Small rebound in confidence in China

has somewhat gained pace in China.

Nordic companies more optimistic and continue to invest

BUSINESS PROSPECTS AND PROFIT EXPECTATIONS UP. Expansion plans remain high,

with both investment and recruitments plans up from the last survey.

THURSDAY 13 MARCH 2014

SEB CHINA FINANCIAL INDEX AT 61.4, up from 58 in September, suggesting business activity Fredrik Hhnel

General Manager Tony Wang Markets SEB Shanghai +86 21 53966681

SHARP FALL IN CONCERN OVER CUSTOMER DEMAND, further indicating a rebound in optimism. But concerns over skilled labour shortage and customer payment ability are up.

SOMEWHAT BETTER DEMAND IN CHINA

Contrary to other business confidence surveys published recently, SEBs China Financial Index shows that Northern European companies have become more optimistic on business conditions in the Chinese market than they were six months ago. Both the business climate and profits are expected to improve, with half of the respondents showing a positive view on overall business conditions. 45% expect profits to rise in the coming six months and only 6% expect profits to deteriorate. Half of the respondents expect business conditions and profits to remain the same.

Historical development for SEBs China Financial Index

increase staff in China in the coming six months, while 11% are planning for significant increases. Hence, the total number planning staff increases has gone up to 56% in this survey from 43% when we asked the same question in September.

China Financial Index, March 2014

Source: SEB Shanghai. Colored stacks are the most recent results. Grey stacks show results in September 2013 and March 2012, respectively

Nordic companies also continue to invest in China. In this survey, 55% of respondents are planning for modest investments in the coming six months, up from 43% in the last survey. 13% plan for significant investments whereas one-third of all respondents do not plan further investments in China at the moment. When asked about hiring plans, they have also gone up since the last survey. 45% say that they will

Fewer companies worry about falling demand for their products in this survey, with 27% now viewing the subject as the main concern (38% in September and 44% one year ago). Another 27% say that competition is their main concern, which is in line with our last survey. The two concerns that increased most in this survey are skilled labour shortage (20% of respondents say it is their main concern) and clients payment ability (10% rate it their biggest concern). Plans for salary increases have moved in two directions since September. Now, roughly one of ten respondents expects salaries to increase by more than 10% in 2014, which is higher than in the last survey.

Important: Your attention is drawn to the statement on the back of this report which affects your rights

China Financial Index

At the same time, however, the number of companies that expect salary increases to be 3-4% has also increased, with one of ten now saying that will be the level. One-third of respondents plan for salary increases of 5-6%, another one-third say 7-8% and one of five say 9-10% when asked about salary increases during 2014. Lower inflation rates in China seem to have had no effect on salary changes, as these numbers are, on an aggregated level, in line with our last survey. However, costs continue to increase for companies in China. In discussions with clients active in the manufacturing field, an increasing number of companies mention environmental compliance costs, salary costs and costs for rent putting pressure on margins. Our index is not completely in line with other data which have pointed to a worsening business climate in the last couple of months. For example, HSBCs Purchasing Managers Index (PMI) hit a sevenmonth low of 48.5 in February. On the other hand, as our index is only done on a six-month basis, it reflects more medium-term changes in business conditions. GDP figures for Q4 were lower than Q3 and many other indications published in January and February indicate that the economy is in the midst of a slowdown.

OUR CONCLUSIONS Since our survey is done every six months, the results of the March survey must be compared with the latest survey in September and do not capture more shortterm changes in sentiment. The conclusion is that Nordic and German companies are more positive now than they were in September. The most significant change is that many companies have changed their mind and do not see falling customer demand as their main concern. Survey results indicate that it is a little bit business as usual in China, with expected sales and profit growth. Hence, slowing GDP growth and reports of a looming hard landing due to Chinas exceptional credit boom, as many analysts have warned, do not seem to show up in companies results. On the contrary, companies continue to expand, with more investments and recruitments in China.

expectations but dropped 18,1% in February. Imports rose 7% on a year-to-year basis in January but also fell in February. Economists and international newspaper headlines are increasingly concerned with credit quality in the Chinese banking system, as well as growth of the shadow banking sector. Bank lending surged in January, reaching RMB 217bn, the highest in about four years, while economic growth has continued to fall, raising concerns that the quality in the allocation of capital has continued to deteriorate.

SEBs main scenario is that Chinas growth continues to decelerate, and we expect GDP growth to ease to 7.4% in 2014 and 7.0% in 2015.

