S-ar putea să vă placă și

- My PDF File 3256fghgDocument1 paginăMy PDF File 3256fghgSachin67% (3)

- EpicorApplication UserGuide Part1of2 100700Document571 paginiEpicorApplication UserGuide Part1of2 100700lebbuu86% (7)

- Accounting Unit 1 NotesDocument20 paginiAccounting Unit 1 NotesNiranjan Sathianathen0% (2)

- Strategic Management Project - PARCODocument84 paginiStrategic Management Project - PARCOBilawal Shabbir100% (4)

- PSO ProjectDocument17 paginiPSO ProjectNadeem100% (4)

- Corporations, Autonomous Bodies ...Document72 paginiCorporations, Autonomous Bodies ...Haris Ali KhanÎncă nu există evaluări

- Subsequent Debit, Delivery Cost and Credit MemoDocument37 paginiSubsequent Debit, Delivery Cost and Credit MemoSrini VasanÎncă nu există evaluări

- 48-86 Ford Truck Catalog PDFDocument232 pagini48-86 Ford Truck Catalog PDFAlejandro Soto RIveraÎncă nu există evaluări

- InvoiceDocument1 paginăInvoicetausif alam0% (1)

- ClickTime ManualDocument291 paginiClickTime Manualopenid_I5nzX5l8100% (2)

- Mid Country Refinery: Refinery's Housing ComplexDocument8 paginiMid Country Refinery: Refinery's Housing ComplexNaveed AhmedÎncă nu există evaluări

- "Supply Chain Management of Pso": PresentersDocument17 pagini"Supply Chain Management of Pso": Presenterstaimoorkhan859538Încă nu există evaluări

- Strategic Management Project PARCODocument84 paginiStrategic Management Project PARCOshahzaib younas100% (1)

- PARCO (Pak Arab Oil Refinery) LTD Pakistan: Operation ManagementDocument23 paginiPARCO (Pak Arab Oil Refinery) LTD Pakistan: Operation Managementhoneyocp6911100% (1)

- Services Marketing Final Project Possession Processing: History and BackgroundDocument18 paginiServices Marketing Final Project Possession Processing: History and BackgroundHamza TayyabÎncă nu există evaluări

- ParcoDocument14 paginiParcoMus'ab UsmanÎncă nu există evaluări

- Sui Northern Gas Pipelines LimitedDocument3 paginiSui Northern Gas Pipelines LimitedAbeer_Ahsan_9557Încă nu există evaluări

- PARCO (Pak Arab Oil Refinery) LTD Pakistan: Operation ManagementDocument23 paginiPARCO (Pak Arab Oil Refinery) LTD Pakistan: Operation ManagementXtylish RajpootÎncă nu există evaluări

- PARCODocument57 paginiPARCOmuhammadtaimoorkhan100% (4)

- Final Project PSODocument31 paginiFinal Project PSOadeel80% (5)

- Parco Report (FINAL)Document28 paginiParco Report (FINAL)haroonrashid00767% (3)

- PsoDocument43 paginiPsoHassanj Amal100% (1)

- "Sui Southern Gas Company Limited": Strategic Management Report OnDocument25 pagini"Sui Southern Gas Company Limited": Strategic Management Report OnAsif MominÎncă nu există evaluări

- ParcoDocument24 paginiParcoSami UrRahmanÎncă nu există evaluări

- Pakgulf Construction (PVT.) LimitedDocument10 paginiPakgulf Construction (PVT.) LimitedUmairSadiqÎncă nu există evaluări

- Supply Chain of HascolDocument9 paginiSupply Chain of HascolqamarunnisaÎncă nu există evaluări

- Case Study Pakistan State OilDocument4 paginiCase Study Pakistan State OilDavidparkash Mirza100% (1)

- PEST AnalysisDocument5 paginiPEST AnalysisSultan HaiderÎncă nu există evaluări

- Hascol Ipo2016Document46 paginiHascol Ipo2016Rebekah SchmidtÎncă nu există evaluări

- PARCODocument22 paginiPARCOAeman ShakilÎncă nu există evaluări

- Pakistan Petroleum IndustryDocument67 paginiPakistan Petroleum IndustryUmber Zareen Siddiqui94% (17)

- CSS Solved Precis 2014 - 2017 PDFDocument13 paginiCSS Solved Precis 2014 - 2017 PDFAzhar JavaidÎncă nu există evaluări

