S-ar putea să vă placă și

- DO It Yaselfadd-Tradelines-To-Credit-Reportucc-Filingspdf-Uniform PDFDocument18 paginiDO It Yaselfadd-Tradelines-To-Credit-Reportucc-Filingspdf-Uniform PDFNicole Smith100% (8)

- Property Securitization Memorandum: Consumer Defense ProgramsDocument31 paginiProperty Securitization Memorandum: Consumer Defense ProgramsFrederick DeMarques Thomas100% (2)

- Jean Keating InterviewDocument107 paginiJean Keating InterviewRandy Rosado98% (47)

- Finders' Fee Template-2Document3 paginiFinders' Fee Template-2David Jay Mor100% (1)

- The Fundamentals of CreditDocument20 paginiThe Fundamentals of CreditAlyssa Jane G. Alvarez100% (1)

- Lesson 6 - CreditDocument52 paginiLesson 6 - CreditDianne Joy MempinÎncă nu există evaluări

- Sale of Goods DissertationDocument8 paginiSale of Goods DissertationINeedSomeoneToWriteMyPaperUK100% (1)

- How To Find Pooling and Servicing Agreements Is Key To Killing Your ForeclosureDocument13 paginiHow To Find Pooling and Servicing Agreements Is Key To Killing Your ForeclosureJaniceWolkGrenadier100% (2)

- Escrow Institute of CaliforniaDocument5 paginiEscrow Institute of California51 PegasiÎncă nu există evaluări

- Securities Regulation - Cases and Materials - Aspen Casebook SeriesDocument535 paginiSecurities Regulation - Cases and Materials - Aspen Casebook SeriesSimon Holgersen100% (4)

- NY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized MortgagesDocument8 paginiNY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized Mortgages83jjmackÎncă nu există evaluări

- Talbots Harvard Case AnsDocument4 paginiTalbots Harvard Case AnsChristel Yeo0% (1)

- You're Welcome Planet Earth The Most Powerful Trading System PDFDocument44 paginiYou're Welcome Planet Earth The Most Powerful Trading System PDFLibert YoungÎncă nu există evaluări

- Dividend Policy and Internal FinancingDocument14 paginiDividend Policy and Internal FinancingMichaela San Diego0% (1)

- Assignment Business LawDocument30 paginiAssignment Business LawafmofeeshÎncă nu există evaluări

- Raising Money – Legally: A Practical Guide to Raising CapitalDe la EverandRaising Money – Legally: A Practical Guide to Raising CapitalEvaluare: 4 din 5 stele4/5 (1)

- House Lawyers Are in Securities, Health Care.20140401.200112Document2 paginiHouse Lawyers Are in Securities, Health Care.20140401.200112gramweeder1Încă nu există evaluări

- CrowdEngine Scott Anderson WebinarDocument6 paginiCrowdEngine Scott Anderson WebinarCrowdFunding BeatÎncă nu există evaluări

- Securities RegulationDocument29 paginiSecurities RegulationSwapan Kumar Saha100% (1)

- BR QbankDocument50 paginiBR QbankDraxÎncă nu există evaluări

- Recordation FraudDocument42 paginiRecordation FraudJeff Wilner78% (9)

- Legal Position of Stockbrokers 2023Document7 paginiLegal Position of Stockbrokers 2023TasmineÎncă nu există evaluări

- Land Records FraudDocument42 paginiLand Records FraudJeff Wilner88% (8)

- De La Salle University College of Law: Lasallian Commission On Bar Operations 2018Document80 paginiDe La Salle University College of Law: Lasallian Commission On Bar Operations 2018Jazib ZainabÎncă nu există evaluări

- Mortgage FraudDocument42 paginiMortgage FraudJeff Wilner100% (11)

- Tuesday, March 6, 2012: OCC Servicer Review Firm Also "Scrubs" Loan Files, Fabricates DocumentsDocument5 paginiTuesday, March 6, 2012: OCC Servicer Review Firm Also "Scrubs" Loan Files, Fabricates DocumentsJenny Blume SaezÎncă nu există evaluări

- Securities Regulation Spindler Fall2013 KreshoverDocument21 paginiSecurities Regulation Spindler Fall2013 KreshoverBill ColemanÎncă nu există evaluări

