S-ar putea să vă placă și

- Self Esteem Building-Teaching How To Say NoDocument4 paginiSelf Esteem Building-Teaching How To Say NoSabah SarahÎncă nu există evaluări

- Introduction To Law1 (Old Version)Document37 paginiIntroduction To Law1 (Old Version)Sabah SarahÎncă nu există evaluări

- QuestionnaireDocument2 paginiQuestionnaireSabah SarahÎncă nu există evaluări

- Ghani KhanDocument3 paginiGhani KhanSabah SarahÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Pakistan's Lack of Entrepreneurship CultureDocument4 paginiPakistan's Lack of Entrepreneurship CultureUmar Kundi100% (1)

- Taxation-for-Development-Narrative-Report Final ReportDocument40 paginiTaxation-for-Development-Narrative-Report Final ReportJackÎncă nu există evaluări

- Assignment DataDocument284 paginiAssignment DataDerickMwansaÎncă nu există evaluări

- Farmer-Controlled Economic InitiativesDocument73 paginiFarmer-Controlled Economic InitiativesGreen Action Sustainable Technology GroupÎncă nu există evaluări

- BibliographyDocument19 paginiBibliographyLuis OliveiraÎncă nu există evaluări

- AdSurf PonziDocument23 paginiAdSurf PonzibizopÎncă nu există evaluări

- Credit LendingDocument64 paginiCredit LendingZubair Mirza100% (2)

- The Asian Growth MiracleDocument50 paginiThe Asian Growth MiracleKen AggabaoÎncă nu există evaluări

- Stand ChartDocument804 paginiStand Chartnagaraj100Încă nu există evaluări

- JWCh07 PDFDocument29 paginiJWCh07 PDF007featherÎncă nu există evaluări

- Assignment Public SectorDocument3 paginiAssignment Public SectorCeciliaÎncă nu există evaluări

- Barclays BankDocument14 paginiBarclays BankKavish SobronÎncă nu există evaluări

- Public Sector AccountingDocument10 paginiPublic Sector AccountingbillÎncă nu există evaluări

- EPGPX02 Group 3 - Strategic Decisions and ToolsDocument14 paginiEPGPX02 Group 3 - Strategic Decisions and ToolsrishiÎncă nu există evaluări

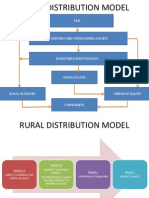

- Hul Distribution ModelDocument5 paginiHul Distribution ModelBhavik LodhaÎncă nu există evaluări

- IFRS 9 Financial InstrumentsDocument38 paginiIFRS 9 Financial Instrumentssaoodali1988Încă nu există evaluări

- Simple Interest Lesson PlanDocument5 paginiSimple Interest Lesson Planapi-3954158270% (1)

- Vesuvius India - Result Update-jun-17-EdelDocument11 paginiVesuvius India - Result Update-jun-17-EdelanjugaduÎncă nu există evaluări

- Envico LTDDocument2 paginiEnvico LTDKashif Mehmood100% (1)

- Branding of ProductDocument87 paginiBranding of ProductSuchismita DhalÎncă nu există evaluări

- Sept 2018 Top Links Work Round DocumentDocument65 paginiSept 2018 Top Links Work Round DocumentAndrew Richard ThompsonÎncă nu există evaluări

- Telecommunications in Nepal - Current State and NeedsDocument3 paginiTelecommunications in Nepal - Current State and NeedsSomanta BhattaraiÎncă nu există evaluări

- Entrepreneurship AssignmentDocument12 paginiEntrepreneurship AssignmentZubair A KhanÎncă nu există evaluări

- Capital Budgeting ProcessDocument17 paginiCapital Budgeting ProcessjanineÎncă nu există evaluări

- Accounting Types of Major Accounts Lesson PlanDocument2 paginiAccounting Types of Major Accounts Lesson PlanJessie Rose Tamayo92% (13)

- Chapter 1 Securities Operations and Risk ManagementDocument32 paginiChapter 1 Securities Operations and Risk ManagementMRIDUL GOELÎncă nu există evaluări

- Chapter 5 Capacity PlanningDocument78 paginiChapter 5 Capacity PlanningAnthony Royupa100% (1)

- India Russia Relations PDFDocument4 paginiIndia Russia Relations PDFAmalRejiÎncă nu există evaluări

- Module B Corporate Financing - Part 2Document333 paginiModule B Corporate Financing - Part 2Darren Lau100% (1)

- Specific RatiosDocument26 paginiSpecific RatiosSunil KumarÎncă nu există evaluări