S-ar putea să vă placă și

- Business Case ROI Workbook For IT Initiatives: On This WorksheetDocument33 paginiBusiness Case ROI Workbook For IT Initiatives: On This WorksheetMrMaui100% (1)

- 790 GMAT TargetDocument4 pagini790 GMAT TargetKodwoP100% (2)

- Wiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesDe la EverandWiley Not-for-Profit GAAP 2017: Interpretation and Application of Generally Accepted Accounting PrinciplesÎncă nu există evaluări

- F7 Interactive Self Study Guide by AimDocument25 paginiF7 Interactive Self Study Guide by AimBeryl Maliakkal100% (1)

- F5 FinalDocument18 paginiF5 FinalPrashant PandeyÎncă nu există evaluări

- Financing Your Business in GhanaDocument40 paginiFinancing Your Business in GhanaKodwoPÎncă nu există evaluări

- F7 Workbook Q & A PDFDocument247 paginiF7 Workbook Q & A PDFREGIS IzereÎncă nu există evaluări

- Solutions Manual to Accompany Introduction to Quantitative Methods in Business: with Applications Using Microsoft Office ExcelDe la EverandSolutions Manual to Accompany Introduction to Quantitative Methods in Business: with Applications Using Microsoft Office ExcelÎncă nu există evaluări

- Accounting and Finance Policies and ProceduresDe la EverandAccounting and Finance Policies and ProceduresEvaluare: 4 din 5 stele4/5 (2)

- Fi instrument calc and accountingDocument47 paginiFi instrument calc and accountingInformation InsidserÎncă nu există evaluări

- Acca F7 Questions and AnswersDocument1 paginăAcca F7 Questions and AnswersRezaul AlamÎncă nu există evaluări

- One-CHRP - 0120 - Strategic Intent & BSC - Arry EkanantaDocument70 paginiOne-CHRP - 0120 - Strategic Intent & BSC - Arry EkanantaAffan Ghaffar Ahmad100% (3)

- Critical Financial Review: Understanding Corporate Financial InformationDe la EverandCritical Financial Review: Understanding Corporate Financial InformationÎncă nu există evaluări

- 2017 BPP Passcard F9 PDFDocument129 pagini2017 BPP Passcard F9 PDFSanam AlamÎncă nu există evaluări

- Revision f8 NotesDocument104 paginiRevision f8 NotesRanie Syafiqah JafferieÎncă nu există evaluări

- Guide to Strategic Management Accounting for managers: What is management accounting that can be used as an immediate force by connecting the management team and the operation field?De la EverandGuide to Strategic Management Accounting for managers: What is management accounting that can be used as an immediate force by connecting the management team and the operation field?Încă nu există evaluări

- ACCA P4 December 2015 NotesDocument164 paginiACCA P4 December 2015 NotesopentuitionIDÎncă nu există evaluări

- ACCA F7 Revision Mock June 2013 ANSWERS Version 4 FINAL at 25 March 2013 PDFDocument24 paginiACCA F7 Revision Mock June 2013 ANSWERS Version 4 FINAL at 25 March 2013 PDFPiyal Hossain100% (1)

- ACCA F5 LSBF Class Notes December 2011Document15 paginiACCA F5 LSBF Class Notes December 2011GT Boss AvyLaraÎncă nu există evaluări

- Understanding IFRS Fundamentals: International Financial Reporting StandardsDe la EverandUnderstanding IFRS Fundamentals: International Financial Reporting StandardsÎncă nu există evaluări

- Financial Reporting A Complete Guide - 2020 EditionDe la EverandFinancial Reporting A Complete Guide - 2020 EditionÎncă nu există evaluări

- Cima E1Document5 paginiCima E1Enoch Abassey0% (1)

- F1FAB Revision Question Bank - Contents - j14-j15 (Encrypted)Document144 paginiF1FAB Revision Question Bank - Contents - j14-j15 (Encrypted)karan100% (3)

- ACCA F8 Audit and Assurance Revision Notes 2017 PDFDocument84 paginiACCA F8 Audit and Assurance Revision Notes 2017 PDFJudithÎncă nu există evaluări

- ACCA F5 Linear Programming RevisionDocument4 paginiACCA F5 Linear Programming RevisionZoe ChimÎncă nu există evaluări

- Tuition Mock D11 - F7 Questions FinalDocument11 paginiTuition Mock D11 - F7 Questions FinalRenato WilsonÎncă nu există evaluări