- Business Administration Css NotesDocument14 paginiBusiness Administration Css NotesAnwar Khan100% (1)

- Ogdcl InternshipDocument73 paginiOgdcl InternshipMuhammad Aslam SaberÎncă nu există evaluări

- Auriga Group of Chemicals: 33-KM Multan RoadDocument9 paginiAuriga Group of Chemicals: 33-KM Multan RoadTahir SaeedÎncă nu există evaluări

- Fertilizer Industry of PakistanDocument23 paginiFertilizer Industry of PakistanShahzaib RazaÎncă nu există evaluări

- BYCO ReportDocument17 paginiBYCO ReportAliRashidÎncă nu există evaluări

- OGDC Annual ReportDocument67 paginiOGDC Annual Reporttanveeraddozai112667% (3)

- Report On OGDCLDocument47 paginiReport On OGDCLsyed Muntazir naqvi100% (7)

- Khalid Mehmood Anjum Internship Report MBA UOLDocument110 paginiKhalid Mehmood Anjum Internship Report MBA UOLTaimur FazilÎncă nu există evaluări

- Notes LUMS Governing With Shackles - Selecting PESCO CEODocument4 paginiNotes LUMS Governing With Shackles - Selecting PESCO CEOAAFurqanÎncă nu există evaluări

- Sui Gas Internship ReportDocument45 paginiSui Gas Internship ReportALi Khan100% (1)

- Sui Southern Gas Company Limited Annual Report 2004Document0 paginiSui Southern Gas Company Limited Annual Report 2004InaamÎncă nu există evaluări

- Internship Report at FFCDocument93 paginiInternship Report at FFCmuhammad irfan100% (8)

- Energy Crisis in Pakistan by Malik Naseem AbbasDocument91 paginiEnergy Crisis in Pakistan by Malik Naseem AbbasAfzaal Ashraf100% (1)

- Intrenship Report 2017 OGDCL PakistanDocument56 paginiIntrenship Report 2017 OGDCL PakistanIsrarAhmadMarwatÎncă nu există evaluări

- SWOT Analysis of China Pakistan Economic Corridor (CPEC) : StrengthsDocument3 paginiSWOT Analysis of China Pakistan Economic Corridor (CPEC) : StrengthsZawar Hussain100% (1)

- FFBL Internship ReportDocument38 paginiFFBL Internship Reportجہانزیب عباس100% (1)

- PTCLDocument35 paginiPTCLMuhammad Ashraf Khan100% (1)

- Details of LPG Marketing CompaniesDocument7 paginiDetails of LPG Marketing Companiespakistan1stÎncă nu există evaluări

- A Project Report On PSMCDocument8 paginiA Project Report On PSMCWazeeer AhmadÎncă nu există evaluări

- OgdclDocument9 paginiOgdclSun RayÎncă nu există evaluări

- Assignment Topic: Cpec Chaina Pakistan Economic Corridor: BackgroundDocument21 paginiAssignment Topic: Cpec Chaina Pakistan Economic Corridor: BackgroundAbdul MunemÎncă nu există evaluări

- China Pakistan Economic Corridor (CPEC) and Small Medium Enterprises (SMEs) of PakistanDocument12 paginiChina Pakistan Economic Corridor (CPEC) and Small Medium Enterprises (SMEs) of PakistanTayyaub khalidÎncă nu există evaluări

- Corporate Finance Project On Descon in PakistanDocument43 paginiCorporate Finance Project On Descon in PakistanuzmazainabÎncă nu există evaluări

- Islam Dor e Jadid Ka Khaliq.Document122 paginiIslam Dor e Jadid Ka Khaliq.Nakh145 RisayÎncă nu există evaluări

- Report On CpecDocument22 paginiReport On CpecHamza ShabbirÎncă nu există evaluări

- AKRSP Energy Mapping and Socio-Economic Impact Assessment of Access To Electricity in Villages of Gilgit, Baltistan and ChitralDocument65 paginiAKRSP Energy Mapping and Socio-Economic Impact Assessment of Access To Electricity in Villages of Gilgit, Baltistan and Chitralkarishma ghaziÎncă nu există evaluări

- Parco Internship ReportDocument17 paginiParco Internship Reportvj kumarÎncă nu există evaluări

