Documente Academic

Documente Profesional

Documente Cultură

Incidence of Tax

Încărcat de

Anurag SindhalDrepturi de autor

Formate disponibile

Partajați acest document

Partajați sau inserați document

Vi se pare util acest document?

Este necorespunzător acest conținut?

Raportați acest documentDrepturi de autor:

Formate disponibile

Incidence of Tax

Încărcat de

Anurag SindhalDrepturi de autor:

Formate disponibile

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page1

CHAPTER - 15

MISC. RESIDENTIAL STATUS

INCIDENCE OF TAX

Question 1. Need to determine Residential Status?

Total Income of an assessee can not be determined without knowing his residential status in

India because the scope of Total Income and the incidence of tax depends upon the

residential status of the assessee in India.

Total Income will be different in case of a person resident in India and a person non-

resident in India. Resident status is determined in order to compute the Total Income of the

assessee for the relevant previous year.

Indian income : It includes

1. Income earned in India

2. Income received in India

3. Income earned & received in India

Foreign income : It includes income earned and received outside India.

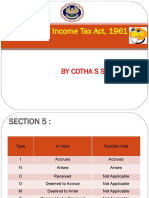

SUMMARISED TABLE OF INCIDENCE OF TAX

Particular of income

Whether taxable

Resident/

ROR

Not-

Ordinarily

Resident

Non

Resident

1. Income received or deemed to be received in

India whether earned in India or elsewhere.

Yes

Yes

Yes

2. Income which accrues or arises or is deemed to

accrue or arise in India during the previous year,

whether received in India or elsewhere

Yes

Yes

Yes

3. Income which accrues or arises outside India and

received outside India from a business totally or

partially controlled from India or a profession set up

in India (Means originally set up in India and later

expanded to other countries)

Yes

Yes

No

4. Income which accrues or arises outside India and

received outside India in the previous year

Yes

No

No

5. Income which accrues or arises outside India and

received outside India during the years preceding the

previous year and remitted to India during the

previous year. [Past untaxed profits]

No

No

No

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page2

INCOME RECEIVED IN INDIA:

Any income received in India is taxable for all categories of assessees viz. ROR, NOR &

NR.

What is taxable is net receipt & not gross receipt i.e. all deductions & reliefs are available.

An income can only be received once. Thus, charge on receipt basis will be attracted when

the income is received for the first time after its accrual.

As per Keshav Mills Ltd. vs CIT (1953)(SC) remittance of an already received amount

does not result in its receipt at that other place.

Thus if an assessee having received an income in a foreign country, say in Japan, remits it

to his family in India, it is not an income received in India, as the income has already been

received in Japan & after its receipt it is being merely remitted to India.

The position will not change if the Assessee having received an income outside India,

himself brings it to India during the previous year.

Now consider a case, when income is not received by assessee in foreign country but by

someone on his behalf say his agent, brother, relative, employee or even bank. If his

agent etc. remits money to him in India after having received it in a foreign country, then in a

way it is being received by assessee for the first time. But it is an established preposition

that such income will be treated as if already received in foreign country and is being

received for the second time and is hence it is not taxable as income received in India.

It is very important to note that such income i.e. earned and received outside during the

previous year is not exempt for all categories of assessees because for ROR it is taxable

even if the income is not received in India.

INCOME DEEMED TO BE RECEIVED IN INDIA: (Section 7)

The following incomes shall be deemed to be received in India in the previous year even in the

absence of actual receipt:

(i) Tax deducted at source is an income in the hands of the payee;

(ii) Interest credited to recognised provident fund, in excess of 9.5% per annum.

(iii) Contribution of the employer to a Recognised Provident Fund in excess of 12% of

the salary of the employee;

(iv) Transferred balance in a Recognised Provident fund to the extent taxable.

(v) The contribution made by the Central Govt. or any other employer to the account of an

employee under a pension scheme referred to in Section 80CCD.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page3

INCOME ACCRUE OR ARISE IN INDIA:

Accrue means due and arise means earned.

In simple language

it means any income

which is earned

and /or

is due in India,

is taxable in India

irrespective of residential status.

INCOME DEEMED TO ACCRUE OR ARISE IN INDIA: SECTION 9

The following incomes shall be deemed to accrue or arise in India:

(1) Section 9(1)(i) Income from a business connection in India.- Where by virtue of

business connection in India, income accrues or arises outside India to any person it is

deemed to accrue or arise in India.

Business connection is very well illustrated by the following examples:

(i) Forming a local subsidiary company to sell the products of the non-resident

parent company; and

(ii) Maintaining a branch office for the sale of goods or transacting other business in

India.

(iii) Erecting a factory in India in which raw produce purchased locally is worked into

semi-finished or finished goods for export abroad.

In the case of a Non-Resident the following shall not be treated as business

connection in India:

(i) In the case of a business of which all the operations are not carried out in India, only

such part of the income as is reasonably attributable to operations carried out in India shall

be treated as deemed to accrue or arise in India.

(ii) Operations confined to purchase of goods in India for purpose of exports;

(iii) Operations confined to collection of news and views for transmission outside India by or

on behalf of Non-resident who is engaged in the business of running news agency or

publishing newspaper, magazines or journals;

(iv) Operations confined to shooting of cinematograph films in India,

if such non-resident is either an individual, who is not a citizen of India,

or a firm which does not have any partner who is a citizen of India or who is a resident in

India,

or a company which does not have any shareholder who is a citizen of India or is

resident in India.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page4

BUSINESS CONNECTION It includes a profession connection.

Business activity carried through following agents of non resident is covered

(a) Concluding agent the agent who concludes contract on behalf of the non resident.

However, agents who only purchase goods for the non resident are not covered.

(b) Stocking agent the one who maintains stock of goods in India and also does delivery

on behalf of non resident

(c) Indenting agent the one who secures orders mainly on behalf of non resident.

INDEPENDENT BROKERS / AGENTS ARE EXCLUDED

The business connection, shall not include cases

where the non-resident carries on business

through a broker, general commission agent or any other agent

of an independent status,

provided that

such a person is acting

in the ordinary course of his business.

Where a broker, general commission agent or any other agent

works (mainly or wholly)

on behalf of a non-resident

or other non-residents under the same management,

he shall not be deemed to be

a broker, general commission agent or an agent

of an independent status.

(2) Section 9(1)(i) Income from any property, asset or source of income situated in India:

Income through or from property in India is deemed to accrue or arise in India.

For instance, the house property or machinery or furniture, situated in India, is hired

under an agreement, which makes the hire/rent payable outside India.

It is an income deemed to accrue or arise in India as the property is situated in India.

The term assets here include intangible assets like patents, copyrights etc

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page5

(3) Section 9(1)(i) - Income from the transfer of any capital asset situated in India:

Any capital gain from the transfer of a capital asset, situated in India, is deemed to

accrue or arise in India. Shares/ securities of Indian companies are Indian capital assets

for this purpose.

(4) Section 9(1)(ii) - Income under the head Salaries- Income of a non-resident which falls

under the head salaries is deemed to accrue or arise in India if it is earned in India.

For this purpose income payable for services rendered in India is regarded as income earned

in India.

Leave encashments / pensions received by a non-resident in respect of services rendered in

India is taxable in India.

(5) Section 9(1)(iii) - Income under salary head payable to a citizen of India abroad by the

government:

It is applicable to government employees who are citizens of India and are posted

abroad.

They render the services outside India and they may also be paid outside India.

