S-ar putea să vă placă și

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDe la EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsÎncă nu există evaluări

- FI and CO OverviewDocument22 paginiFI and CO OverviewSPSINGH RathourÎncă nu există evaluări

- Order To Cash BPO A Complete Guide - 2020 EditionDe la EverandOrder To Cash BPO A Complete Guide - 2020 EditionÎncă nu există evaluări

- Final Version of IFRS 9Document17 paginiFinal Version of IFRS 9Sunil GÎncă nu există evaluări

- Task Sequence Process for Production Order ManagementDocument2 paginiTask Sequence Process for Production Order Managementmadhub_17Încă nu există evaluări

- Implementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesDe la EverandImplementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesÎncă nu există evaluări

- Chapter 4Document21 paginiChapter 4api-294576901Încă nu există evaluări

- Fixed Assets Management A Complete Guide - 2020 EditionDe la EverandFixed Assets Management A Complete Guide - 2020 EditionÎncă nu există evaluări

- CO - 1KEK - JPN - Transfer Profit Centers To Receivables, PayablesDocument15 paginiCO - 1KEK - JPN - Transfer Profit Centers To Receivables, PayablesnguyencaohuyÎncă nu există evaluări

- FC 10.0 Starter Kit For IFRS Configuration DesignDocument67 paginiFC 10.0 Starter Kit For IFRS Configuration DesignKsuÎncă nu există evaluări

- FISD IntegrationDocument21 paginiFISD IntegrationshekarÎncă nu există evaluări

- FIEUT007CL - 02 Year End ClosingDocument7 paginiFIEUT007CL - 02 Year End ClosingMajut AlenkÎncă nu există evaluări

- PCA Actual Assessment ProcessDocument10 paginiPCA Actual Assessment ProcessrajdeeppawarÎncă nu există evaluări

- SAP FI Important TcodeDocument4 paginiSAP FI Important TcodesalhumÎncă nu există evaluări

- Accruals and deferrals explained with phone bill exampleDocument3 paginiAccruals and deferrals explained with phone bill exampleArchana KoreÎncă nu există evaluări

- Valuated Project StockDocument4 paginiValuated Project StockAshley StutteÎncă nu există evaluări

- Report Painter1Document15 paginiReport Painter1kumarkrishna.grÎncă nu există evaluări

- ABST2 Preparation For Year-End Closing - Account ReconcilatiDocument13 paginiABST2 Preparation For Year-End Closing - Account ReconcilatiOkikiri Omeiza RabiuÎncă nu există evaluări

- Budget Management System User ManualDocument60 paginiBudget Management System User ManualChelle P. TenorioÎncă nu există evaluări

- Integration of BPS Layouts With CRM Planning PDFDocument18 paginiIntegration of BPS Layouts With CRM Planning PDFAntonioLeitesÎncă nu există evaluări

- SAP Project Systems PS Study Material 137 PagesDocument9 paginiSAP Project Systems PS Study Material 137 Pagespbhat83Încă nu există evaluări

- Investment Management in PM: Test Script SAP S/4HANA 1709 June 2018Document50 paginiInvestment Management in PM: Test Script SAP S/4HANA 1709 June 2018Naveen Reddy KasarlaÎncă nu există evaluări

- FI - Auto Email Notification For Closing Cockpit PDFDocument9 paginiFI - Auto Email Notification For Closing Cockpit PDFHoang Quoc DatÎncă nu există evaluări

- Process Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunDocument2 paginiProcess Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunUppiliappan GopalanÎncă nu există evaluări

- User Training Manual - PS - TP - End User V1.2Document108 paginiUser Training Manual - PS - TP - End User V1.2Rahul KumarÎncă nu există evaluări

- Unit Test ScriptDocument6 paginiUnit Test ScriptDebabrata SahooÎncă nu există evaluări

- Accrual EngineDocument6 paginiAccrual EngineSatya Prasad0% (1)

- Validations in Project SystemDocument17 paginiValidations in Project Systemsamirjoshi73Încă nu există evaluări

- Sap Fico AdvancedDocument14 paginiSap Fico AdvancedsanbharasÎncă nu există evaluări

- Planning and ConsolidationDocument6 paginiPlanning and Consolidationsivachandran_abapÎncă nu există evaluări

- What Are Business Transaction EventsDocument20 paginiWhat Are Business Transaction EventsSaket ShahiÎncă nu există evaluări

