S-ar putea să vă placă și

- Proiect Final Sas 1Document108 paginiProiect Final Sas 1Alexandra Iuliana IonÎncă nu există evaluări

- Daily journal entries June 30Document81 paginiDaily journal entries June 30Alexandra Iuliana IonÎncă nu există evaluări

- Analiuza Univariata+matricea de CorelatieDocument91 paginiAnaliuza Univariata+matricea de CorelatieAlexandra Iuliana IonÎncă nu există evaluări

- Armonizare Politica Fiscala UeDocument5 paginiArmonizare Politica Fiscala UeAlexandra Iuliana IonÎncă nu există evaluări

- Monetary Policy and Inflation Targeting: Lars E.O. SvenssonDocument8 paginiMonetary Policy and Inflation Targeting: Lars E.O. SvenssonAlexandra Iuliana IonÎncă nu există evaluări

- BRIC Countries in Comparative Perspective: Kristalina GeorgievaDocument28 paginiBRIC Countries in Comparative Perspective: Kristalina GeorgievaabhisilkÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Bdo BranchesDocument43 paginiBdo BranchesJohn Carlo ChomatogÎncă nu există evaluări

- ConfigGuide AADocument46 paginiConfigGuide AAfungayingorimaÎncă nu există evaluări

- GM - OEM Quick Reference Guide - Dec2016 1 PDFDocument2 paginiGM - OEM Quick Reference Guide - Dec2016 1 PDFSelvaraj Simiyon0% (1)

- Nomination Committee RoleDocument10 paginiNomination Committee RolesusmritiÎncă nu există evaluări

- GDR - Global Depository ReceiptsDocument22 paginiGDR - Global Depository Receiptshahire0% (1)

- Mergers - MotivesDocument17 paginiMergers - MotivesyogeshsherlaÎncă nu există evaluări

- Local Government in The United StatesDocument21 paginiLocal Government in The United StatesAhmed Ali SiddiquiÎncă nu există evaluări

- WorksheetDocument4 paginiWorksheetHumaira NomanÎncă nu există evaluări

- Feedback Form Congress 2014Document4 paginiFeedback Form Congress 2014Siju BoseÎncă nu există evaluări

- Principles of Accounting in New Accounting ModelDocument43 paginiPrinciples of Accounting in New Accounting ModelMudassar Nawaz100% (1)

- Private and Confidential Bank Statement SummaryDocument3 paginiPrivate and Confidential Bank Statement SummaryPromothesh MondalÎncă nu există evaluări

- HOA Meeting MinutesDocument20 paginiHOA Meeting MinutesRachmat SetiajiÎncă nu există evaluări

- INF090I01569 - Franklin India Smaller Cos FundDocument1 paginăINF090I01569 - Franklin India Smaller Cos FundKiran ChilukaÎncă nu există evaluări

- Invoice NoDocument2 paginiInvoice Nodhiec100% (1)

- Jack Welch's Lesson For SuccessDocument7 paginiJack Welch's Lesson For Successhakiki_nÎncă nu există evaluări

- Offshore Shell Games 2014Document56 paginiOffshore Shell Games 2014Global Financial IntegrityÎncă nu există evaluări

- Coll V Batangas Case DigestDocument1 paginăColl V Batangas Case DigestRheaParaskmklkÎncă nu există evaluări

- SA220Document22 paginiSA220Laura D'souza0% (1)

- Challan FormDocument1 paginăChallan FormAhmer KhanÎncă nu există evaluări

- Global Audit Director Controller Worldwide Resume George BayidesDocument2 paginiGlobal Audit Director Controller Worldwide Resume George BayidesGeorgeBayidesÎncă nu există evaluări

- Indian MarketsDocument252 paginiIndian MarketsshivaprasadamÎncă nu există evaluări

- Reliance Mutual Fund-FinalDocument7 paginiReliance Mutual Fund-FinalTamanna Mulchandani100% (1)

- In-House Bank & Payment Factory:: Challenges & OpportunitiesDocument43 paginiIn-House Bank & Payment Factory:: Challenges & OpportunitiesmonaÎncă nu există evaluări

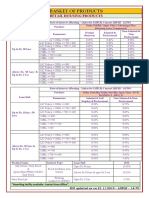

- BASKET OF RETAIL PRODUCTS RATESDocument3 paginiBASKET OF RETAIL PRODUCTS RATESVirendra K VermaÎncă nu există evaluări

- CV - SYaiful Arif WicaksonoDocument2 paginiCV - SYaiful Arif WicaksonoSyaiful Arif WicaksonoÎncă nu există evaluări

- Manufacturer Cylinder Listing August 2018Document27 paginiManufacturer Cylinder Listing August 2018Alvin BernardoÎncă nu există evaluări

- Business License ApplicationDocument2 paginiBusiness License Applicationchern15Încă nu există evaluări

- Invitation To Bid: General GuidelinesDocument26 paginiInvitation To Bid: General GuidelinespandaypiraÎncă nu există evaluări

- Corporate Law ProjectDocument15 paginiCorporate Law Projectbhargavi mishraÎncă nu există evaluări

- 00 - ELECTION CODE - FinalwdtemplateDocument17 pagini00 - ELECTION CODE - FinalwdtemplateDang Joves BojaÎncă nu există evaluări