But still salary is taxable by virtue of this provision.

It is important to note that by virtue of Section 10(7), all allowances and perquisites

received by such an employee is exempt in India.

(6) Section 9(1)(iv) - Dividend paid by an Indian company outside India.:-

Any dividend paid by an Indian company outside India is deemed to accrue or arise in India.

As per latest provisions, such dividend is exempt u/s 10(34) except u/s 2(22)(e).

(7) Income by way of interest, royalty and technical fees [Sec.9(1) (v)/(vi)/(vii)]- These are

deemed to accrue or arise in India in the following cases

Rule 1 When received from Government Interest royalty or technical fees received from

the Central Government/any State Government, is deemed to accrue or arise in India.

Rule 2 When received from a person resident in India Interest, royalty or technical fees

received from a resident person, is deemed to accrue or arise in India in the hands of recipient.

However, this rule is not applicable in the following cases

a. If borrowed money is utilized by the payer for carrying on a business/profession outside

India or for earning any income outside India; or

b. Payment of royalty/technical fees pertains to a business/profession carried on by the

payer outside India or earning any income outside India.

Rule 3 When received from a non-resident Interest, royalty or technical fees received

from a non-resident, is deemed to accrue or arise in India in the hands of recipient, in the

following cases

a. Borrowed money is utilized by the payer for carrying on a business/profession in India;

or

b. Payment of royalty/technical fees pertains to a business/profession carried on by the

payer in India or earning any income in India.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page6

Provision illustrated A is a non-resident in India. Only Indian income is taxable in the hands

of A in India. During the previous year 2012-13, he receives interest on different dates as given

below. In all these cases, interest is received outside India. If in these cases, interest accrues or

arises in India, then it will be Indian income and taxable in India. Conversely, if in these cases,

interest does not deem to accrue or arise in India, it will become foreign income which will not

be taxable in the hands of A, who is non-resident

Date Nature of interest received by A Whether

deemed to

accrue or

arise in India

April 19, 2012 Rs.8,00,000 is received from the Government of Gujrat Yes

May 11, 2012 Rs.6,00,000 is received from X Ltd. (resident in India)

and X Ltd. has utilized the capital borrowed from A for

carrying on business or profession outside India or

earning any income outside India

Yes

May 22, 2012 Rs.3,00,000 is received from P Ltd. (resident in India)

and P Ltd. has utilized the capital borrowed from A for

carrying o business or profession in India or earning any

income in India

Yes

June 19, 2012 Rs.5,00,000 is received from Q Ltd. (non-resident in

India) and Q Ltd. has utilized the capital borrowed from

A for carrying on business or profession in India

Yes

June 23, 2012 Rs.4,00,000 is received from R Ltd. (non-resident in

India) and R Ltd. has utilized the capital borrowed from A

for carrying on business or profession outside India or

earning any income outside India

No

Definition of royalty [Explanation to Section 9(1)(vi)]

Royalty has been defined as the consideration for

1. The transfer of all or any rights in respect of a patent, invention, model, design, secret

formula or process or trade mark etc.

2. The imparting of any information covering the working of the use of a patent,

invention, model, design, secret formula or process or trade mark etc.

3. The use of any patent, invention, model, design, secret formula, process or trademark

etc.

4. The imparting of any information regarding technical, industrial, commercial or

scientific knowledge or skill.

5. The right to use any industrial, commercial or scientific equipment.

6. The transfer of all or any rights in respect of any copyright, literary artistic or scientific

work

7. The transfer of all or any right for use of a computer software.

8. The rendering of services in connection with any of the above activities.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page7

Royalty includes any lumpsum consideration but excludes consideration, which is covered by

the head capital gains.

Definition of fees for technical services Explanation to Section 9(1)(vii)

It means any consideration, including any lump sum consideration, for the rendering of any

managerial, technical or consultancy services

Excludes consideration for any construction, assemble, mining or like project undertaken by the

recipient.

Also excludes consideration taxable under the head salaries.

PRACTICE QUESTIONS

Question 2. For the assessment year 2013-14, NG (whose previous year is 2012-13) receives

the following incomes :

Royalty earned in India but received on May 8, 2012 in Karachi: Rs.80,000 ; dividend from a

foreign company received in Lahore on July 9, 2012 : Rs. 50,000 ; share of profit of a business

situated in Nepal received in Dhaka on June 10, 2012, but controlled from India : Rs. 40,000 ;

rent of 2012-13 of a house property situated in Dhaka and received there on December 31,

2012 : Rs. 1,65,000 (ignore standard deduction); Determine the gross total income of NG for the

assessment year 2013-14 if he is (a) non-resident, (b) resident but not ordinarily resident, and

(c) resident and ordinarily resident.

Question 3. NG, a foreign national furnishes the following particulars of his income relevant for

the previous year 2012-13 :

Profit on sale of asset at Dubai (40% is received in India)

Profit on sale of plant at Delhi (one half is received in Dubai)

Salary from an Indian company received in London (70% is paid for rendering

service in India)

Interest on USA Development Bonds (entire amount is received in New York)

Income from property in London received there

Income from business in Sri Lanka received there, half of which is used for meeting

education expenses of NGs son in Sri Lanka and remaining amount is later on

remitted to India

Dividend received in London on July 26, 2012 from a company registered in India but

mainly operating in USA

Profit from a business in Agra managed from India

Rental income from a property in Dhaka deposited by the tenant in a foreign branch

of an Indian bank operating there (ignore standard deduction)

Gift in foreign currency (one-third of which is received in India and remaining amount

is used for meeting education expenses of NGs son in Sri Lanka)

1,00,000

2,00,000

50,000

1,40,000

2,30,000

4,25,000

30,000

40,000

60,000

3,00,000

Determine gross total income of NG for the assessment year 2013-14, if he is : (a) non-resident,

(b) resident but not ordinarily resident ; and (c) resident and ordinarily resident

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page8

Question 4. Discuss whether the following incomes are taxable or not in India

1. A non-resident purchases goods from India and sells these goods abroad.

2. A non-resident is engaged in the business of publication of a magazine from Karachi.

Some of the news published in the magazine are collected from India.

3. NG Ltd., a non-resident foreign company, is engaged in the business of shooting a

cinematography film in India. The firm after its completion is sold to another non-resident

outside India. None of the shareholders of NG Ltd. is an Indian citizen or resident in

India.

4. A non-resident owns a commercial building in Surat, which is transferred to another non-

resident outside India. The consideration is payable in a foreign currency outside India.

5. A non-resident owns a residential house in Noida, which is given on rent to a foreign

embassy. Rent is, however, payable outside India in a foreign currency.

6. Interest on loan is paid by the Government of India to a non-resident outside India.

7. N Ltd. a non-resident gets royalty from G Ltd. a non-resident outside India. Royalty is,

however payable by G Ltd. In relation to a business of manufacturing carried on by it

outside India.

8. N Ltd., a non-resident gets interest from G Ltd., an Indian company, outside India. The

capital was borrowed by G Ltd. for the purpose of a business carried on by it outside

India.

9. N, a non-resident Indian, is presently appointed by the Government of India in its

embassy at Sri Lanka. Salary for rendering service is paid to him in a foreign currency

outside India.

10. N, a non-resident Indian, is presently appointed by an Indian company in its foreign

branch at Dhaka. Salary is paid to him outside India in a foreign currency.