- SAP Network Blog How To Configure Valuated Project StockDocument4 paginiSAP Network Blog How To Configure Valuated Project StockSoumen LaruÎncă nu există evaluări

- S - ALR - 87012284 - Financial Statements & Trial BalanceDocument9 paginiS - ALR - 87012284 - Financial Statements & Trial Balancessrinivas64Încă nu există evaluări

- SAP Document TypeDocument2 paginiSAP Document Type8286140035Încă nu există evaluări

- FINANCIALSDocument94 paginiFINANCIALSsumit kishnaniÎncă nu există evaluări

- Budget Carry ForwardDocument2 paginiBudget Carry Forwardpednekar125Încă nu există evaluări

- ESI - 6455 SAP Project System OverviewDocument59 paginiESI - 6455 SAP Project System OverviewJoão de AlmeidaÎncă nu există evaluări

- A. QB Lesson 5Document24 paginiA. QB Lesson 5Shena Mari Trixia GepanaÎncă nu există evaluări

- Important SAP FI and CO TablesDocument4 paginiImportant SAP FI and CO TablesSachin HegdeÎncă nu există evaluări

- BADI's AVAILABLE IN SRM 7.0Document15 paginiBADI's AVAILABLE IN SRM 7.0Karthik BabuÎncă nu există evaluări

- First Steps in SAP FI Configuration - Ann CacciottoliDocument51 paginiFirst Steps in SAP FI Configuration - Ann CacciottoliJose GonzalezÎncă nu există evaluări

- SAP New General Ledger ConfigurationDocument51 paginiSAP New General Ledger ConfigurationParas GourÎncă nu există evaluări

- F 54Document10 paginiF 54madyeid31Încă nu există evaluări

- Use of Variables in A Report Painter ReportDocument11 paginiUse of Variables in A Report Painter Reporttapan92Încă nu există evaluări

- CO Manual CO-PA-04 Report PainterDocument55 paginiCO Manual CO-PA-04 Report PaintergirijadeviÎncă nu există evaluări

- SAP Records ManagementDocument93 paginiSAP Records ManagementVasco MonteiroÎncă nu există evaluări

- FAGL - 104 Transaction PDFDocument2 paginiFAGL - 104 Transaction PDFotaviomendes1Încă nu există evaluări

- 1KEK Transferring Payables - Receivables To PCADocument6 pagini1KEK Transferring Payables - Receivables To PCABrigitta BallaiÎncă nu există evaluări

- POD - Series 1 POD - Series 2: RefurbishmentDocument3 paginiPOD - Series 1 POD - Series 2: RefurbishmentshekarÎncă nu există evaluări

- GL TrainingDocument160 paginiGL TrainingDiwakar Saribala100% (1)

- As Is DocumentDocument37 paginiAs Is DocumentJyotiraditya BanerjeeÎncă nu există evaluări

- F-02 General DoumentDocument9 paginiF-02 General DoumentP RajendraÎncă nu există evaluări

- AA003 - Depreciation: AC605 Profitability AnalysisDocument23 paginiAA003 - Depreciation: AC605 Profitability AnalysisVinay KumarÎncă nu există evaluări

- Configuration and Design Document Funds: Management Page 1 of 146Document146 paginiConfiguration and Design Document Funds: Management Page 1 of 146Reddaveni Nagaraju100% (1)

- Changes To Master Data Asset Accounting - Add Profit Centre - 2013Document5 paginiChanges To Master Data Asset Accounting - Add Profit Centre - 2013Naresh BabuÎncă nu există evaluări

- Accounts Payable: Global Process Management SystemDocument89 paginiAccounts Payable: Global Process Management SystemcybervistaÎncă nu există evaluări

- SAP FICO concepts for financial accounting and controllingDocument7 paginiSAP FICO concepts for financial accounting and controllinganuradha9787Încă nu există evaluări

- FM-GM Troubleshooting TipsDocument37 paginiFM-GM Troubleshooting TipsBAble996Încă nu există evaluări

- Fi GL AuthorizationDocument12 paginiFi GL AuthorizationpysulÎncă nu există evaluări

- Notes For Microsoft WordDocument3 paginiNotes For Microsoft WordKaran KumarÎncă nu există evaluări

