S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Accenture Social Banking RetailDocument12 paginiAccenture Social Banking RetailMikhail DashkovÎncă nu există evaluări

- Analisa Investasi Dengan Feasibility Stu De749a7bDocument11 paginiAnalisa Investasi Dengan Feasibility Stu De749a7bIsti W.aÎncă nu există evaluări

- Al Dhaid Trading & Contracting Al Dhaid Trading ContractingDocument5 paginiAl Dhaid Trading & Contracting Al Dhaid Trading ContractingAbi JithÎncă nu există evaluări

- Banking SectorDocument8 paginiBanking SectorSupreet KaurÎncă nu există evaluări

- Credit Skills For Bankers Certificate Sme IndiaDocument4 paginiCredit Skills For Bankers Certificate Sme IndiaitsurarunÎncă nu există evaluări

- "Customer Attitude Towards COMMERCIAL LOANDocument58 pagini"Customer Attitude Towards COMMERCIAL LOANPulkit SachdevaÎncă nu există evaluări

- Ps 2Document8 paginiPs 2Amy BeansÎncă nu există evaluări

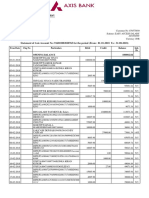

- Statement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Document9 paginiStatement of Axis Account No:916010083028765 For The Period (From: 01-01-2018 To: 31-08-2018)Saran ManiÎncă nu există evaluări

- Goibibo DocumentDocument2 paginiGoibibo DocumentUdit SinghalÎncă nu există evaluări

- EOI On Excess Bank ChargesDocument22 paginiEOI On Excess Bank ChargesOlufemi Moyegun100% (4)

- Association of Small Landowners in The Philippines v. Honorable Secretary of Agrarian ReformDocument9 paginiAssociation of Small Landowners in The Philippines v. Honorable Secretary of Agrarian Reformczabina fatima delicaÎncă nu există evaluări

- PSL-57A - Initial Exam Application BlankDocument5 paginiPSL-57A - Initial Exam Application BlankColin-James LoweÎncă nu există evaluări

- FAQs On Cheque Collection PolicyDocument1 paginăFAQs On Cheque Collection PolicyPrasant PrasadÎncă nu există evaluări

- Philippine National Bank Vs DeeDocument3 paginiPhilippine National Bank Vs DeeJezenEstherB.PatiÎncă nu există evaluări

- SIBL FINAL COVER Page EXTERNALDocument5 paginiSIBL FINAL COVER Page EXTERNALShahidullah RanaÎncă nu există evaluări

- B B F A R: ANK OF Aroda Inancial Nalysis EportDocument31 paginiB B F A R: ANK OF Aroda Inancial Nalysis Eportlaxmi_bodduÎncă nu există evaluări

- Bass vs. de La Rama DigestDocument2 paginiBass vs. de La Rama Digestdexter lingbananÎncă nu există evaluări

- Auditing ExamDocument14 paginiAuditing ExamJericha GolezÎncă nu există evaluări

- Top Largest Central Bank Rankings by Total AssetsDocument24 paginiTop Largest Central Bank Rankings by Total AssetsMayank AhujaÎncă nu există evaluări

- MagnetarDocument11 paginiMagnetarYokohama3000Încă nu există evaluări

- Research Project On SHG 5Document15 paginiResearch Project On SHG 5ashan.sharmaÎncă nu există evaluări

- Banking Ch03 - Bank Fund Management (Extended)Document23 paginiBanking Ch03 - Bank Fund Management (Extended)Indo WalelengÎncă nu există evaluări

- Vertical Integration-Emerging Trends and Challenges1.0Document15 paginiVertical Integration-Emerging Trends and Challenges1.0Madhavilatha JayanthiÎncă nu există evaluări

- Background of The CompaniesDocument7 paginiBackground of The CompaniesJerhome LunaÎncă nu există evaluări

- Role of Foreign Venture Capital Funds in IndiaDocument10 paginiRole of Foreign Venture Capital Funds in IndiaJames ManishÎncă nu există evaluări

- Comprehensive NotesDocument13 paginiComprehensive NotesBelle Andrea GozonÎncă nu există evaluări

- Full Download Book Financial Services PDFDocument41 paginiFull Download Book Financial Services PDFcalvin.williams888100% (13)

- Oxford - BoothDocument20 paginiOxford - BoothRamÎncă nu există evaluări

- Problem Sets Ce Review 2014Document93 paginiProblem Sets Ce Review 2014RyanCalleja33% (3)

- TR 7. Garcia v. CADocument2 paginiTR 7. Garcia v. CAJyrus CimatuÎncă nu există evaluări