Question 5. NG furnishes the following particulars of his income earned during the previous

year relevant to the assessment year 2013 14:

Interest on UK Development Bonds (60% is received in India)

Income from agriculture in Bangladesh, received there but later on Rs. 40,000 is

remitted to India

Income from property at Australia received outside India

Income earned from business in Lahore which is controlled from Delhi (Rs. 1,50,000

is received in India)

Dividend paid by a foreign company but received in India on June 10, 2012

Past untaxed profit of 2008-09 brought to India in 2012-13

Profit from a business in Patiala and managed from outside India

Profits on sale of building in India but received in Australia

Pension from a former employer in India, received in Sri Lanka (net of standard

deduction)

Gift in foreign currency from a relative received in India

80,000

1,00,000

60,000

2,00,000

5,000

10,00,000

8,20,000

14,00,000

70,000

90,000

Find out the gross total income of NG, if he is (i) resident and ordinarily resident in India, (ii)

resident but not ordinarily resident in India, or (iii) non-resident in India for the assessment year

2013-14.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page9

Question from Study Module

Question 6. Determine the taxability of the following incomes in the hands of a resident and

ordinarily resident, resident but not ordinarily resident, and non-resident for the A.Y. 2013-14:

Particulars Amount

(Rs.)

Interest on UK Development Bonds, 50% of interest received in India

Income from a business in Chennai (50% is received in India)

Profits on sale of shares of an Indian company received in London

Dividend from British company received in London

Profits on sale of plant at Germany 50% of profits are received in India

Income earned from business in Germany which is controlled from Delhi

(Rs.40,000 is received in India)

Profits from business in Delhi but managed entirely from London

Rent from property in London deposited in a Indian Bank at London,

brought to India (Ignore std. deduction)

Interest for debentures in an Indian company received in London

Fees for technical services rendered in India but received in London

Profits from a business in Bombay managed from London

Pension for services rendered in Indi abut received in Burma

Income from property situated in Pakistan received there

Past foreign untaxed income brought to India during the previous year

Income from agricultural land in Nepal received there and then brought

to India

Income from profession in Kenya which was set up in India, received

there but spent in India

Gift received on the occasion of his wedding

Interest on saving bank deposit in State Bank of India

Income from a business in Russia, controlled from Russia

Dividend from Reliance Petroleum Limited, an Indian Company

Agricultural income from a land in Rajasthan

10,000

20,000

20,000

5,000

40,000

70,000

15,000

50,000

12,000

8,000

26,000

4,000

16,000

5,000

18,000

5,000

20,000

10,000

20,000

5,000

15,000

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page10

EXAMINATION QUESTIONS

PCC MAY - 2012

Question 7 (12 Marks)

Mr. Ramesh & Mr. Suresh are brothers and they earned the following incomes during the

financial year 2012-13. Mr. Ramesh settled in Canada in the year 1996 and Mr. Suresh settled

in Delhi. Compute the total income for the assessment year 2013-14

Sl.

No.

Particulars Mr. Ramesh Mr. Suresh

1. Interest on Canada Development Bond, (only 50% of

interest received in India)

35,000 40,000

2. Dividend from British company received in London 28,000 20,000

3. Profit from a business in Nagpur, but managed directly

from London

1,00,000 1,40,000

4. Short term capital gain on sale of shares of an Indian

company received in India

60,000 90,000

5. Income from a business in Chennai 80,000 70,000

6. Fees for technical services rendered in India, but

received in Canada

1,00,000 -----

7. Interest on fixed bank deposit in UCO Bank, Delhi 7,000 12,000

8. Agricultural income from a land situated in Andhra

Pradesh

55,000 45,000

9. Income under the head house property at Bhopal 1,00,000 60,000

Question 8. (4 Marks)

Discuss the correctness or otherwise of the statement Income deemed to accrue or arise in

India to a non-resident by way of interest, royalty and fees for technical services is to be taxed

irrespective of territorial nexus.

PCC NOV - 2011

Question 9. (5 Marks)

Mr. David a Government employee serving in the Ministry of External Affairs left India for the

first time on 31.03.2012 due to his transfer of high Commission of Canada. He did not visit any

time during previous year 2012-13. He has received the following income for the Financial Year

2012-13.

Rs.

(i) Salary 5,00,000

(ii) Interest on fixed deposit from bank in India 1,00,000

(iii) Income from agriculture in Pakistan 2,00,000

(iv) Income from house property in Pakistan 2,50,000

Compute his gross total income for Assessment Year 2013-14.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page11

IPCC MAY - 2011

Question 10. (4 Marks)

Miss Vivitha paid a sum of 5000 USD to Mr. Kulasekhara, a management consultant practicing

in Colombo, specializing in project financing. The payment was made in Colombo. Mr.

Kulasekhara is a non-resident. The consultancy related to a project in India with possible

Ceylonese collaboration. Is this payment chargeable to tax in India in the hands of Mr.

Kulasekhara, since the services were used in India?

IPCC MAY 2010

Question 11. From the following particulars of income furnished by Mr A pertaining to the year

ended 31.3.2013, compute the total income for the AY 2013-14, if he is:

(i) ROR (ii) NOR (iii) NR

Particulars

a) Profit on sale of shares of an Indian company,

received in Germany

15,000

b) Dividend from a Japanese company, received in

Japan.

10,000

c) Income from business in London deposited in a bank

in London

75,000

d) Dividend from RP Ltd., an Indian Company

6,000

e) Agricultural income from land in Gujarat

25,000

PCC MAY - 2010

Question 12. (2 Marks each)

Answer the following with reasons having regard to the provisions of the Income-Tax Act, 1961

for the Assessment Year 2013-14:

(i) State the Scope of total income in the case of an individual, whose residential status is non-

resident with reference to section 5(2) of the Act.

(ii) Mr. X a citizen of India received salary from the Government of India for the services

rendered outside India. Is the salary income chargeable to tax?

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page12

PCC NOV - 2009

Question 13. (7 Marks)

Determine the taxability of income of US based company Heli Ltd., in India on entering following

transactions during the financial year 2012-13:

(i) Rs.5 lacs received from an Indian domestic company for providing technical know how in

India.

(ii) Rs.6 lacs from an Indian firm for conducting the feasibility study for the new project in

Finland.

(iii) Rs.4 lacs from a non-resident for use of patent for a business in India.

(iv) Rs.8 lacs from a non-resident Indian for use of know how for a business in Singapore.

(v) Rs.10 lacs for supply of manuals and designs for the business to be established in

Singapore.

Explain the rate of tax applicable on taxable income for US based company, Heli Ltd., in India.

NOTE: Tax rate for domestic company is 30% and for foreign company is 40%. Surcharge, if

income is above Rs 1 crore is 5% for domestic company and 2% for foreign company.

Education cess & SHEC shall apply in normal way to both the companies.

PE-II NOV - 2009

Repeat Question of PCC MAY 2012 (10 Marks)

PE-II MAY - 2008

Question 14 (1 Marks)

Choose the correct answer with reference to the provisions of the Income-tax Act, 1961:

Income accruing in Japan and received there is taxable in India in the case of

(a) Resident and ordinarily resident only

(b) Both resident and ordinarily resident and resident but not ordinarily resident

(c) Both resident and non-resident

(d) Non-resident

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page13

BASICS - EXTRA

Section Particulars

2(7) Assessee

2(9) Assessment year

2(31) Person

2(34) & 3 Previous Year defined

FEW IMPORTANT DEFINITIONS ;

Person [Section 2(31)] : Person includes:

(i) An Individual;

(ii) A Hindu Undivided Family:- Under the Income tax law, a HUF is treated as a separate

entity for the purpose of taxation.