- F5 ATC Pass Card 2012 PDFDocument102 paginiF5 ATC Pass Card 2012 PDFsaeed_r2000422100% (1)

- Exam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationDocument61 paginiExam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationMyDustbin2010100% (1)

- MCQ 1-Questions f5 AccaDocument6 paginiMCQ 1-Questions f5 AccaAmanda7100% (1)

- ACCA F5 NotesDocument244 paginiACCA F5 Notesfatehsaleh100% (4)

- MBA Managerial Economics Distance Mode Presessional Assignment 2016Document2 paginiMBA Managerial Economics Distance Mode Presessional Assignment 2016Tawanda Zimbizi0% (1)

- F7 (Financial Reporting) Trainer-GuideDocument29 paginiF7 (Financial Reporting) Trainer-GuideNguyen NhanÎncă nu există evaluări

- F7 Sir Zubair NotesDocument119 paginiF7 Sir Zubair NotesAli OpÎncă nu există evaluări

- Mock Exam QuestionsDocument21 paginiMock Exam QuestionsDixie CheeloÎncă nu există evaluări

- Part B Notes: CVP AnalysisDocument31 paginiPart B Notes: CVP AnalysisZakariya PkÎncă nu există evaluări

- F4CLENG Revision Question Bank - Sample - D14 J15 PDFDocument82 paginiF4CLENG Revision Question Bank - Sample - D14 J15 PDFMuhib EffendiÎncă nu există evaluări

- Financial Reporting: March/June 2016 - Sample QuestionsDocument7 paginiFinancial Reporting: March/June 2016 - Sample QuestionsViet Nguyen QuocÎncă nu există evaluări

- f5 SQB 15 Sample PDFDocument51 paginif5 SQB 15 Sample PDFCecilia Mfene Sekubuwane0% (1)

- f1 Answers Nov14Document14 paginif1 Answers Nov14Atif Rehman100% (1)

- T4 Mocks - Hafiz Muhammad Adnan (Sialkot)Document67 paginiT4 Mocks - Hafiz Muhammad Adnan (Sialkot)adnan79100% (1)

- ACCA F5 Exam Tips for Activity Based CostingDocument32 paginiACCA F5 Exam Tips for Activity Based CostingVagabond Princess Rj67% (3)

- 2013 Paper F9 QandA SampleDocument41 pagini2013 Paper F9 QandA SampleSajid AliÎncă nu există evaluări

- FREE ACCA F3 Practice KIT - Free Accountancy Resources - Video Lectures - Online Forums - Notes - Past Papers - Mock ExamsDocument6 paginiFREE ACCA F3 Practice KIT - Free Accountancy Resources - Video Lectures - Online Forums - Notes - Past Papers - Mock Examsmashooqali100% (1)

- NPV Practice CompleteDocument5 paginiNPV Practice CompleteShakeel AslamÎncă nu există evaluări

- f8 RQB 15 Sample PDFDocument98 paginif8 RQB 15 Sample PDFChandni VariaÎncă nu există evaluări

- ACCA Study Guide f5Document4 paginiACCA Study Guide f5tho1009Încă nu există evaluări

- ACCA F5 Revision Mock June 2013 ANSWERS Version 5 FINAL at 25 March 2013Document20 paginiACCA F5 Revision Mock June 2013 ANSWERS Version 5 FINAL at 25 March 2013Shahrooz Khan0% (1)

- Principle-Based vs. Rule-Based AccountingDocument2 paginiPrinciple-Based vs. Rule-Based AccountingPeter MastersÎncă nu există evaluări

- f2 Revesion Notes by AmmarDocument76 paginif2 Revesion Notes by Ammarammar_acca9681100% (1)

- ACCA F7 Exam ReoprtDocument5 paginiACCA F7 Exam Reoprtkevior2Încă nu există evaluări

- ACCA F7 December 2013 Q1 Workings Consolidated Financial StatementsDocument3 paginiACCA F7 December 2013 Q1 Workings Consolidated Financial StatementsKian TuckÎncă nu există evaluări

- F7 Technical ArticlesDocument121 paginiF7 Technical ArticlesNicquain0% (1)

- CMA (USA) - Recorded Lectures Details V2Document15 paginiCMA (USA) - Recorded Lectures Details V2frostyfusioncreameryÎncă nu există evaluări

