S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Macroeconomics ConsolidatedDocument118 paginiMacroeconomics ConsolidatedViral SavlaÎncă nu există evaluări

- Checklist For Preparation and Review of Year End Reports Rev3122020Document70 paginiChecklist For Preparation and Review of Year End Reports Rev3122020errolÎncă nu există evaluări

- Indonesia Construction Equipment Market - April 2013Document83 paginiIndonesia Construction Equipment Market - April 2013girish_patkiÎncă nu există evaluări

- Analysis and Estimation of The US Oil ProductionDocument1 paginăAnalysis and Estimation of The US Oil ProductionEduardo PetazzeÎncă nu există evaluări

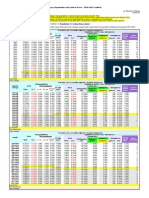

- India - Index of Industrial ProductionDocument1 paginăIndia - Index of Industrial ProductionEduardo PetazzeÎncă nu există evaluări

- Germany - Renewable Energies ActDocument1 paginăGermany - Renewable Energies ActEduardo PetazzeÎncă nu există evaluări

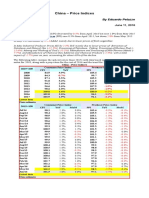

- China - Price IndicesDocument1 paginăChina - Price IndicesEduardo PetazzeÎncă nu există evaluări

- Highlights, Wednesday June 8, 2016Document1 paginăHighlights, Wednesday June 8, 2016Eduardo PetazzeÎncă nu există evaluări

- Turkey - Gross Domestic Product, Outlook 2016-2017Document1 paginăTurkey - Gross Domestic Product, Outlook 2016-2017Eduardo PetazzeÎncă nu există evaluări

- U.S. New Home Sales and House Price IndexDocument1 paginăU.S. New Home Sales and House Price IndexEduardo PetazzeÎncă nu există evaluări

- Reflections On The Greek Crisis and The Level of EmploymentDocument1 paginăReflections On The Greek Crisis and The Level of EmploymentEduardo PetazzeÎncă nu există evaluări

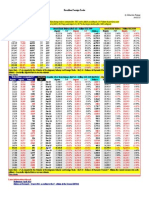

- WTI Spot PriceDocument4 paginiWTI Spot PriceEduardo Petazze100% (1)

- U.S. Employment Situation - 2015 / 2017 OutlookDocument1 paginăU.S. Employment Situation - 2015 / 2017 OutlookEduardo PetazzeÎncă nu există evaluări

- Commitment of Traders - Futures Only Contracts - NYMEX (American)Document1 paginăCommitment of Traders - Futures Only Contracts - NYMEX (American)Eduardo PetazzeÎncă nu există evaluări

- Brazilian Foreign TradeDocument1 paginăBrazilian Foreign TradeEduardo PetazzeÎncă nu există evaluări

- China - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaDocument1 paginăChina - Demand For Petroleum, Energy Efficiency and Consumption Per CapitaEduardo PetazzeÎncă nu există evaluări

- India 2015 GDPDocument1 paginăIndia 2015 GDPEduardo PetazzeÎncă nu există evaluări

- USA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesDocument1 paginăUSA - Oil and Gas Extraction - Estimated Impact by Low Prices On Economic AggregatesEduardo PetazzeÎncă nu există evaluări

- Singapore - 2015 GDP OutlookDocument1 paginăSingapore - 2015 GDP OutlookEduardo PetazzeÎncă nu există evaluări

- South Africa - 2015 GDP OutlookDocument1 paginăSouth Africa - 2015 GDP OutlookEduardo PetazzeÎncă nu există evaluări

- China - Power GenerationDocument1 paginăChina - Power GenerationEduardo PetazzeÎncă nu există evaluări

- US Mining Production IndexDocument1 paginăUS Mining Production IndexEduardo PetazzeÎncă nu există evaluări

- México, PBI 2015Document1 paginăMéxico, PBI 2015Eduardo PetazzeÎncă nu există evaluări

- European Commission, Spring 2015 Economic Forecast, Employment SituationDocument1 paginăEuropean Commission, Spring 2015 Economic Forecast, Employment SituationEduardo PetazzeÎncă nu există evaluări

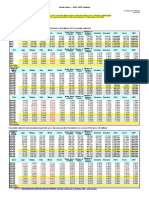

- Chile, Monthly Index of Economic Activity, IMACECDocument2 paginiChile, Monthly Index of Economic Activity, IMACECEduardo PetazzeÎncă nu există evaluări

- Highlights in Scribd, Updated in April 2015Document1 paginăHighlights in Scribd, Updated in April 2015Eduardo PetazzeÎncă nu există evaluări

- U.S. Federal Open Market Committee: Federal Funds RateDocument1 paginăU.S. Federal Open Market Committee: Federal Funds RateEduardo PetazzeÎncă nu există evaluări

- Mainland China - Interest Rates and InflationDocument1 paginăMainland China - Interest Rates and InflationEduardo PetazzeÎncă nu există evaluări