(iii) A company(whether Indian or foreign);

(iv) A firm;

(v) An Association of Persons (AOP) or a Body of Individuals (BOI), whether incorporated or

not e.g. clubs, co-operative societies etc.

(vi) A local authority e.g. MCD,DDA,DVB etc;

(vii) Every artificial judicial person not falling within any of the preceding sub-clauses e.g. Delhi

University / Bar council.

Assessee [Section 2(7)] : Assessee means a person by whom any tax or any other sum of

money (penalty / interest) is payable as per this Act and includes the following:

(i) Every person in respect of whom any proceeding under the Income-tax Act has been

taken for the assessment of his income or

the income of any person in respect of which he is assessable or

to determine the loss sustained by him or by such other person, or

the amount of refund due to him or such other person.

(ii) A deemed assessee - A person who is deemed to be an assessee for some other

person, is called Deemed Assessee.

For example,(i) after the death of a person, his legal representative will be treated as an

assessee for that income of the deceased on which tax has not been paid by the

deceased before his death ; (ii) a person representing a foreigner or a minor or a lunatic

is treated as an assessee for the income of such foreigner or minor or lunatic.

(iii) Assessee who is deemed to be an assessee in default -

When a person is responsible for doing any work under the Act and if he fails to do it, he

is called an Assessee in default.

For example, if a person while making any payment to another person, is liable to

deduct income tax thereon at source, does not deduct income tax therefrom, or

having deducted it, does not deposit it in the Government Treasury, he will be

treated as an assessee in default for that income tax.

Likewise under section 218, if an assessee does not pay advance tax, he shall

be deemed to be assessee in default.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page14

Assessment Year [Section 2(9)]: Assessment Year means the period of 12 months

commencing on the first day of April every year.

It is, therefore, the period from 1

st

April every to 31

st

of March.

Previous Year [Section 2 (34) & 3]: According to section save as otherwise provided in this

section, previous year means the financial year immediately preceding the assessment year.

Income-tax is payable on the income earned during the previous year and it is assessed

in the immediately succeeding financial year which is called an assessment year.

Therefore, the income earned during the previous year 1

st

April 2012 to 31

st

March, 2013

will be assessed or charged to tax in the assessment year 2013 2014.

W.e.f. assessment year 198990, all assesses are required to follow a uniform previous

year i.e. the financial year (1

st

April to 31

st

March) as their previous year .i.e. they cannot

choose calendar year as their previous year.

First previous year for a business/profession newly set-up during the financial year or for

a new source of income:

In such a case the period beginning from the date of setting up of the business or from

the date the new source came into existence, and

Ending on the last day of that financial year i.e. 31

st

of March shall be first previous year

for that business or source of income.

Case where income of previous year is assessed in the same year; As a normal rule, the

income earned during any Previous year is assessed or charged to tax in the immediately

succeeding assessment year.

However, in the following circumstances the income is taxed in the same year in which it is

earned:

1. Non-resident shipping business (Section 172)

2. Assessment of persons leaving India (Section 174)

3. Associations/ bodies formed for short duration (Sec. 174A)

4. Assessment of person trying to alienate his assets with a view to avoid tax

(Section 175)

5. Discontinued business (Section 176)

Section 172 : Non resident shipping business: Section 172 is applicable if the following

conditions are satisfied:

(a) the taxpayer is a non-resident ;

(b) he owns a ship or ship is chartered by the non-resident taxpayer ;

(c) the ship carries passengers, livestock, mail or goods shipped at a port in India ; and

(d) the non-resident taxpayer may (or may not) have an agent / representative in India.

If all the aforesaid conditions are satisfied, 7.5 per cent of amount paid (or payable) on account

of such carriage (including demurrage charge or handling charge or similar amount) to the non-

resident taxpayer shall be deemed to be the income of the taxpayer.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page15

Departure after approval & tax payment only:-For this purpose, the master of the ship shall

submit a return of income before the departure of the ship from the Indian port (such return may

be submitted within 30 days of the departure of the ship, if the Assessment Officer is satisfied

that it will be difficult to submit the return before departure and if satisfactory arrangement for

payment of tax has been made).

Unless the tax has been paid (or satisfactory arrangements have been made for payment

thereof), a port clearance shall not be granted by the Collector of Customs.

In case covered by this section, the income of a previous year is charged in the same

year and not in the immediately following assessment year.

Double taxation avoidance agreements: This section, however, does not apply in a

case where the non-resident belongs to a country that has an agreement on avoidance

of double taxation with India, in which case such earnings are taxed in accordance with

that agreement.

In cases where ships are owned by an enterprise belonging to a country with which India

has entered into an Agreement of Avoidance of Double Taxation, and the Agreement

provides for taxation of shipping profits only in the country of which the enterprise is a

resident, no tax is payable by such ships at the Indian ports.

Section 174 Assessment of Persons Leaving India

When it appears to the Assessing Officer that any individual may leave India during the

current assessment year or shortly after its expiry, and that he has no present intention

of returning to India, the total income of the individual for the period noted below is

charged to tax in that assessment year :

commencing from first day of assessment year, and

up to the probable date of his departure from India.

Separate assessments are made for each completed previous year or part thereof.

Example : A, a foreign citizen is residing in India since 2001. While completing assessment for

the AY 2012-13, on Feb 10, 2013, the AO comes to know that A will leave India on April 15,

2013 with no intention of returning. In this case, the Assessing Officer will make three

assessments for the AY 2012-13:

1. Regular assessment for PY 2011-12

2. Assessment u/s 174 for PY 2012-13

3. Assessment u/s 174 for the period 1/4/2013 to 15/4/2013.

All assessments shall be completed separately. Income shall not be aggregated. Relevant rates

of tax shall be applicable.

Section 174A Association/ bodies formed for short duration

Section 174A has been inserted from the assessment year 2002 03. This section is

applicable as follows-

1. There is an association of persons or a body of individuals or an artificial judicial person,

formed or established or incorporated for a particular event or purpose.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page16

2. It appears to the Assessing Officer that the above mentioned association, body etc., is likely

to be dissolved in the assessment year in which such association of persons or body of

individuals or artificial person was formed or established or incorporated or immediately after

such assessment year.

3. The total income of such association for the period from the expiry of the previous year for

that assessment year up to the date of its dissolution shall be chargeable to tax in that

assessment year.

Provision illustrated:- X co. is an association of two individuals X & Y. It is formed on April 22,

2011 for the purpose of completing a contract given by a German company in India. It is likely to

be dissolved on October 5, 2012. While processing the return submitted by the association for

the assessment year 2012 13, the assessing officer comes to know on August 16, 2012 about

the probable date of dissolution. In this case, the Assessing Officer will make two assessments

for the assessment year 2012 13

a. regular assessment for the previous year 2011 12 (i.e. income of the period April 22, 2011

to March 31, 2012); and

b. assessment for the income of the period April 1, 2012 to October 5, 2012.

The above two income assessments shall be completed separately. For the first assessment,

tax shall be chargeable at the rates applicable for the assessment year 2012 13. For the

second assessment tax shall be chargeable at the rates applicable for the assessment year

2013 14.

Section 175 Assessment of Persons Likely to Transfer Property to Avoid Tax

If it appears to the Assessing Officer that any person is likely to sell, transfer, dispose of

or otherwise part with any of his assets, with a view to avoiding payment of any liability,

the total income of such person for the specified period is taxed in the assessment year

in which it so appears to the Assessing Officer.