EURO CROSS-BORDER CURRENCY

Almost no company uses CNH across borders Although the Chinese government is trying to bolster the use of RMB for trade and investment purposes in and out of China, North European companies continue to use foreign currencies as their main cross-border currency. Only 5% use the RMB, or CNH as it is often referred to, outside China. When asked which currency is the preferred one for cross-border business, 52% mention EUR as their main currency and 36% say they use USD. Only 7% say Scandinavian currencies, which is slightly higher than previous surveys. Half of the companies expect the RMB exchange rate to appreciate against the USD in the coming six months, and 40% think it will be stable. The same number of companies as previously (11%) believes the RMB will weaken against the dollar. Half the companies think interest rates will remain unchanged. 11% expect a falling rate and 43% think rates will go up.

Modest recovery

7.4% GDP GROWTH EXPECTED 2014

Chinas economy grew by 7.7% in the fourth quarter of 2013 compared to the same quarter 2012. This was a slight deceleration from 7.8% in the third quarter. China has retained a target of 7.5% GDP growth for 2014. Chinas official PMI hit an eight-month low in February at 50.2, adding signs of a slowdown in Chinas economy. Chinese exports accelerated faster than expected in January, up by 10.6%, beating

China Financial Index

Until early March 2014, the RMB has against all odds depreciated by 1.12% against the USD. The Chinese central bank (PBOC), with the objective to promote two-way volatility on the onshore market, has through market interventions interrupted the widely accepted one-way move of the RMB. For the 2014 full-year forecast, SEB still expects the RMB to appreciate towards 6.00 against the USD, but with the notion that the ride with be bumpy ahead.

SUBJECT: Fixed Asset Investment Plans Compared to the last issue, investment plans among corporates remain modest. More than half (55%) of all corporates are planning to have modest investments, compared to 43% six months earlier. 32% plan to not have any investment, which is a decrease from 43% in the last survey. Only 13% are considering major investment plans, which is a slowdown from 15% last September. Our result indicates a marginal change among the respondents. Corporates remain cautious for any major investment, despite higher profit expectations (see above). As many of our clients are within the capital-intensive manufactory sector, the average manager seems to prefer holding investments tight in the current environment. (See graph 2 on page 5)

Survey Results

INFORMATION ABOUT THE SURVEY

SEBs China Financial Survey is based on input from CEOs and CFOs at 50 subsidiaries of major Swedish, Danish, Finnish, Norwegian and German companies. Most of the companies have a global turnover of more than EUR 500mn. The survey is web-based and confidential, and was carried out from 13 February through 4 March, 2014.

SUBJECT: Business Climate/Profit Expectations Looking ahead, Northern European subsidiary managers have become slightly more optimistic compared to six months ago. Among these companies, 38% (vs. 28% in September 2013) believe conditions will be favourable, while 11% expect conditions to be very favourable. The respondents who expect conditions to be not so favourable have decreased to 6% from 15% in the last survey. Nevertheless, the majority (45%) still expect the business climate to remain average in the coming six months In terms of profit expectations, 45% expect higher profits compared to 40% in September. Managers with very strong views in either direction have decreased. 49% of all respondents believe profit will stay unchanged. China grew by 7.7% in 2013, slightly above the market expectation of 7.6%. The recent NPC meeting has confirmed the GDP growth target for 2014 will stay at 7.5%, compared to SEBs forecast of 7.4%. Meanwhile, the official PMI index for February came in somewhat mixed, with non-manufacturing at a threemonth high of 55, and the manufacturing equivalent at 50.2. These figures support the view that the investment-intensive manufacturing sector is gradually slowing down. (See graphs 1 and 3 on page 5)

SUBJECT: Employment Structure Corporate managers of Northern Europe continue to expand in terms of workforce in China. 45% are in need of increasing staff numbers, compared to 38% six months ago. 11% would like to increase their workforce significantly, up from 5% in the last survey. Similar to last year, 11% of corporates need to reduce their workforce in the coming half year. (See graphs 4 on page 5) SUBJECT: Salary increase More than half of the surveyed corporates are planning to increase salaries between 5-8%, which is slightly lower than the previous survey. 11% expect a wage increase above 10%, which is up from 2% six months ago. The average manager expects a 7% salary increase. Our survey shows that the increasingly shortage of skilled labour is a major concern among corporates, which may explain the escalating salary trend in China. (See graph 5 on page 5)

SUBJECT: Funding Needs Funding needs among Northern European corporates remain stable. 36% of managers expect funding needs to increase, up from 35% last September. 62%

China Financial Index

expect the funding situation to remain unchanged. With normalisinginvestment plans and slightly higher profit expectations (see above), funding needs will most likely stay stable going forward. (See graph 6 on page 5)

labour shortage stands for the largest increase and remains as a top-three concern among corporates. (See graph 11 on page 6)