- F8 - BPP Passcard (2017)Document161 paginiF8 - BPP Passcard (2017)Dime PierrowÎncă nu există evaluări

- CMA USA Ratio Definitions 2015Document4 paginiCMA USA Ratio Definitions 2015Shameem JazirÎncă nu există evaluări

- f2 Acca Lesson6 (Labour)Document10 paginif2 Acca Lesson6 (Labour)Mikhail Banhan100% (1)

- ACCA Paper F9 Full Study Textbook (Sample Download v2)Document30 paginiACCA Paper F9 Full Study Textbook (Sample Download v2)accountancylad100% (1)

- Acca f8 MockDocument8 paginiAcca f8 MockMuhammad Kamran Khan100% (3)

- Inventory valuation Complete Self-Assessment GuideDe la EverandInventory valuation Complete Self-Assessment GuideEvaluare: 4 din 5 stele4/5 (1)

- Cost Of Capital A Complete Guide - 2020 EditionDe la EverandCost Of Capital A Complete Guide - 2020 EditionEvaluare: 4 din 5 stele4/5 (1)

- Session 1 - FM Function and Basic Investment Appraisal: ACCA F9 Financial ManagementDocument8 paginiSession 1 - FM Function and Basic Investment Appraisal: ACCA F9 Financial ManagementKodwoPÎncă nu există evaluări

- Bank Ak Opening RequirementsDocument1 paginăBank Ak Opening RequirementsKodwoPÎncă nu există evaluări

- Experts On Remote Working-Compiled by Kodwo ArmahDocument14 paginiExperts On Remote Working-Compiled by Kodwo ArmahKodwoPÎncă nu există evaluări

- GHANAIAN Translation PDFDocument2 paginiGHANAIAN Translation PDFKodwoPÎncă nu există evaluări

- Acca f7 Slides 2014Document73 paginiAcca f7 Slides 2014KodwoP100% (1)

- HaddockDocument53 paginiHaddockKodwoPÎncă nu există evaluări

- Business Banking (Enterprise) Pricing Guide Effective 1st March, 2018Document2 paginiBusiness Banking (Enterprise) Pricing Guide Effective 1st March, 2018KodwoPÎncă nu există evaluări

- PS MusicDocument7 paginiPS MusicKodwoPÎncă nu există evaluări

- F9 Acowtancy Notes PDFDocument202 paginiF9 Acowtancy Notes PDFKodwoPÎncă nu există evaluări

- F9 Acowtancy Notes PDFDocument202 paginiF9 Acowtancy Notes PDFKodwoPÎncă nu există evaluări

- Studentcompanion VCA3qDocument15 paginiStudentcompanion VCA3qKodwoPÎncă nu există evaluări

- Kaplan ACCA Goodwill ArticleDocument3 paginiKaplan ACCA Goodwill ArticleKodwoPÎncă nu există evaluări

- Oxford University DonsDocument4 paginiOxford University DonsKodwoPÎncă nu există evaluări

- Kaplan ACCA Goodwill ArticleDocument3 paginiKaplan ACCA Goodwill ArticleKodwoPÎncă nu există evaluări

- How To Pass The P2 ExamDocument2 paginiHow To Pass The P2 ExamKodwoPÎncă nu există evaluări

- Gaap Finrep33Document8 paginiGaap Finrep33KodwoPÎncă nu există evaluări

- ACCA ChangesDocument14 paginiACCA ChangesKodwoPÎncă nu există evaluări

- BHP Billiton Mitsubishi AllianceDocument3 paginiBHP Billiton Mitsubishi AllianceKodwoPÎncă nu există evaluări

- Kaplan ACCA Goodwill ArticleDocument3 paginiKaplan ACCA Goodwill ArticleKodwoPÎncă nu există evaluări

- f7 Students Must ReadDocument3 paginif7 Students Must ReadKodwoPÎncă nu există evaluări

- Your Chances of Passing. Increase: Francis' Study GuidesDocument1 paginăYour Chances of Passing. Increase: Francis' Study GuidesKodwoPÎncă nu există evaluări

- Anglogold Ashanti: - LocationDocument2 paginiAnglogold Ashanti: - LocationKodwoPÎncă nu există evaluări

- ACCA ChangesDocument14 paginiACCA ChangesKodwoPÎncă nu există evaluări

- Tom Clendon's RecommendationsDocument2 paginiTom Clendon's RecommendationsKodwoPÎncă nu există evaluări