Specified period is the period commencing from the first day of assessment year and up

to the date when the Assessing Officer commences proceedings under this section.

Separate assessments are made for each completed previous year or part thereof

included in the above period. Therefore, income for such periods cannot be aggregated

for the purposes of assessment.

Section 176 Discontinued Business

This section covers any business or profession that is discontinued in any assessment year,

i.e., the business is ceased.

Implications of such discontinuance in terms of sub-sections (1) and (2) are as follows :

The income for the specified period is taxed in the assessment year of

discontinuance. Specified period is the period commencing from the first day of

assessment year and up to the date of discontinuance.

Such income is charged to tax at the discretion of the Assessing Officer. If such

discretion is not exercised, the income of the discontinued business is taxed in

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page17

the normal way in the assessment year immediately following the previous year

of discontinuance.

Separate assessments are made for each completed previous year or part

thereof included in the above period [income for such periods cannot be

aggregated].

Related procedures may be stated as follows :

Any person discontinuing the business or profession has to give notice of such

discontinuance to the Assessing Officer within 15 days of the discontinuance.

The Assessing Officer may serve a notice on the following persons to furnish a

return within the specified time [not being less than 7 days]:

The person whose income is to be assessed.

In case of a firm, any person who was partner of the firm at the time of

discontinuance.

In the case of a company, the principal officer.

It may be noted that while in first four cases their is no choice i.e. it is mandatory for the

Assessing Officer to follow the process discussed above but in the last case, their is a

choice for the assessing officer i.e. if he wish he can assess the case or alternatively he

can wait till the assessment year.

Some important principle which explain the concept of income for Income-tax purpose are

given below:

(i) Regularity of Income:

To be taxable it is not necessary that a particular source of income is regular.

Thus even casual incomes like lotteries, winnings from races etc. are taxable.

(ii) Form of Income:

Income can be received in cash or in kind i.e. in the form of money or money worth.

Wherever income is received in kind like perquisites then its value has to be found as

per the rules prescribed and this value shall be taken to be the income.

(iii) Legal Vs. Illegal Income:

For purposes of Income -tax, there is no difference between legal and illegal income.

Even illegal income is taxed just like any legal income.

For example the income earned from smuggling activities would also be taxable

under the Act.

If this were not so then the illegal activity would be put at a premium because a

person carrying on this activity would get immunity from payment of taxes, while an

honest tax-payer carrying on a legal business would be paying taxes on his income.

(iv) Disputed Income:

Any dispute regarding the title of the income cannot hold up the assessment of the

income in the hands of the recipient.

In such cases it is the assessing officer who decides regarding the taxability of such

disputed income.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page18

(v) Basis of Income:

Income can be taxed on receipt basis or on accrual basis.

In case of income from business or income from other sources the taxability would

depend upon the method of accounting adopted by the assessee.

Income from salaries is taxable on due or received basis, whichever is earlier.

While in other cases, it would generally be taxed on accrual basis.

Lumpsum Receipt:

If a receipt is an income then whether it is received in lump sum or in installments

would not affect its taxability; for example if a person receives arrears of salary in a

lump sum amount, it would still be his income.

(vi) Revenue Receipt vs. Capital Receipt:

Generally a revenue receipt is taxable as income.

However, there are certain provisions under which such receipt may be exempted

from tax (e.g. under section 10).

A capital receipt on the other hand is normally not taxable.

unless it has been specifically provided for, like in the case of capital gains.

(ix) Casual Income:

It is a casual receipt, received by chance, not anticipated, of non-recurring nature.

Gifts from relatives being of personal nature are exempt unless they can be regarded

as an addition to salary or

where they arise from the exercise of a business or profession.

Following receipts are chargeable to tax, even if they are casual and non-recurring in nature.

- capital gains

- Lottery income, winning from horse races etc.

- Receipts arising from business or exercise of a profession or occupation.

- Receipts by way of addition of remuneration of an employee e.g. arrears of bonus or salary

etc.

Diversion of income by overriding title vs. Application of income Any

expenditure/investment, after income is received, is application of income. Income under the

Income-tax Act, which is chargeable to tax, is income before application of income. Any

expenditure/investment out of such income is deductible only if it is permitted by a provision

under the Income-tax Act or Income-tax Rules.

Diversion of income is where by an obligation, income is diverted to some other person. When

an assessee on behalf of some other person receives income and later on it is diverted to such

person, it is known as diversion of income and, consequently, it is not chargeable to tax. For

example remuneration received by first author (written by two or more persons) for writing an

article in the newspaper. In this case, though total amount may be received by first person and

later on apportioned but still it will be proportionately taxable.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page19

What is amalgamation [ Sec. 2(1B)]

For a merger to qualify as an amalgamation for the purpose of the Income-tax Act, it has to

satisfy the following conditions :

Condition 1 All the properties of the amalgamating company immediately before

the amalgamation should become the property of the amalgamated

company by virtue of the amalgamation

Condition 2 All liabilities of the amalgamating company immediately before the

amalgamation should become the liabilities of the amalgamated

company by virtue of the amalgamation

Condition 3 Shareholder holding not less than three-fourths (in value) of the

shares in the amalgamating company (other than shares already held

by the amalgamated company or by its nominee) should become

shareholder of the amalgamated company by virtue of the

amalgamation

To illustrate the aforesaid condition (3), where A Ltd. merges with X Ltd. in a scheme of

amalgamation, and immediately before the amalgamation, X Ltd. held 20 percent of the shares

in A Ltd. the abovementioned condition will be satisfied if shareholder holding not less than

(in value) of the remaining 80 per cent of the shares in A Ltd., i.e. 60 per cent thereof (3/4 x 80),

become shareholder of X Ltd. by virtue of the amalgamation. Where, however, the whole of the

share capital of a company is held by another company, the merger of the two companies will

qualify as an amalgamation within section 2(1B), if all other conditions are fulfilled.

Transactions not treated as amalgamation Section 2(1B) specifically provides that in the

following two cases there is no amalgamation for the purpose of the Income-tax Act, though

the element of merger exists :

a. Where the property of the company which mergers is sold to the other company and the

merger is a result of a transaction of sale;

b. Where the company which merges is wound up in liquidation and the liquidator

distributes its property to the other company.

In these two cases, there would not be an amalgamation with in the meaning of section

2(1B).

Tax rates are not given under the Income-tax Act, 1961 but by the annual Finance Act,

Discuss.

Provisions for computation of taxable income are given by the Income-tax Act.

Tax rates are not given by the Income-tax Act, but by the Finance Act which is passes by

Parliament along with budget for the Central Government every year.

Apart from making various amendments in the Income-tax Act (and other direct/indirect tax

laws) every Finance Act specifies (in the First Schedule) income-tax rates for the current

assessment year and advance tax rates for the next assessment year.

For instance, the Finance Act, 2012, provides tax rates in the First Schedule (Parts I, II and III)

as follows

Part I of the First Schedule to the Finance Act, 2012 It gives income tax rates for different

assessees for the assessment year 2012-13.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page20

Part II of the First Schedule to the Finance Act, 2012 It gives rates for deduction of tax at

source applicable for the financial year 2012-13. To put it differently, if a person is

responsible for making a payment on which he is supposed to deduct tax at source during

the financial year 2012-13,then tax has to be deducted at source during 2012-13 at the rates

given in Par II of the Fist Schedule to the Finance Act, 2012. However, rate for tax deduction

from salary is given by Part III.