- Final Project: International Islamic University IslamabadDocument24 paginiFinal Project: International Islamic University IslamabadSohaibDanishÎncă nu există evaluări

- Causes of Poverty in Pakistan Presentation (HILAL)Document22 paginiCauses of Poverty in Pakistan Presentation (HILAL)S.M.HILAL67% (3)

- Oil Distribution (Sodr)Document5 paginiOil Distribution (Sodr)Vikas HashmiÎncă nu există evaluări

- Internship Report in PSODocument5 paginiInternship Report in PSOSayyed SofianÎncă nu există evaluări

- Internship Report GikiDocument67 paginiInternship Report GikiMuhammadWaqasAfridi0% (1)

- MNC ReportDocument23 paginiMNC ReportSheriYar KhattakÎncă nu există evaluări

- Afs Report - LuckyDocument18 paginiAfs Report - LuckyMKMikeÎncă nu există evaluări

- Final PARCO Brand AuditDocument24 paginiFinal PARCO Brand AuditŠyȜd UŠmãn AłiÎncă nu există evaluări

- ArlDocument68 paginiArlAtta Ur Rehman100% (1)

- CTC - Inst SlipDocument3 paginiCTC - Inst SlipHaris Ali KhanÎncă nu există evaluări

- Impact of Stress On Employees Job Performance in Business Sector of PakistanDocument5 paginiImpact of Stress On Employees Job Performance in Business Sector of PakistanAqsaQamarÎncă nu există evaluări

- Theeffectsofthephysical Environmentonjob Performance:towards Atheoreticalmodel OfworkspacestressDocument10 paginiTheeffectsofthephysical Environmentonjob Performance:towards Atheoreticalmodel OfworkspacestressHaris Ali KhanÎncă nu există evaluări

- Flex-Time As A Moderator of TheDocument16 paginiFlex-Time As A Moderator of TheHaris Ali KhanÎncă nu există evaluări

- Trafffic JamDocument31 paginiTrafffic JamLee Sum YinÎncă nu există evaluări

- BMtechIrfanMehmood CV and DocumentsDocument15 paginiBMtechIrfanMehmood CV and DocumentsHaris Ali KhanÎncă nu există evaluări

- HR Org ChartDocument1 paginăHR Org ChartHaris Ali KhanÎncă nu există evaluări

- NadeemDocument13 paginiNadeemHaris Ali KhanÎncă nu există evaluări

- CV Sandy HershcovisDocument14 paginiCV Sandy HershcovisHaris Ali KhanÎncă nu există evaluări

- List of Ministries and DivisionsDocument2 paginiList of Ministries and DivisionsHaris Ali KhanÎncă nu există evaluări

- Budget of PunjabDocument70 paginiBudget of PunjabHaris Ali KhanÎncă nu există evaluări

- BMtechIrfanMehmood CV and DocumentsDocument15 paginiBMtechIrfanMehmood CV and DocumentsHaris Ali KhanÎncă nu există evaluări

- NadeemDocument13 paginiNadeemHaris Ali KhanÎncă nu există evaluări

- BbaDocument13 paginiBbaRaghunath ChinnasamyÎncă nu există evaluări

- BMEngr Usman DCMTDocument7 paginiBMEngr Usman DCMTHaris Ali KhanÎncă nu există evaluări

- BMEngr Zulfiqar DCMTDocument24 paginiBMEngr Zulfiqar DCMTHaris Ali KhanÎncă nu există evaluări

- YorkU BrochureDocument8 paginiYorkU BrochureHaris Ali KhanÎncă nu există evaluări

- Post GraduationDocument1 paginăPost GraduationHaris Ali KhanÎncă nu există evaluări

- Job 7978832 260833 SABIDIDocument5 paginiJob 7978832 260833 SABIDIHaris Ali KhanÎncă nu există evaluări

- Canada Plagiarism ApplicationsDocument2 paginiCanada Plagiarism ApplicationsHaris Ali KhanÎncă nu există evaluări

- Transcript MBADocument1 paginăTranscript MBAHaris Ali KhanÎncă nu există evaluări

- CV MalikNaseemAbbasDocument4 paginiCV MalikNaseemAbbasHaris Ali KhanÎncă nu există evaluări

- Public Sector in ResearchDocument7 paginiPublic Sector in ResearchHaris Ali KhanÎncă nu există evaluări