- Relationship Between Education and Economic Growth in Pakistan: A Time Series AnalysisDocument6 paginiRelationship Between Education and Economic Growth in Pakistan: A Time Series AnalysisSmile AliÎncă nu există evaluări

- SWOT Analysis of Meezan BankDocument10 paginiSWOT Analysis of Meezan Banksufyanbutt007Încă nu există evaluări

- 1947Document8 pagini1947sufyanbutt007Încă nu există evaluări

- Audit Working Papers What Are Working Papers?Document8 paginiAudit Working Papers What Are Working Papers?sufyanbutt007Încă nu există evaluări

- What Is The Distinction Between Auditing and AccountingDocument1 paginăWhat Is The Distinction Between Auditing and Accountingsufyanbutt007Încă nu există evaluări

- Profit and Loss Account: Net Spread Earned 10,645 10,452 9,366Document8 paginiProfit and Loss Account: Net Spread Earned 10,645 10,452 9,366sufyanbutt007Încă nu există evaluări

- M.a.D's SWOT Analysis of Meezan Bank!Document10 paginiM.a.D's SWOT Analysis of Meezan Bank!Muhammad Ali DanishÎncă nu există evaluări

- Mission and VisionDocument2 paginiMission and VisionmahibuttÎncă nu există evaluări

- Labo Par Uske Kabhi Baddua Nahi HotiDocument2 paginiLabo Par Uske Kabhi Baddua Nahi Hotisufyanbutt007Încă nu există evaluări

- 1947Document8 pagini1947sufyanbutt007Încă nu există evaluări

- 2Document39 pagini2Neeraj TiwariÎncă nu există evaluări

- Profit and Loss Account: Net Spread Earned 10,645 10,452 9,366Document8 paginiProfit and Loss Account: Net Spread Earned 10,645 10,452 9,366sufyanbutt007Încă nu există evaluări

- BCRWDocument56 paginiBCRWsufyanbutt007Încă nu există evaluări

- Labo Par Uske Kabhi Baddua Nahi HotiDocument2 paginiLabo Par Uske Kabhi Baddua Nahi Hotisufyanbutt007Încă nu există evaluări

- Ingredients: Buy These Ingredients NowDocument1 paginăIngredients: Buy These Ingredients Nowsufyanbutt007Încă nu există evaluări

- Muhammad Tayyab Graphics Designer: Address: Muhalla Bakhtay Wala Gala Gulam Muhammad Thaikadar Wala Street # 1 House # 2Document2 paginiMuhammad Tayyab Graphics Designer: Address: Muhalla Bakhtay Wala Gala Gulam Muhammad Thaikadar Wala Street # 1 House # 2sufyanbutt007Încă nu există evaluări

- Business Law Guess Papers 2014 BDocument2 paginiBusiness Law Guess Papers 2014 Bsufyanbutt007Încă nu există evaluări

- ConclusionDocument1 paginăConclusionsufyanbutt007Încă nu există evaluări

- Economics of Pakistan Guess Papers 2014 B.com Part 2 Important QuestionsDocument6 paginiEconomics of Pakistan Guess Papers 2014 B.com Part 2 Important Questionssufyanbutt007Încă nu există evaluări

- Random ExperimentDocument4 paginiRandom Experimentsufyanbutt007Încă nu există evaluări

- Relationship Between Education and Economic Growth in Pakistan: A Time Series AnalysisDocument6 paginiRelationship Between Education and Economic Growth in Pakistan: A Time Series AnalysisSmile AliÎncă nu există evaluări

- Principles of Criminal Investigation CourseDocument4 paginiPrinciples of Criminal Investigation Coursesufyanbutt007Încă nu există evaluări

- Labour EconomicsDocument29 paginiLabour EconomicsAniketh Anchan100% (1)

- Principles of Economics IDocument2 paginiPrinciples of Economics Isufyanbutt007Încă nu există evaluări

- Principles of Banking IDocument2 paginiPrinciples of Banking Isufyanbutt007Încă nu există evaluări

- MBFDocument1 paginăMBFsufyanbutt007Încă nu există evaluări

- Introduction To Business Guess Papers 2014 BDocument1 paginăIntroduction To Business Guess Papers 2014 Bsufyanbutt007Încă nu există evaluări