Part III of the First Schedule to the Finance Act, 2012 It gives tax rates for different

assesses for payment of advance tax during the financial year 2012-13 (i.e., for the

assessment year 2013-14). The same rates are applicable, for the tax deduction from salary

payment during the financial year 2012-13.

Generally, Part III of the Fist Schedule of a Finance Act becomes Part I of the Fist Schedule

of the subsequent Finance Act. For instance, Part III of the first Schedule to the Finance Act,

2012 will become Part I of the First Schedule to the Finance Act, 2013.

Maximum marginal rate of tax It is defined by section 2 (29C) as the rate of income tax

(including surcharge) applicable in relation to the highest slab of income in the case of an

individual as specified by the relevant Finance Act. For instance, for the assessment year

2013-14, the maximum marginal rate of tax is 30.9%.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page21

DEFINITION OF INCOME U/S 2(24)

The term Income specifically includes the following:

1. Profits and gains: Income includes profits and gains.

2. Dividend

3. Voluntary contributions received by trust : Voluntary contributions received by following

is income :

Charitable or religious trust

Scientific research association

University or educational institution or hospital

Electoral trust i.e. trusts of political parties approved by CBDT

4. Perquisites or profits in lieu of salary

5. Official or personal allowances

6. CCA & DA

7. Benefits to Directors or persons substantially interested in the concern

8. Benefit or Perquisite to a representative Assessee : e.g. a trustee appointed under a

trust. Suppose A is one of the trustee of a charitable trust. The trust provides him a

residential flat. The perquisite value of the flat is treated as income of A.

9. Compensations : Like for termination of agency contracts, Non competing

compensations etc. Export incentives like Duty drawback, sale of import licence, cash

assistance etc are also treated like income. Salary and interest received by a partner

from his firm is also covered.

10. Capital gains

11. Insurance profits : Profits generated by business of insurance

12. Banking income of a cooperative society

13. Winning from lottery, horse races etc.

14. Employees contribution towards PF etc received by employer

15. Amount received under keyman insurance policy

16. Taxable gifts

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page22

INCOME EXEMPT FROM TAX

1. Agricultural income Section 10(1)

2. Share of profit received by a member from HUF Section 10(2)

3. Share of profit received by a partner from partnership firm Section 10(2A)

4. Interest received by a person who is resident outside India on amounts credited in the

Non resident (External) Account Section 10(4)

5. LTC Section 10(5)

6. Remuneration received by foreign diplomats Section 10(6)

7. Salary received by a foreign citizen as an employee of a foreign enterprise provided his

total stay in India does not exceed 90 days Section 10(6)

8. Salary received by a non resident foreign citizen as a member of ships crew provided

his total stay in India does not exceed 90 days Section 10(6)

9. Remuneration received by an employee, being a foreign national, of a foreign Govt

deputed in India for training in a Govt establishment or public sector undertaking

Section 10(6)

10. Foreign allowances and perquisites granted by the Govt of India to its employees posted

abroad Section 10(7)

11. Remuneration received by Non residents from a foreign Govt in connection with

Cooperative Technical assistance programme in India Section 10(8)

12. Gratuity Section 10(10)

13. Commuted pension Section 10(10A)

14. Leave salary at retirement Section 10(10AA)

15. Retrenchment Compensation Section 10(10B)

16. Compensation from the Central Govt or a state govt or a local authority received by an

Individual or his legal heir on account of any disaster Section 10(10BC)

17. VRS Section 10(10C)

18. Tax on perquisite paid by employer Section 10(10CC)

19. Amount received on Life Insurance policy (including bonus) Section 10(10D)

The main provisions are as follows:

a. Amount received u/s 80DD : Deposits for physically handicapped dependent relative

taxable

b. Amount received under Keyman Insurance Policy : Taxable

c. Amount received on death of person Exempt

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page23

d. Amount received under policy issued before 1/4/2003 Exempt

e. Amount received under policy issued On or after 1.4.2003 but upto 31.3.2012

Exempt if premium paid is upto 20% of sum insured

f. Amount received under policy issued on or after 1.4.2012 Exempt if premium paid

is upto 10% of sum insured

20. Amount received at the time of retirement from SPF Section 10(11)

21. Amount received at the time of retirement from RPF Section 10(12)

22. Amount received from Superannuation fund Section 10(13)

23. HRA Section 10(13A)

24. Special allowances Section 10(14)

25. Interest from specified bonds like Capital investment bonds, NRI bonds, Relief bonds etc

Section 10(15) Discussed in the chapter of IFOS

26. Educational scholarships by any employer or any other person Section 10(16)

27. Daily allowance & Constituency allowance for MLAs and MPs Section 10(17)

28. Rewards given by the Central or state Government

For literary, scientific or artistic work or

For service for alleviating the distress of the poor or the weak and the ailing or

For proficiency in sports and games or

Gallantry awards approved by Govt

Section 10(17A)

29. Pension and family pension of Gallantry award winners Section 10(18)

30. Family pension received by family members of armed forces (who died in the course of

operational duties) Section 10(19)

31. Income of Local Authorities Section 10(20)

32. Any income of housing boards constituted in India for planning, development or

improvement of cities, towns or villages Section 10(20A)

33. Any income of approved research associations 10(21)

34. Income of Professional institutions established in India for the purpose of control,

supervision, regulation or encouragement of the profession of law, accountancy,

engineering, architecture, company secretary etc. Section 10(23A). Income from

house property or income by way of interest or dividend etc is not exempt.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page24

35. Income of a welfare fund is exempt from tax if it is approved by Commissioner Income

Tax and the benefits are being provided to member employee / family members in the

event of

Death / retirement of the member employee

Cost of education of his dependent children

Medical treatments /check ups

Section 10(23AAA)

36. Income of an authority established for development of Khadi and Village Industries

Section 10(23BB)

37. Income of PM National Relief Fund Section 10(23C)(i)

38. Income of a University or educational institution It is exempt if

a. Wholly or substantially financed by Govt; or

b. Existing for non-profit reasons and if annual receipts are upto Rs 1 crore; or

c. Existing for non-profit reasons and approved by Chief Commissioner of Income tax.

Section 10(23C)

39. Income of Hospital It is exempt if hospital existing for non-profit reasons (philanthropic

purposes) and is

a) Wholly or substantially financed by Govt; or

b) Existing for non-profit reasons and if annual receipts are upto Rs 1 crore; or

c) Existing for non-profit reasons and approved by Chief Commissioner of Income tax.

Section 10(23C)

40. Income of Investor Protection fund Section 10(23EA)

41. Income of Venture Capital Funds and Venture Capital companies [both Registered with

SEBI and acquiring shares of Venture Capital undertakings] Section 10(23FB)

Venture Capital undertaking means a domestic company whose shares are not listed

in a recognized stock exchange in India. They can be in business of providing services

or in production or manufacture of article or things. These should not be engaged in

activities not permitted under Industrial policy of the Govt.

It is important to note here that the exemption shall continue even if the shares of the

venture capital undertaking are subsequently listed in a recognized stock exchange in

India.

