S-ar putea să vă placă și

- Deutsche Bank Ag Manila Branch VS CirDocument4 paginiDeutsche Bank Ag Manila Branch VS CirJen DeeÎncă nu există evaluări

- Notice of Assessment 2023 04 11 11 51 12 947361Document4 paginiNotice of Assessment 2023 04 11 11 51 12 947361Amelia D. LopezÎncă nu există evaluări

- G.R. No. 127105. June 25, 1999. Commissioner of Internal Revenue, Petitioner, vs. S.C. Johnson and Son, Inc., and Court of APPEALS, RespondentsDocument5 paginiG.R. No. 127105. June 25, 1999. Commissioner of Internal Revenue, Petitioner, vs. S.C. Johnson and Son, Inc., and Court of APPEALS, RespondentsConcepcion Mallari GarinÎncă nu există evaluări

- Bir 1701Document2 paginiBir 1701RAYNAN MARCELO100% (1)

- CIR Vs SolidbankDocument3 paginiCIR Vs SolidbankJoel MilanÎncă nu există evaluări

- Template With Cover PageDocument5 paginiTemplate With Cover PageChristine MannaÎncă nu există evaluări

- 17 Digital Telecom V BatangasDocument2 pagini17 Digital Telecom V BatangasJesse Nicole SantosÎncă nu există evaluări

- INDIA INCOME TAX - Doble Taxation Avoidance Agreement With UKDocument22 paginiINDIA INCOME TAX - Doble Taxation Avoidance Agreement With UKDr.SagindarÎncă nu există evaluări

- Deutsche Bank Vs CIRDocument2 paginiDeutsche Bank Vs CIRAndrea RioÎncă nu există evaluări

- Tax certificate for Zakhele Luka MathunjwaDocument1 paginăTax certificate for Zakhele Luka MathunjwaZakhele MathunjwaÎncă nu există evaluări

- CIR V SC Johnson and Son and CADocument4 paginiCIR V SC Johnson and Son and CAkenken320Încă nu există evaluări

- GoodDocument1 paginăGoodEntertain with musicÎncă nu există evaluări

- Cases 4-6Document3 paginiCases 4-6Mich PadayaoÎncă nu există evaluări

- Cir v. Pal DigestDocument4 paginiCir v. Pal DigestkathrynmaydevezaÎncă nu există evaluări

- RP-Japan Protocol - 2008Document5 paginiRP-Japan Protocol - 2008Hazel PangandianÎncă nu există evaluări

- PROTOCOL Agreement Between United States and JapanDocument25 paginiPROTOCOL Agreement Between United States and JapanOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Article 10-19 Tax RulesDocument5 paginiArticle 10-19 Tax RulesDewi JumiatiÎncă nu există evaluări

- Philippines - ST - en Law-10-12Document3 paginiPhilippines - ST - en Law-10-12Kindg NiceÎncă nu există evaluări

- Philippines - ST - en Law-19-21Document3 paginiPhilippines - ST - en Law-19-21Kindg NiceÎncă nu există evaluări

- Rp-Japan Tax TreatyDocument7 paginiRp-Japan Tax TreatyPrintet08Încă nu există evaluări

- PROTOCOL Agreement Between Cyprus and PolandDocument7 paginiPROTOCOL Agreement Between Cyprus and PolandOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- DTC Agreement Between Poland and SwitzerlandDocument13 paginiDTC Agreement Between Poland and SwitzerlandOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- (2006) 7 CPT 520 Usefulness of Non-Discrimination Provision in The TreatiesDocument3 pagini(2006) 7 CPT 520 Usefulness of Non-Discrimination Provision in The Treatiessuraj gulipalliÎncă nu există evaluări

- Treaty US Model 2016 - 1Document70 paginiTreaty US Model 2016 - 1Christian Louie LimÎncă nu există evaluări

- Art 12 BDocument13 paginiArt 12 BJORGEÎncă nu există evaluări

- RMC 46-02Document2 paginiRMC 46-02saintkarriÎncă nu există evaluări

- Philippines - ST - en Law-7-9Document3 paginiPhilippines - ST - en Law-7-9Kindg NiceÎncă nu există evaluări

- Pertemuan 9 Perbandingan Tax Treaty Dalam Model Oecd, Un Dan Model IndonesiaDocument41 paginiPertemuan 9 Perbandingan Tax Treaty Dalam Model Oecd, Un Dan Model IndonesiaWindu ShabrielliaÎncă nu există evaluări

- DTC Agreement Between Barbados and ChinaDocument8 paginiDTC Agreement Between Barbados and ChinaOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- DTC Agreement Between United States and MaltaDocument39 paginiDTC Agreement Between United States and MaltaOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- DTC Agreement Between Netherlands and TurkeyDocument29 paginiDTC Agreement Between Netherlands and TurkeyOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Philippines - ST - en Law-13-15Document3 paginiPhilippines - ST - en Law-13-15Kindg NiceÎncă nu există evaluări