- F7 CourseDocument118 paginiF7 CourseKodwoP100% (3)

- Magazines in GhanaDocument2 paginiMagazines in GhanaKodwoPÎncă nu există evaluări

- Completed Example FileDocument2 paginiCompleted Example FileKodwoPÎncă nu există evaluări

- Chap 04Document87 paginiChap 04Tùng NguyễnÎncă nu există evaluări

- Samsung Care Plus Terms and Conditions PDFDocument10 paginiSamsung Care Plus Terms and Conditions PDFav86Încă nu există evaluări

- BT India Factsheet - NewDocument2 paginiBT India Factsheet - NewsunguntÎncă nu există evaluări

- E Channel Product FinalDocument100 paginiE Channel Product Finalakranjan888Încă nu există evaluări

- Case 1 - Iguazu Offices Financial ModelDocument32 paginiCase 1 - Iguazu Offices Financial ModelapoorvnigÎncă nu există evaluări

- Scope and Methods of EconomicsDocument4 paginiScope and Methods of EconomicsBalasingam PrahalathanÎncă nu există evaluări

- Project Proposal: ESC472 - Electrical and Computer Capstone Design Division of Engineering ScienceDocument19 paginiProject Proposal: ESC472 - Electrical and Computer Capstone Design Division of Engineering Scienceapi-140137201Încă nu există evaluări

- Performance Review and GoalsDocument3 paginiPerformance Review and GoalsTaha NabilÎncă nu există evaluări

- Doing Research in Business ManagementDocument20 paginiDoing Research in Business Managementravi_nyseÎncă nu există evaluări

- Prelim Quiz 2 Strategic ManagementDocument4 paginiPrelim Quiz 2 Strategic ManagementRoseÎncă nu există evaluări

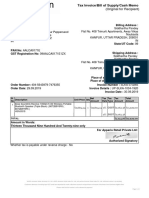

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 paginăTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Satyam SinghÎncă nu există evaluări

- MIC 2e Study Guide Complete 2Document230 paginiMIC 2e Study Guide Complete 2anna_jankovskaÎncă nu există evaluări

- Stages in Consumer Decision Making ProcessDocument19 paginiStages in Consumer Decision Making ProcessAnshita GargÎncă nu există evaluări

- Sarah Williams CVDocument2 paginiSarah Williams CVsarahcwilliamsÎncă nu există evaluări

- Advantages and Disadvantages of Business Entity Types.Document3 paginiAdvantages and Disadvantages of Business Entity Types.Kefayat Sayed AllyÎncă nu există evaluări

- Kalyan Pharma Ltd.Document33 paginiKalyan Pharma Ltd.Parth V. PurohitÎncă nu există evaluări

- The Daimlerchrysler Merger - A Cultural Mismatch?Document10 paginiThe Daimlerchrysler Merger - A Cultural Mismatch?frankmdÎncă nu există evaluări

- The Polka-Unilever Merger in PakistanDocument1 paginăThe Polka-Unilever Merger in PakistanirfanÎncă nu există evaluări

- Richard ADocument2 paginiRichard AsubtoÎncă nu există evaluări

- TTK Report - 2011 and 2012Document2 paginiTTK Report - 2011 and 2012sgÎncă nu există evaluări

- An Examination of Audit Delay Further Evidence From New ZealandDocument13 paginiAn Examination of Audit Delay Further Evidence From New ZealandAmelia afidaÎncă nu există evaluări

- Alk2-Brief Bible History - MachenDocument80 paginiAlk2-Brief Bible History - Machenanthonius70Încă nu există evaluări

- IBS Renault Nissan Alliance FinalDocument24 paginiIBS Renault Nissan Alliance FinalakshaykgÎncă nu există evaluări

- 0452 s05 QP 2Document16 pagini0452 s05 QP 2Nafisa AnwarAliÎncă nu există evaluări

- Dominos PizzaDocument14 paginiDominos PizzahemantÎncă nu există evaluări

- What Are Mutual Funds?Document8 paginiWhat Are Mutual Funds?ShilpiVaishkiyarÎncă nu există evaluări

- Tally PPT For Counselling1Document11 paginiTally PPT For Counselling1lekhraj sahuÎncă nu există evaluări

- Edmonton City Council Report On Downtown ArenaDocument61 paginiEdmonton City Council Report On Downtown ArenaedmontonjournalÎncă nu există evaluări