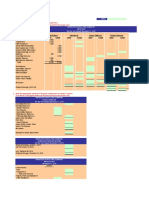

CHINA FINANCIAL INDEX COMPOSITION

The SEB China Financial Index in March had a value of 61.4, indicating a slightly positive attitude. A value of 50 would indicate a neutral view. The index is based on four components with the following ranking in this survey: General Business Climate 61, Profit Expectations 58, Investment Plans 66, and Employment Plans 61. (See the graph on page 1)

SUBJECT: FX and Interest Rates Similar to last year, the predominant view held by local managers is that China will keep its interest rate stable for the coming six months. Surprisingly, 43% of all respondents are hawkish towards a rate hike, compared to 17% in the earlier survey. Only 11% expects a rate cut, compared to 26% last year. In China, the current interest rate remains at 6% while the 12-month benchmark deposit rate is at 3.0%. CPI in January rose by 2.5% year-on-year, in accordance with market expectations. Producer prices, on the other hand, slid for the 23rd consecutive month, dropping 1.6%, suggesting weakening demand in factory goods. In this survey, several managers hold a view regarding the direction of the RMB. Half of the managers expect the RMB to appreciate against the USD, compared to 40% in the last survey. 40% is unbiased in terms of the RMB fluctuation, while 11% believe in a weaker RMB in six months time. Many corporates (41%) are still in favour of hedging some or most of their FX exposure on the onshore market. At the same time, 28% are hedging through their head office via off-shore market, versus 33% six months earlier. As China is aiming towards full liberalisation of the FX market, a two-way volatility will subsequently increase the needs of import/export flow hedging among corporate managers. (Please see graphs 7 and 8 on page 5 plus 10 on page 6)

SUBJECT: Main Concerns More than a quarter of all managers expressed competition as the largest concern. At the same time, 25% put it as the second largest concern. Client demand continues to be an important factor, albeit with a decrease this survey to 27% from 38%. Skilled

China Financial Index

1. BUSINESS CONDITIONS

5. AVERAGE SALARY INCREASE

2. FIXED ASSET INVESTMENT PLANS

6. FUNDING NEEDS

3. PROFIT EXPECTATIONS

7. RMB AGAINST USD

4. NUMBER OF EMPLOYEES

8. RMB INTEREST RATES

China Financial Index

9. MAIN TRADING CURRENCY

11. MAIN CONCERNS

10. HEDGING STRATEGY

12. MAIN INDEX

Source: SEB Shanghai. Grey stacks are indicating companies answers in the last two surveys in September 2013 and March 2013

IMPORTANT: THIS STATEMENT AFFECTS YOUR RIGHTS

This Report is produced by Skandinaviska Enskilda Banken AB (publ) for institutional investors only. Information and opinions contained within this document are given in good faith and are based on sources believed reliable. We do not represent that they are accurate or complete. No liability is accepted for any direct or indirect or consequential loss resulting from reliance on this document. Changes may be made to opinions or information contained herein without notice. Any US person wishing to obtain further information about this report should contact the New York branch of the Bank, which has distributed this report in the US. Skandinaviska Enskilda Banken AB (publ) is a member of the London Stock Exchange. It is regulated by the Securities and Futures Authority for the conduct of investment business in the UK.

S-ar putea să vă placă și

- Insights From 2014 of Significance For 2015Document5 paginiInsights From 2014 of Significance For 2015SEB GroupÎncă nu există evaluări

- Economic Insights: Riksbank To Lower Key Rate, While Seeking New RoleDocument3 paginiEconomic Insights: Riksbank To Lower Key Rate, While Seeking New RoleSEB GroupÎncă nu există evaluări

- Economic Insights: The Middle East - Politically Hobbled But With Major PotentialDocument5 paginiEconomic Insights: The Middle East - Politically Hobbled But With Major PotentialSEB GroupÎncă nu există evaluări

- Economic Insights: Subtle Signs of Firmer Momentum in NorwayDocument4 paginiEconomic Insights: Subtle Signs of Firmer Momentum in NorwaySEB GroupÎncă nu există evaluări

- CFO Survey 1403: Improving Swedish Business Climate and HiringDocument12 paginiCFO Survey 1403: Improving Swedish Business Climate and HiringSEB GroupÎncă nu există evaluări

- SE-Banken, Investment Outlook, Dec 2013, "Market Hopes Will Require Some Evidence"Document35 paginiSE-Banken, Investment Outlook, Dec 2013, "Market Hopes Will Require Some Evidence"Glenn ViklundÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Olive Branch Foundation 2005 990Document21 paginiOlive Branch Foundation 2005 990TheSceneOfTheCrimeÎncă nu există evaluări