- DTC Agreement Between Greece and SwitzerlandDocument8 paginiDTC Agreement Between Greece and SwitzerlandOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- DTAADocument7 paginiDTAAA PLÎncă nu există evaluări

- DTC Agreement Between Papua New Guinea and New ZealandDocument40 paginiDTC Agreement Between Papua New Guinea and New ZealandOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Multi-Tiered Interest Rates: Power of The Monetary Board Under Section 1-A Paragraph 2Document23 paginiMulti-Tiered Interest Rates: Power of The Monetary Board Under Section 1-A Paragraph 2DANICA FLORESÎncă nu există evaluări

- DTC Agreement Between Netherlands and BarbadosDocument10 paginiDTC Agreement Between Netherlands and BarbadosOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Indonesia - Belanda (Netherlands)Document12 paginiIndonesia - Belanda (Netherlands)natashaÎncă nu există evaluări

- Taxation Ii-Reviewer PDFDocument31 paginiTaxation Ii-Reviewer PDFMisc Ellaneous0% (1)

- 64.double Taxation ReliefDocument14 pagini64.double Taxation ReliefMohit MalhotraÎncă nu există evaluări

- Tds Under GSTDocument4 paginiTds Under GSTShaan MithagariÎncă nu există evaluări

- Dtaa India UsaDocument38 paginiDtaa India UsaNilesh KulkarniÎncă nu există evaluări

- 7-Income From PropertyDocument4 pagini7-Income From PropertySumaira AslamÎncă nu există evaluări

- Union of IndiaDocument47 paginiUnion of IndiaayushÎncă nu există evaluări

- CTA CasesDocument177 paginiCTA CasesJade Palace TribezÎncă nu există evaluări

- BLR 2023 TAX LAW ExaminationDocument21 paginiBLR 2023 TAX LAW Examinationfdg7vf8tcwÎncă nu există evaluări

- DTC Agreement Between Zambia and SeychellesDocument31 paginiDTC Agreement Between Zambia and SeychellesOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 paginiCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsÎncă nu există evaluări

- 04 - TanDocument8 pagini04 - TanRundolphJemmuel CouncilÎncă nu există evaluări

- DTC Agreement Between United Arab Emirates and KazakhstanDocument27 paginiDTC Agreement Between United Arab Emirates and KazakhstanOECD: Organisation for Economic Co-operation and DevelopmentÎncă nu există evaluări

- Amendment DirectTax FA2013Document30 paginiAmendment DirectTax FA2013Bharat LuthraÎncă nu există evaluări

- Dec 2 - Tax 1 - TranscriptDocument5 paginiDec 2 - Tax 1 - TranscriptFedencio CostunaÎncă nu există evaluări

- Treaty UK Notes 7 24 2001Document10 paginiTreaty UK Notes 7 24 2001ada.sezginÎncă nu există evaluări

- United Arab Emirates: Notification G.S.R. No. 710 (E), Dated 18th November, 1993Document24 paginiUnited Arab Emirates: Notification G.S.R. No. 710 (E), Dated 18th November, 1993Parthasarathy P RamaswamiÎncă nu există evaluări

- #9 CIR v. SC JohnsonDocument3 pagini#9 CIR v. SC JohnsonKORINA NGALOYÎncă nu există evaluări

- Adopted Regulation of The State TreasurerDocument8 paginiAdopted Regulation of The State TreasurerRidalyn AdrenalynÎncă nu există evaluări

- Question and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofDocument6 paginiQuestion and Answers Ques. No.1) Write Notes On: A.) Taxability of Deep Discount Bond - A Recent Move of The Central Board ofAnamika VatsaÎncă nu există evaluări

- 40% of The Financial BenefitsDocument17 pagini40% of The Financial Benefitsallysa maicaÎncă nu există evaluări

- Israel Phil TreatyDocument4 paginiIsrael Phil TreatyGrace TrinidadÎncă nu există evaluări

- PerquisitesDocument6 paginiPerquisitesArgha DeySarkarÎncă nu există evaluări

- American Chicle Co. v. United States, 316 U.S. 450 (1942)Document4 paginiAmerican Chicle Co. v. United States, 316 U.S. 450 (1942)Scribd Government DocsÎncă nu există evaluări

- Revenue Memorandum Circular 69-03Document3 paginiRevenue Memorandum Circular 69-03Jeng PionÎncă nu există evaluări

- Taxation of Corporate Dividends and Stock DividendsDocument16 paginiTaxation of Corporate Dividends and Stock DividendsGeralyn GabrielÎncă nu există evaluări

- Project (MMP) Dan Model Pembelajaran Think Talk WriteDocument18 paginiProject (MMP) Dan Model Pembelajaran Think Talk WriteEko SiswantoÎncă nu există evaluări