- US - Personal Income and Outlays - 2015-2016 OutlookDocument1 paginăUS - Personal Income and Outlays - 2015-2016 OutlookEduardo PetazzeÎncă nu există evaluări

- Japan, Population and Labour Force - 2015-2017 OutlookDocument1 paginăJapan, Population and Labour Force - 2015-2017 OutlookEduardo PetazzeÎncă nu există evaluări

- United States - Gross Domestic Product by IndustryDocument1 paginăUnited States - Gross Domestic Product by IndustryEduardo PetazzeÎncă nu există evaluări

- South Korea, Monthly Industrial StatisticsDocument1 paginăSouth Korea, Monthly Industrial StatisticsEduardo PetazzeÎncă nu există evaluări

- Japan, Indices of Industrial ProductionDocument1 paginăJapan, Indices of Industrial ProductionEduardo PetazzeÎncă nu există evaluări

- FRBM ActDocument8 paginiFRBM ActTanvi ShahÎncă nu există evaluări

- Managing A Family BudgetDocument5 paginiManaging A Family BudgetGaurav Umbarkar100% (1)

- Silang2018 Audit Report PDFDocument113 paginiSilang2018 Audit Report PDFLomo LomoÎncă nu există evaluări

- Situacion Economica VzlaDocument11 paginiSituacion Economica VzlaErwing HernándezÎncă nu există evaluări

- Tiss Sample Test PaperDocument53 paginiTiss Sample Test PaperLight ZoomÎncă nu există evaluări

- MSL 873: Security Analysis and Portfolio Management Minor AssignmentDocument9 paginiMSL 873: Security Analysis and Portfolio Management Minor AssignmentVasavi MendaÎncă nu există evaluări

- Jharkhand World BanK ReportDocument148 paginiJharkhand World BanK ReportJitendra NayakÎncă nu există evaluări

- Balanced Budget MultiplierDocument48 paginiBalanced Budget MultiplierSakthirama Vadivelu100% (1)

- Somaliland in Figures 2010Document82 paginiSomaliland in Figures 2010Kheyria GaheyrÎncă nu există evaluări

- IMF and PakistanDocument82 paginiIMF and PakistanAineekamranÎncă nu există evaluări

- PDU April 2022 April18 ForWEB FinalDocument43 paginiPDU April 2022 April18 ForWEB FinalumerjicÎncă nu există evaluări

- Economics 2 XiiDocument17 paginiEconomics 2 Xiiapi-3703686Încă nu există evaluări

- Philoid Test Series 73off PDFDocument17 paginiPhiloid Test Series 73off PDFM BanerjeeÎncă nu există evaluări

- Debt Peonage, Corporate Capitalism, Codex Alimentarius, and Tyranny: An Optimist's Guide To Lisbon.Document24 paginiDebt Peonage, Corporate Capitalism, Codex Alimentarius, and Tyranny: An Optimist's Guide To Lisbon.biko97jcjÎncă nu există evaluări

- Multiple Linear Regression Analysis On FDI and Foreign Exchange RateDocument15 paginiMultiple Linear Regression Analysis On FDI and Foreign Exchange RateSubodh Kumar BaranwalÎncă nu există evaluări

- Economy TermsDocument90 paginiEconomy TermsSabyasachi SahuÎncă nu există evaluări

- ACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilityDocument5 paginiACC 211 Discussion - Provisions, Contingent Liability and Decommissioning LiabilitySayadi AdiihÎncă nu există evaluări

- Important Bank TermsDocument22 paginiImportant Bank TermsZayed Mohammad JohnyÎncă nu există evaluări

- 01 Growth and InvestmentDocument22 pagini01 Growth and Investmentusman sattiÎncă nu există evaluări

- Economic Environment in India (B.com) P-2Document115 paginiEconomic Environment in India (B.com) P-2Anonymous uHT7dDÎncă nu există evaluări

- Jargon: Form NCERT BOOKS (Suggested by TARUN SIR)Document62 paginiJargon: Form NCERT BOOKS (Suggested by TARUN SIR)Dilip KumarÎncă nu există evaluări

- Response To PTI White Paper FinalDocument30 paginiResponse To PTI White Paper FinalKhawaja BurhanÎncă nu există evaluări

- 2020, A Global Debt Tidal Wave: April 2020Document5 pagini2020, A Global Debt Tidal Wave: April 2020anujÎncă nu există evaluări

- Vivekananda College,: Thakurpukur Kolkata-700063Document26 paginiVivekananda College,: Thakurpukur Kolkata-700063Paramartha BanerjeeÎncă nu există evaluări

- 14 Ch36-Six Debates Over Macroeconomic Policy-KeyDocument15 pagini14 Ch36-Six Debates Over Macroeconomic Policy-KeyChen JunhaoÎncă nu există evaluări

- Morocco Policy Analysis Model 1621235278Document47 paginiMorocco Policy Analysis Model 1621235278asbath alassaniÎncă nu există evaluări

- Peronomics, Populism and MMTDocument16 paginiPeronomics, Populism and MMTSkeletorÎncă nu există evaluări