- DTC Eligibility Q & ADocument18 paginiDTC Eligibility Q & AjeremyÎncă nu există evaluări

- CHAPTER Auto Saved)Document139 paginiCHAPTER Auto Saved)ynarsaleÎncă nu există evaluări

- Definition: Illegal Insider Trading Is The Trading in A Security (Buying or Selling A Stock) Based OnDocument13 paginiDefinition: Illegal Insider Trading Is The Trading in A Security (Buying or Selling A Stock) Based OnSHAIL911Încă nu există evaluări

- Automating: The Wheels of CommerceDocument20 paginiAutomating: The Wheels of CommerceBhola PrasadÎncă nu există evaluări

- The Foreclosure ReportDocument19 paginiThe Foreclosure ReportAndyJackson100% (3)

- Amortization:: Amortization Is The Process of Decreasing, or Accounting For, An Amount Over ADocument5 paginiAmortization:: Amortization Is The Process of Decreasing, or Accounting For, An Amount Over ASrikanth GuruÎncă nu există evaluări

- Short Answers: 1) Characteristics of Negotiable InstrumentDocument9 paginiShort Answers: 1) Characteristics of Negotiable InstrumentNavyaRaoÎncă nu există evaluări

- CH.2 Buying and Selling SecuritiesDocument47 paginiCH.2 Buying and Selling SecuritiesMahmood KhanÎncă nu există evaluări

- 8 Outsourcing Lessons From IndianaDocument5 pagini8 Outsourcing Lessons From IndianaSANDEEPÎncă nu există evaluări

- Case 1.5 Lincoln Savings and Loan AssociationDocument17 paginiCase 1.5 Lincoln Savings and Loan AssociationAlexa RodriguezÎncă nu există evaluări

- Dokumen - Tips 1 2 3 Do Your Own Securitization Auditin 2016-03-01 A Securitization Audit EvaluatesDocument20 paginiDokumen - Tips 1 2 3 Do Your Own Securitization Auditin 2016-03-01 A Securitization Audit EvaluatesRamon RogersÎncă nu există evaluări

- Collateral Presentation FAI Final2Document31 paginiCollateral Presentation FAI Final2amitsh20072458Încă nu există evaluări

- Busi Law Ch14Document33 paginiBusi Law Ch14Saeed KhanÎncă nu există evaluări

- ETH 321 Final ExamDocument5 paginiETH 321 Final ExamGastonMaignanÎncă nu există evaluări

- Property Law CourseworkDocument7 paginiProperty Law Courseworkbcqneexy100% (2)

- REMIC AND UCC EXPLAINED BY Plus NotesDocument66 paginiREMIC AND UCC EXPLAINED BY Plus Notesfgtrulin100% (9)

- Professional Opportunities For CAsDocument14 paginiProfessional Opportunities For CAsChethan VenkateshÎncă nu există evaluări

- Transcript SEC Fundamentals Part 1Document10 paginiTranscript SEC Fundamentals Part 1archanaanuÎncă nu există evaluări

- Bankruptcy DissertationDocument5 paginiBankruptcy DissertationBuyWritingPaperElgin100% (1)

- Broker Dealers Market Makers and Fiduciary DutiesDocument20 paginiBroker Dealers Market Makers and Fiduciary DutiesghalibÎncă nu există evaluări

- R45 Derivative Markets and InstrumentsDocument24 paginiR45 Derivative Markets and InstrumentsSumair ChughtaiÎncă nu există evaluări

- Statute of Limitations On Debt Collection Sorted by StateDocument5 paginiStatute of Limitations On Debt Collection Sorted by StateWarriorpoetÎncă nu există evaluări

- STC 2012 10k Without ContractsDocument80 paginiSTC 2012 10k Without Contractspeterlee100100% (1)

- Holdback Escrows: Security Against The UnpredictableDocument4 paginiHoldback Escrows: Security Against The UnpredictableSusmita DasÎncă nu există evaluări

- United States Court of Appeals, Tenth CircuitDocument4 paginiUnited States Court of Appeals, Tenth CircuitScribd Government DocsÎncă nu există evaluări

- NEWBRAND - Session 5 Pre-Class AssignmentsDocument4 paginiNEWBRAND - Session 5 Pre-Class AssignmentsimadhamzoÎncă nu există evaluări

- 60 Cds Big BangDocument7 pagini60 Cds Big BangBad PersonÎncă nu există evaluări