- The Public SectorDocument12 paginiThe Public SectorHaris Ali KhanÎncă nu există evaluări

- HRM in MultinationalDocument8 paginiHRM in MultinationalHaris Ali KhanÎncă nu există evaluări

- 03-Motivation and Employees' Performance in The Public PDFDocument10 pagini03-Motivation and Employees' Performance in The Public PDFHaris Ali KhanÎncă nu există evaluări

- Public Sector ResearchDocument14 paginiPublic Sector ResearchHaris Ali KhanÎncă nu există evaluări

- Public SectorDocument10 paginiPublic SectorHaris Ali KhanÎncă nu există evaluări

- Research of Public SectorDocument26 paginiResearch of Public SectorHaris Ali KhanÎncă nu există evaluări

- Tracking Data Flow Through Receipts Tables 9-11-13Document68 paginiTracking Data Flow Through Receipts Tables 9-11-13Sudheer SanagalaÎncă nu există evaluări

- Addenda ChryslerDocument6 paginiAddenda ChryslerJose Luis Jimenez Cid0% (1)

- Ajio FL0116687730 1564208470689Document1 paginăAjio FL0116687730 1564208470689sravanÎncă nu există evaluări

- Purchasing Partner DeterminationDocument13 paginiPurchasing Partner DeterminationMalith Tharaka Perera100% (3)

- Sap T Code List IsuDocument30 paginiSap T Code List IsuShailesh Tatkare100% (2)

- Triumph Gate Technologies: 3 Floor, Nagasuri Plaza, Bank of India, AmeerpetDocument6 paginiTriumph Gate Technologies: 3 Floor, Nagasuri Plaza, Bank of India, AmeerpetmayuriÎncă nu există evaluări

- Application SummaryDocument14 paginiApplication SummaryIradukunda MarcelÎncă nu există evaluări

- Fuck OffDocument3 paginiFuck OffAnurag RanaÎncă nu există evaluări

- Mukon Constructions Pvt. LTD.: 1 Manpower Supply For The Month of Aug. 2019 9985 Lum Sum - 16,90,884Document1 paginăMukon Constructions Pvt. LTD.: 1 Manpower Supply For The Month of Aug. 2019 9985 Lum Sum - 16,90,884lucky dudeÎncă nu există evaluări

- Docslide - Us General Conditions of 1994 Fidic SubcontractDocument23 paginiDocslide - Us General Conditions of 1994 Fidic SubcontractzazaÎncă nu există evaluări

- Viewtenddoc AspDocument87 paginiViewtenddoc AspvigneshÎncă nu există evaluări

- Card Summary-Sales Tax ActDocument4 paginiCard Summary-Sales Tax ActM.Faizan ToorÎncă nu există evaluări

- SAmple Temp AgreementDocument11 paginiSAmple Temp AgreementDeepthi BadriÎncă nu există evaluări

- Third Party SalesDocument4 paginiThird Party SalesVicky KumarÎncă nu există evaluări

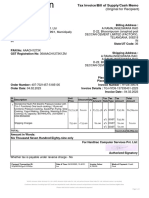

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 paginăTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)sandesh badawaneÎncă nu există evaluări

- Clause 13: Variations and AssignmentsDocument27 paginiClause 13: Variations and AssignmentsJane PanganibanÎncă nu există evaluări

- IESCO - SAP - ERP - FI - TD Fiori - AP 01Document47 paginiIESCO - SAP - ERP - FI - TD Fiori - AP 01Fahim JanÎncă nu există evaluări

- InvoiceDocument1 paginăInvoiceRamalingeswaraRao AmpalamÎncă nu există evaluări

- Thank You! Your Payment Was Successful.: Invoice #28209622Document1 paginăThank You! Your Payment Was Successful.: Invoice #28209622navin_netÎncă nu există evaluări

- Chapter 4 - Recording and Summarizing TransactionsDocument56 paginiChapter 4 - Recording and Summarizing Transactionsshemida60% (5)

- SAP AR Dilip SadhDocument90 paginiSAP AR Dilip SadhDilip SadhÎncă nu există evaluări

- Display Document FlowDocument6 paginiDisplay Document FlowzenyahÎncă nu există evaluări

- Valuation With The Moving Average Price: Problems With Stock CoverageDocument6 paginiValuation With The Moving Average Price: Problems With Stock CoverageUday HawaldarÎncă nu există evaluări