- 2012-2013 Mercantile USC-LAWDocument17 pagini2012-2013 Mercantile USC-LAWrye736Încă nu există evaluări

- Long-Term Social Impacts and Financial Costs of Foreclosure On Families and Communities of ColorDocument49 paginiLong-Term Social Impacts and Financial Costs of Foreclosure On Families and Communities of ColorJH_CarrÎncă nu există evaluări

- Engineering Economy: Compound InterestDocument16 paginiEngineering Economy: Compound InterestLETADA NICOLE MAEÎncă nu există evaluări

- Classification of CostsDocument6 paginiClassification of CostsKate Crystel reyesÎncă nu există evaluări

- Return On Equity:: A Compelling Case For InvestorsDocument15 paginiReturn On Equity:: A Compelling Case For InvestorsPutri LucyanaÎncă nu există evaluări

- How To Value Straight Vanilla Bonds (Questions)Document4 paginiHow To Value Straight Vanilla Bonds (Questions)hadosib264Încă nu există evaluări

- Chapter 1 - MFRS140 - QssssDocument9 paginiChapter 1 - MFRS140 - QssssCountess DraculaÎncă nu există evaluări

- Trade Lifecycle 1Document15 paginiTrade Lifecycle 1RamÎncă nu există evaluări

- Determinants of Signaling by Banks Through Loan Loss ProvisionsDocument9 paginiDeterminants of Signaling by Banks Through Loan Loss ProvisionsabhinavatripathiÎncă nu există evaluări

- Wahlen Int3e EX03-11Document3 paginiWahlen Int3e EX03-11林義哲Încă nu există evaluări

- Case Study Merrill LYnchDocument17 paginiCase Study Merrill LYnchSandeep YadavÎncă nu există evaluări

- Module 8 Benefit Cost Ratio PDFDocument4 paginiModule 8 Benefit Cost Ratio PDFRio DpÎncă nu există evaluări

- Do Stocks Outperform Treasury BillsDocument53 paginiDo Stocks Outperform Treasury BillsblacksmithMGÎncă nu există evaluări

- BUS 360 Chapter 12 14 - Verhallen-8eDocument90 paginiBUS 360 Chapter 12 14 - Verhallen-8esrrutkowÎncă nu există evaluări

- Finance For Executives 5Th Edition Full ChapterDocument41 paginiFinance For Executives 5Th Edition Full Chapterstephanie.ullmann917100% (26)

- Financial Markets and InstitutionsDocument18 paginiFinancial Markets and InstitutionsAvni Sharma100% (1)

- Derivatives Case StudyDocument39 paginiDerivatives Case StudyVarun AgrawalÎncă nu există evaluări

- Financial Sector Presentation AnchalDocument20 paginiFinancial Sector Presentation AnchalPrashant Kumar100% (1)

- Credit RiskDocument15 paginiCredit RiskjoshdreamzÎncă nu există evaluări

- Activity 01Document3 paginiActivity 01Mahra AlMazroueiÎncă nu există evaluări

- Chapter 3 Securities MarketDocument50 paginiChapter 3 Securities Marketsharktale2828100% (1)

- Motilal Oswal Financial Services LTDDocument5 paginiMotilal Oswal Financial Services LTDseawoodsÎncă nu există evaluări

- Long Run Relationship Between South Asian Equity Markets and Equity Markets of Developed WorldDocument23 paginiLong Run Relationship Between South Asian Equity Markets and Equity Markets of Developed Worldmansoor_uosÎncă nu există evaluări

- BAFIA FOR RBB Bank CLassDocument29 paginiBAFIA FOR RBB Bank CLassDagendra BasnetÎncă nu există evaluări

- Asian Paints: Prepared byDocument54 paginiAsian Paints: Prepared bylaxmi joshiÎncă nu există evaluări

- Maskey Bikesh - SMART MONEY CONCEPTS IN THE FOREX MARKET - 011915Document68 paginiMaskey Bikesh - SMART MONEY CONCEPTS IN THE FOREX MARKET - 011915AFOLABIÎncă nu există evaluări

- Capital Structure Problems AssignmentDocument3 paginiCapital Structure Problems AssignmentRamya Gowda100% (2)

- Wlcon - PS Wlcon PMDocument10 paginiWlcon - PS Wlcon PMP RosenbergÎncă nu există evaluări

- Ikea HRDocument10 paginiIkea HRMaugli JungleÎncă nu există evaluări