42. Income by way of interest on securities, property income and income from other sources

of a registered trade union or an association of registered trade unions Section 10(24)

43. Incomes of SPF, RPF, Approved Superannuation Fund, Approved Gratuity Fund

Section 10(25)

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page25

44. Income of Employees State Insurance Fund Section 10(25A)

45. Income of a member of a Scheduled Tribe, residing in Nagaland, Manipur, Tripura,

Arunachal Pradesh, Mizoram, Ladakh or in Sikkim by working in these states or income

by way of dividend or interest in securities Section 10(26)/(26AAA)

46. Any income of a statutory corporation or of a body /institution, financed by the Govt

formed for promoting the interest of scheduled castes / tribes Section 10(26B)

47. Income of a cooperative society formed for promoting interest of members of SC/ST

Section 10(27)

48. Income of minor being clubbed Section 10(32)

49. Dividend from domestic company Section 10(34)

50. Interest on Units of UTI / Mutual Funds Section 10(35)

51. Capital gain on compensation received on compulsory acquisition of urban agricultural

land Section 10(37)

52. LTCG on transfer of Listed equity shares after paying STT Section 10(38)

53. Any amount received by an individual as a loan (either in lump sum or installment) in a

transaction of reverse mortgage Section 10(43)

54. Perquisites / Allowances to Chairman / Members of UPSC Section 10(45)

55. Income from units in SEZ Section 10AA

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page26

INCOME OF CHARITABLE & RELIGIOUS TRUST

Question 1 : Explain the provisions regarding taxation of charitable trusts.

Ans: Income of Charitable Trusts is exempt u/s 11

In order to claim exemption, a Charitable or Religious trust should fulfill the below conditions

Trust should be created for a lawful purpose

Trust should be for charitable or religious purpose

Property should be held under trust

Trust should be registered with CIT (Commissioner of Income Tax) u/s 12AA

Accounts should be audited if Total Income before exemption u/s11 & 12 Exceeds

exemption amount (i.e. Rs.2,00,000)

Trust should not be created for the benefit of particular community or caste

Trust can carry out business activities if the business activities are incidental to the

attainment of its objectives & separate books are maintained.

Funds of the trust should be invested or deposited as per Section 11(5)

Taxable income of the trust shall be computed as per normal tax provisions. Tax rates

applicable to individuals are applicable to the Charitable trusts.

A trust should apply its income from trust property & voluntary contributions to the extent

of at least 85% during the financial year itself.

BASIC CONCEPTS OF APPLICATION OF INCOME

1. It is any expenditure to achieve the objects of the trust. It can be a revenue or capital

expenditure.

2. Repayment of loan taken to fulfill one of the objectives of trust is treated as an

application of income for charitable purpose.

3. Granting of loan to students is an application of income. Though in the year of

repayment it shall be constituted like income again.

4. Even payment of taxes shall be treated like application of income.

5. Donation given by a trust is an application of income.

6. Utilisation of income for meeting expenses of earlier years is an application.

Section 11(5) (options of accumulation of money)

i. Central/State Government Securities

ii. Govt saving certificates

iii. Deposits/Bonds of Financial Corporation providing long-term finance for

industrial development

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page27

iv. Deposits/Bonds of public company providing long term finance for

residential houses or urban infrastructure

v. Units of UTI, Mutual funds

vi. Deposits with IDBI

vii. Deposit with Schedule Bank, Co-op Bank, Post Office Saving Bank.

viii. Immovable property

ix. Investment in debentures or bonds of any corporate body, where repayment

of principle and interest is guaranteed by Central or State Govt.

x. Investment or deposit in any public sector company

xi. Deposit with housing authority or authority for development of towns and

cities

xii. Acquiring shares of National skill development corporation

xiii. Investment in shares of a depository

xiv. Any other mode of investment as may be prescribed

Various types of Income of a Trust

1. Income from property held under trust

2. Voluntary contributions (donations) not forming part of Corpus

3. Voluntary contributions (donations) forming part of Corpus. (Just like capital of

company). It is fully exempt. Assessee has to prove that voluntary contribution

received is forming corpus of the trust. Condition of 85% application is not applicable

on such contributions / donations received.

4. Business Income

Section 11(1)

15% is the accumulation allowed for future. No time limit for usage. Funds should

be invested as per Section 11(5).

1 + 2 + 4 (Mentioned above)

APPLIED for Charitable or Religious

purpose in India

Amount of Exemption

Income applied is atleast 85% : 100%

I Income applied less than 85% : Amount

applied + 15%

Applied for Charitable Purpose outside India

Exempt, provided such trust created for

Promoting INTERNATIONAL WELFARE in

which India is interested

15% accumulation not allowed here.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page28

Question 2: A registered charitable trust discloses the following particulars for PY 12-13.

Gross receipts from property held under trust : 10,00,000

Expenditure for charitable & religious purpose in India

Case 1 : 9,00,000

Case 2 : 5,00,000

Determine the Total Income for A/Y 13-14.

INCOME APPLIED for charitable or religious purpose means

Income actually applied for Charitable or Religious purposes in India

Income deemed to be applied for Charitable or Religious purpose in India

Income deemed to be applied

A) Where income not applied due to non-receipt of Income during previous year:

Such income should be applied for Charitable & Religious purpose during P/Y of actual

receipt or during next P/Y

B) Where income not applied due to other reasons (e.g. received very near to closing of

financial year)

Such income should be applied for Charitable & Religious purpose during P/Y next to previous

year to which such income relates

Note:

To avail the facility of the above extended period of application of income, the trust

has to exercise an option in writing (No form prescribed). Such option has to be

exercised before the expiry of the time allowed u/s 139(1) for submission of returns.

Question 3 : Assume in question 1, case 2, Rs.2,50,000 could not be applied upto 31.3.2013

because

a) Amount was not received upto 31.3.2013 & finally received on 11.9.2015.

b) Due to other reasons (like amount received on 30.3.2013)

Section 11(2): Additional exemption for Income accumulated or set apart in excess

of 15%

Where 85% income not applied (actual or deemed) for charitable &religious purpose

then additional exemption shall be available for such amount

which is accumulated or set apart for application in future year

Provided

Notice is given to A.O is in Form 10 on or before 139(1) date, specifying period and purpose for

which such income is accumulated.

However, period cannot exceed 5 yrs from P/Y in which such income is derived and

Money so accumulated or set apart is invested or deposited in mode specified in Sec.11(5)

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page29

Note : In computing the period of 5 years, the period during which the income could not be

applied for the purposes for which it is accumulated, due to an order of any court, shall be

excluded.

CONSEQUENCES OF DEFAULT IN ABOVE SITUATION

1. Funds not used for the purpose for which accumulated Taxable in the FY of misuse

2. Funds does not remain invested as per 11(5) Taxable in FY of default

3. Funds non utilized or under utilized in prescribed period of 5 Years + one extn year

allowed for using these accumulated funds Taxable in the Extn FY e.g. Rs 5 lacs

saved in FY 2012-13 for utilizing them upto next 5 years i.e. upto 2017-18. If such funds

are not fully utilized upto 2017-18 & extn year 2018-19, then unutilized amount shall be

taxable in FY 2018-19 (AY 2019-20).

4. Such accumulated amount can not be paid to other trusts / institutions as donation

(Though it can be done in the year of dissolution of the trust).

5. If funds cannot be utilized due to reasons, beyond the control of trustees, AO, on

application, may allow funds to be utilized for other objects of the trust.

Question 4 : A registered charitable trust discloses the following particulars for PY 12-13.

Gross receipts from property held under trust : 10,00,000

Expenditure for charitable & religious purpose in India : 5,00,000

The trust wants to set apart 2,00,000 for application for Charitable or religious purpose in

future years (5 years). Determine the conditions to be fulfilled and what will be the total Income

for AY 13-14 if such conditions are fulfilled.