- MBFDocument1 paginăMBFsufyanbutt007Încă nu există evaluări

- TaleemDocument46 paginiTaleemsufyanbutt007Încă nu există evaluări

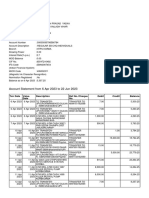

- Account Statement PDFDocument3 paginiAccount Statement PDFPrakashÎncă nu există evaluări

- Toy World CaseDocument9 paginiToy World Casesaurabhsaurs100% (1)

- ch05 PPTDocument23 paginich05 PPThusnainttsÎncă nu există evaluări

- InvoiceDocument1 paginăInvoiceMaryroseÎncă nu există evaluări

- Receipts Orders InvoicesDocument45 paginiReceipts Orders InvoicesAyush53Încă nu există evaluări

- Financial Anylsuis of Icic BankDocument79 paginiFinancial Anylsuis of Icic BankStewart DuraiÎncă nu există evaluări

- PF Withdrawal Form - 19Document2 paginiPF Withdrawal Form - 19Bhavesh ThankiÎncă nu există evaluări

- 4 PC Builtup, Proyektor Jaringan 26 Oktober 2023Document2 pagini4 PC Builtup, Proyektor Jaringan 26 Oktober 2023IT MusaciÎncă nu există evaluări

- Fastag E-Statement: Customer Details Bank DetailsDocument2 paginiFastag E-Statement: Customer Details Bank DetailsSawariya PaintsÎncă nu există evaluări

- WWRPL Oct-19Document12 paginiWWRPL Oct-19Sanjay KumarÎncă nu există evaluări

- Logcat CSC Compare LogDocument943 paginiLogcat CSC Compare LogGustavo Adolfo Fandiño AvilaÎncă nu există evaluări

- Hope You Enjoyed Your Ride!: Your Grab E-ReceiptDocument1 paginăHope You Enjoyed Your Ride!: Your Grab E-ReceiptalexsaputrasÎncă nu există evaluări

- Nentr 6043Document4 paginiNentr 6043wadagrosÎncă nu există evaluări

- CHAPTER 6 - The General Structure of Insurance IndustryDocument18 paginiCHAPTER 6 - The General Structure of Insurance Industryanis abdÎncă nu există evaluări

- Account Balance(s) As at 23 January 2021Document5 paginiAccount Balance(s) As at 23 January 2021seen youÎncă nu există evaluări

- Statement Summary for Aman S SureDocument35 paginiStatement Summary for Aman S SureSudhir SubnisÎncă nu există evaluări

- 12th Computer Applications Chapter 15 To 18 Study Material Tamil Medium PDF DownloadDocument25 pagini12th Computer Applications Chapter 15 To 18 Study Material Tamil Medium PDF Downloadsaoja3Încă nu există evaluări

- Accounting Quiz on Merchandising ConceptsDocument8 paginiAccounting Quiz on Merchandising ConceptsJayson LucenaÎncă nu există evaluări

- Cutco Case StudyDocument3 paginiCutco Case StudyrusfazairaafÎncă nu există evaluări

- GSM/GPRS Modem Wireless ConnectivityDocument2 paginiGSM/GPRS Modem Wireless ConnectivityAaaaÎncă nu există evaluări

- Hotel VoucherDocument2 paginiHotel VoucherViky ArdiÎncă nu există evaluări

- Health Apps - A ToolkitDocument3 paginiHealth Apps - A ToolkitAlexandra WykeÎncă nu există evaluări

- Balance - RisexerDocument1 paginăBalance - RisexerLaser002 RaackÎncă nu există evaluări

- ACCT5001 2022 S2 - Module 1 - Student Lecture SlidesDocument34 paginiACCT5001 2022 S2 - Module 1 - Student Lecture Slideswuzhen102110Încă nu există evaluări

- Home Helpers Home Care - Google SearchDocument1 paginăHome Helpers Home Care - Google Searchrudy.upshawÎncă nu există evaluări

- Wa0064Document5 paginiWa0064Coid CekÎncă nu există evaluări

- Tugas GC 1Document8 paginiTugas GC 13.7 MÎncă nu există evaluări

- Account Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 paginiAccount Statement From 6 Apr 2023 To 22 Jun 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNishant Sagar DewanganÎncă nu există evaluări

- Bba 208Document3 paginiBba 208armaanÎncă nu există evaluări

- Dynamic RoutingDocument23 paginiDynamic RoutingZoheb qureshiÎncă nu există evaluări