part TwoFarhang Abdalla IsmaelÎncă nu există evaluări

- The 19 Century Philippines: Changes in Its Designated AspectsDocument4 paginiThe 19 Century Philippines: Changes in Its Designated AspectsMarvic AboÎncă nu există evaluări

- Application of The Ethical Matrix in Evaluation of The Question of Downer Cattle TransportDocument23 paginiApplication of The Ethical Matrix in Evaluation of The Question of Downer Cattle Transportterry whitingÎncă nu există evaluări

- Eksamen The RejectionDocument5 paginiEksamen The RejectionAidan SmedegaardÎncă nu există evaluări

- Employee Disciplinary FormDocument3 paginiEmployee Disciplinary FormThanh ThuyÎncă nu există evaluări

- Lead Magnet 5 Minute Grace Period 1Document3 paginiLead Magnet 5 Minute Grace Period 1Lawrence BerezinÎncă nu există evaluări

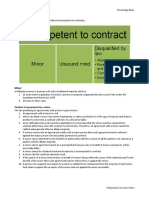

- Competency To Contract: MinorDocument4 paginiCompetency To Contract: MinorZeeshan BakaliÎncă nu există evaluări

- Article 443 - ExplanationsDocument2 paginiArticle 443 - ExplanationsFritzie G. PuctiyaoÎncă nu există evaluări

- Project Proposal Outline Form (Ppof)Document4 paginiProject Proposal Outline Form (Ppof)Dane MartinezÎncă nu există evaluări

- Signs You - Re in A Toxic RelationshipDocument6 paginiSigns You - Re in A Toxic RelationshipJustice Anunaobi100% (1)

- What Group Defines Themselves Through A Rejection of The MainstreamDocument3 paginiWhat Group Defines Themselves Through A Rejection of The MainstreamXratedÎncă nu există evaluări

- Consumer Attitude Formation and Change: Consumer Behavior, Eighth EditionDocument35 paginiConsumer Attitude Formation and Change: Consumer Behavior, Eighth Editionjugnu4selfÎncă nu există evaluări

- Movie Analysis (The Boy in The Striped Pajamas)Document2 paginiMovie Analysis (The Boy in The Striped Pajamas)2022ctecarlonscÎncă nu există evaluări

- Decentering The Ego-Self and Releasing The Care-ConsciousnessDocument14 paginiDecentering The Ego-Self and Releasing The Care-ConsciousnessFille e BeauÎncă nu există evaluări

- The CarpenterDocument10 paginiThe CarpenterSukanya V. MohanÎncă nu există evaluări

- (Philosophy in The Roman World) Raphael Woolf - Cicero - The Philosophy of A Roman Sceptic-Routledge (2015)Document269 pagini(Philosophy in The Roman World) Raphael Woolf - Cicero - The Philosophy of A Roman Sceptic-Routledge (2015)Catalina Gonzalez100% (3)

- UnityMag - Jul - Aug - Catherine PonderDocument4 paginiUnityMag - Jul - Aug - Catherine PonderZenaÎncă nu există evaluări

- IE Meter Application Form Regulatory Rev 6Document5 paginiIE Meter Application Form Regulatory Rev 6Abraham mayomikunÎncă nu există evaluări

- Complete The Form Below. Write No More Than Three Words And/Or A Number For Each AnswerDocument4 paginiComplete The Form Below. Write No More Than Three Words And/Or A Number For Each AnswerCooperative LearningÎncă nu există evaluări

- 2019 Police Officer Exam Study GuideDocument41 pagini2019 Police Officer Exam Study GuideBenjamin WilliamÎncă nu există evaluări

- When Someone You Love Is Toxic - How To Let Go, Without GuiltDocument1 paginăWhen Someone You Love Is Toxic - How To Let Go, Without GuiltDaniel Bryan TarongaÎncă nu există evaluări

- Outline Structure For Literary Analysis EssayDocument4 paginiOutline Structure For Literary Analysis EssayProbinciana's TVÎncă nu există evaluări

- School Form Checking Report SFCRDocument10 paginiSchool Form Checking Report SFCRRene Rey B. SulapasÎncă nu există evaluări

- Progress Check Practice Revisi N Del Intento PDFDocument7 paginiProgress Check Practice Revisi N Del Intento PDFYordy Rodolfo Delgado Rosario100% (1)

- Behavioral and Organizational Issues in Management Accounting and Control SystemsDocument3 paginiBehavioral and Organizational Issues in Management Accounting and Control SystemsCha ChaÎncă nu există evaluări

- Public International Law General Principles Municipal LAW International LAWDocument50 paginiPublic International Law General Principles Municipal LAW International LAWDon Renz San JoseÎncă nu există evaluări

- Assignment On: Discuss The Provisions Relating To Injunction Under The Code of Civil Procedure, 1908Document5 paginiAssignment On: Discuss The Provisions Relating To Injunction Under The Code of Civil Procedure, 1908AsH TheSutoVaiÎncă nu există evaluări