What shall be the consequences if out of accumulated funds of Rs 2,00,000 above, only Rs

1,35,000 is utilized till 31.3.2019.

Section 13: Cases when Exemption u/s. 11 or 12 Not Available

[FORFEITURE OF EXEMPTION]

Income used

for private

religious

purpose, not for

public benefit

Trust created

for benefit of

particular

religious

community

See Note 1

According to the

terms of trust,

Income is to applied

for benefit of

specified persons

u/s. 13(3)

See Note 2

During previous

year income used

for benefit of

specified person

u/s. 13(3)

See note 3 &4

Funds not

invested

u/s. 11(5)

See note 5

In above cases, exemption shall be lost & trust shall be taxable at maximum marginal rate of tax

i.e. 30.9%

Note 1 : A trust or institution created or established for the benefit of Scheduled Castes,

Backward classes, Scheduled tribes or women and children shall not be deemed to be a trust or

institution created or established for the benefit of a religious community or caste for this

purpose.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page30

Note 2 : Sec. 13(3): Specified Persons

1. Author of Trust.

2. Person contributed greater than 50,000/- during P/Y

3. Where person above (in point 1 or 2) is a HUF, any member of such HUF

4. Trustee/Manager of trust

5. Relatives of (persons under points 1, 2, 3, 4, )

6. Concern in which (persons under points 1, 2, 3, 4, 5) has Substantial interest

(i.e. HOLDING 20% of equity shares or 20% of profits of the concern whether held

singly or jointly with other persons mentioned above)

Relative :

a. Spouse of the individual

b. Brother or sister of the individual

c. Any lineal ascendant or descendant of the individual

d. Any lineal ascendant or descendant of the spouse of the individual

e. Spouse of the person referred to in (b), (c), (d) or (e) above;

f. Any lineal ascendant or descendant of a brother or sister of either the individual or of the

spouse of the individual.

Note 3 : If any medical or educational facility is provided to the specified persons, the whole

exemption shall not be lost. Only the value of benefit shall become taxable.

Note 4 : WHAT IS MEANT BY GIVING BENEFIT TO INTERSTED PERSONS

1. Loan is given without adequate security or adequate rate of interest

2. Property is given without adequate rent

3. Excess salary is being provided

4. Services of trust being provided at inadequate consideration

5. Any share or property is purchased from interest persons at higher price or sold to them

at lower price

6. Any income or property is given to them above Rs 1000 p.a.

7. Investment exceeding 5% Of capital of a concern in which such persons have

substantial interest.

Note 5 : Convert the non confirming assets / funds

Acceptance of donations in kind or acquiring any asset not confirming to the provisions of

section 11(5) will not make the fund or trust or institution lose tax exemption. The trust or

institution shall be required to dispose of or convert the asset not confirming to the requirement

of section 11(5) into permissible investment within one year from the end of the financial year in

which such assets are acquired.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page31

Concept of anonymous donation Section 115BBC

It means a donation where the information about the name and address of the donor is not

available.

The provisions:

1. For Wholly Religious entities Section 115BBC not applicable (Normal provisions apply

i.e. 15% deduction allowed plus 85% should be applied in FY itself)

2. For educational / medical institutions / charitable entities / partly religious & partly

charitable entities :

a. Exempt if upto Rs 1 lac p.a

b. Exempt if upto 5% of total donations (other than corpus donations)

c. If higher amounts then higher of Rs 1 lac or 5% of total donations is exempt and

balance amount taxable u/s 115BBC @ 30% flat. Actual expenditure shall not be

relevant. Please note that this exemption of 5% etc is at the time of computing tax

and not at the time of computing income.

d. 15% standard deduction not allowed against such donations if received by

educational / medical institutions / charitable entities.

Example : One such trust has received total donations of Rs 100,00,000 out of which

anonymous donations are Rs 30,00,000, in this case, exemption allowed shall be 5% of Rs

100,00,000 or Rs 1,00,000 whichever is higher i.e. Rs 5,00,000 and balance anonymous

donations i.e. Rs 25,00,000 (30,00,000 5,00,000) shall be taxable @ 30%. Rs 5,00,000

shall not be taxable at all.

Amount spended for charitable purposes out of anonymous donation is not relevant. In this

example, suppose anonymous donation received is only say Rs 80,000 or only upto 5% of

total say Rs 3,50,000 than normal provisions shall apply.

Treatment of capital gains

It shall be computed as per normal provisions. If the net consideration is invested for acquiring

net capital asset within FY then exemption = Investment (-) Cost / Indexed cost of acquisition.

Meaning of Charitable Purpose Section 2(15)

Charitable purpose includes

- relief of the poor,

- education,

- medical relief,

- preservation of environment (including forests and wildlife) and preservation of

monuments or places or objects of artistic or historic interest,

- advancement of any other object of general public utility

Advancement of any other object of general public utility should not be in the nature of

business however if the gross receipt is upto `25,00,000, it will be considered to be charitable

purpose but if gross receipt is exceeding `25,00,000, it will not be considered as charitable

purpose.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page32

Example

One charitable trust has the business of publishing of books on social and religious

matters and gross receipt is Rs 24,00,000, in this case, it will be considered to be charitable

purpose but if gross receipt is more than Rs25,00,000, entire income shall be taxable.

Similarly, one such trust is running a coaching centre for music & drama and gross receipt is

Rs 18,00,000, in this case, it will be considered to be charitable purpose but if gross receipt is

exceeding `25,00,000, entire income shall be taxable.

Any trust having the above objectives shall be considered to be charitable or religious trust.

Trust will include any other institutions or organizations also i.e. it will include even Society

registered under Societies Registration Act, 1860, company registered under section 25 of

Companies Act, 1956, or other similar institutions, provided they are for charitable purpose.

Return of income of charitable or religious trust or institution Section 139(4A)

If the total income of a charitable or religious trust or institution before exemption under sections

11 and 12 exceeds the maximum amount not chargeable to tax, then the trust or institution is

under an obligation to furnish the return of income within the time allowed under section 139(1)

and all provisions of the Income-tax Act shall apply as if it were a return furnished under section

139(1).

Note 1: The tax rates applicable to a religious/ charitable trust/ institution are the same as

applicable to an individual.

Note 2: As per section 12A, exemption under section 11 & 12 is available only if the trust /

institution gets its accounts audited in case the total income of the trust/ institution before

exemption under section 11 & 12 exceeds Rs2,00,000/-. Audit report should be submitted under

rule 17B in form No. 10B.

Note 3: The due date for filing of return under section 139(4A) is 30

th

September of the

assessment year.

Note 4: Return furnished under section 139(4A) is deemed to be return furnished under section

139(1) and can therefore be revised under section 139(5).

Few other points relating to Assessment of charitable trusts

1. Excess expenditure in one year may be set off against next years incomeCIT v

Maharana of Mewar Charitable Foundation, (1987) (Raj.).

2. Board has clarified that promotion of sports and games shall be considered to be

charitable.

3. Relief to poor : Relief must not be only to a group of private individuals rather it should

be a relief to the poor in general. Similarly for educational help also.

4. Trust can also be in the name of some private person.

NEERAJ GUPTA CA IPCC TAX CLASSES MISC

www.ngpacollege.comAssessmentYear201314Forsmsonly9810139214 Page33

Section 12A : Registration of Trust

Every trust wanting to claim exemption of its income u/s 11 or 12 shall make an application for