- Artikel Ilmiah 08310599Document22 paginiArtikel Ilmiah 08310599Eko SiswantoÎncă nu există evaluări

- Ulangan Kelas X Kartur 2012 - 2013Document1 paginăUlangan Kelas X Kartur 2012 - 2013Eko SiswantoÎncă nu există evaluări

- BRSL EnglandDocument1 paginăBRSL EnglandEko SiswantoÎncă nu există evaluări

- Latihan Ulangan Logaritma Kelasa XDocument1 paginăLatihan Ulangan Logaritma Kelasa XEko SiswantoÎncă nu există evaluări

- BRSL EnglandDocument1 paginăBRSL EnglandEko SiswantoÎncă nu există evaluări

- 1Document1 pagină1Eko SiswantoÎncă nu există evaluări

- Sistem Informasi Akuntansi Silabi Sep 2013Document8 paginiSistem Informasi Akuntansi Silabi Sep 2013Eko SiswantoÎncă nu există evaluări

- Citizens National Bank Pay StubDocument1 paginăCitizens National Bank Pay StubsherrieÎncă nu există evaluări

- Promoted Team Leader HR DeputationDocument2 paginiPromoted Team Leader HR DeputationHimanshu AlighÎncă nu există evaluări

- FNF Settlement Guidelines and Ways To Reach Finance: Computation As Per Input F&F Calculation ParametersDocument1 paginăFNF Settlement Guidelines and Ways To Reach Finance: Computation As Per Input F&F Calculation ParametersVivekMedaramitlaÎncă nu există evaluări

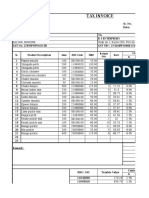

- Tax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyDocument4 paginiTax Invoice: % Rate CGST Sr. Product Description Gms HSN Code MRP Return QtyJai GaneshÎncă nu există evaluări

- Invoice for Waste Paper SaleDocument1 paginăInvoice for Waste Paper SaleJaffa TuppuÎncă nu există evaluări

- Tax.3301-3 Accounting Methods and PeriodsDocument2 paginiTax.3301-3 Accounting Methods and PeriodsDena Heart OrenioÎncă nu există evaluări

- Children Education Allowance Form WordDocument2 paginiChildren Education Allowance Form WordTechno WhatÎncă nu există evaluări

- RMC No. 46-2021Document1 paginăRMC No. 46-2021Joel SyÎncă nu există evaluări

- BIR Form No. 2322 Certificate of DonationDocument2 paginiBIR Form No. 2322 Certificate of DonationGuile Gabriel AlogÎncă nu există evaluări

- Business and Transfer Taxation - T or FDocument3 paginiBusiness and Transfer Taxation - T or FEuli Mae SomeraÎncă nu există evaluări

- GST InvoiceDocument1 paginăGST Invoicemrutyunjaya1Încă nu există evaluări

- Diversion of IncomeDocument11 paginiDiversion of IncomeSrivathsan NambiraghavanÎncă nu există evaluări

- Moredo, Eloisa Joy R Payroll Workshop: Alaras, Arla Gabrielle (A0012)Document15 paginiMoredo, Eloisa Joy R Payroll Workshop: Alaras, Arla Gabrielle (A0012)Eloisa Joy MoredoÎncă nu există evaluări

- 101 Amendment of Indian Constitution 58Document3 pagini101 Amendment of Indian Constitution 58Nageswara Rao VemulaÎncă nu există evaluări

- I 8802Document13 paginiI 8802ccshanÎncă nu există evaluări

- GST TEST - 2 DEC 22 and JUNE 23 Batch Without AnswerDocument6 paginiGST TEST - 2 DEC 22 and JUNE 23 Batch Without AnswerSanjana KashyapÎncă nu există evaluări

- E TaxDocument1 paginăE TaxTemesgenÎncă nu există evaluări

- DM Realty Developers Private LimitedDocument1 paginăDM Realty Developers Private LimitedsimplepannuÎncă nu există evaluări

- Payslip: HJC Design and ConstructionDocument6 paginiPayslip: HJC Design and ConstructionHazel Joy CastilloÎncă nu există evaluări

- RajeshDocument1 paginăRajeshSiva RamanÎncă nu există evaluări

- CREATE Zalamea Briefing + RRsDocument76 paginiCREATE Zalamea Briefing + RRsGerryÎncă nu există evaluări

- GST RegistrationDocument4 paginiGST RegistrationUnique Trans SystemÎncă nu există evaluări

- Problem 1 Communal PropertiesDocument11 paginiProblem 1 Communal PropertiesJuanaÎncă nu există evaluări

- Itr Acknowledgement FormatDocument1 paginăItr Acknowledgement FormatDinesh RajputÎncă nu există evaluări

- Solved For Many Years MR K The President of KJ IncDocument1 paginăSolved For Many Years MR K The President of KJ IncAnbu jaromiaÎncă nu există evaluări