- MB0051 Legal Aspects of BusinessDocument11 paginiMB0051 Legal Aspects of BusinessajayvmehtaÎncă nu există evaluări

- Mergers and Acquisitions VII 07.2022Document11 paginiMergers and Acquisitions VII 07.2022K KÎncă nu există evaluări

- Unit 5: Aspect of Contract and Negligence For Business: Kashif AliDocument46 paginiUnit 5: Aspect of Contract and Negligence For Business: Kashif AliKashifÎncă nu există evaluări

- Interview QuestionsDocument2 paginiInterview Questionsvenkatesh286Încă nu există evaluări

- Chicago Interest Rate Swap Legal AnalysisDocument29 paginiChicago Interest Rate Swap Legal AnalysisThe Daily LineÎncă nu există evaluări

- Blaw R 16 Solved FINAL BackupDocument13 paginiBlaw R 16 Solved FINAL BackuptalhaÎncă nu există evaluări

- Business LawDocument7 paginiBusiness LawArchiÎncă nu există evaluări

- Crypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationDe la EverandCrypto Taxation in USA: A Comprehensive Guide to Navigating Digital Assets and TaxationÎncă nu există evaluări

- Frequently Asked Questions in Anti-Bribery and CorruptionDe la EverandFrequently Asked Questions in Anti-Bribery and CorruptionÎncă nu există evaluări

- Primer On Securitization 2019Document36 paginiPrimer On Securitization 2019Anonymous tgYyno0w6Încă nu există evaluări

- Trevor Schuesler - ResumeDocument1 paginăTrevor Schuesler - ResumeDavid HammondÎncă nu există evaluări

- Chap7 PDFDocument61 paginiChap7 PDFAshraf Alawneh100% (1)

- RJR Nabisco ValuationDocument7 paginiRJR Nabisco ValuationAnil Kotaga0% (1)

- Metropolis-Warburg Press Release FinalDocument3 paginiMetropolis-Warburg Press Release FinalvmmalviyaÎncă nu există evaluări

- Ch03 P15 SolutionsDocument16 paginiCh03 P15 SolutionsM E0% (1)

- Chapter 3 - Supply Chain Drivers & MetricsDocument14 paginiChapter 3 - Supply Chain Drivers & MetricsNOSCRIBD100% (1)

- Scopia Capital Presentation On Forest City Realty Trust, Aug. 2016Document19 paginiScopia Capital Presentation On Forest City Realty Trust, Aug. 2016Norman OderÎncă nu există evaluări

- CH 08 - Financial OptionsDocument59 paginiCH 08 - Financial OptionsSyed Mohib HassanÎncă nu există evaluări

- Sample Question CFPDocument15 paginiSample Question CFPapi-3814557100% (7)

- S.E.C. Civil Complaint Against SJK Investment ManagementDocument30 paginiS.E.C. Civil Complaint Against SJK Investment ManagementDealBookÎncă nu există evaluări

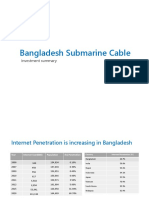

- Bangladesh Submarine Cable (Investment Summary)Document21 paginiBangladesh Submarine Cable (Investment Summary)hossainboxÎncă nu există evaluări

- IFU Coursework 2015 Semester2Document3 paginiIFU Coursework 2015 Semester2DanielÎncă nu există evaluări

- Dividend DecisionsDocument44 paginiDividend DecisionsYogesh JoshiÎncă nu există evaluări

- 162 003Document4 pagini162 003Angelli LamiqueÎncă nu există evaluări

- On January 1 2017 Mcilroy Inc Acquired A 60 PercentDocument1 paginăOn January 1 2017 Mcilroy Inc Acquired A 60 PercentAmit PandeyÎncă nu există evaluări

- Understanding Fortunes FormulaDocument5 paginiUnderstanding Fortunes FormulaTraderCat Solaris0% (2)

- Policy On NISM Series VIIDocument5 paginiPolicy On NISM Series VIIMayank ShahÎncă nu există evaluări

- ACCA F9 - Financia Management - LSBF Class Notes 2011 (Free)Document185 paginiACCA F9 - Financia Management - LSBF Class Notes 2011 (Free)Rahib Jaskani100% (1)

- Books-A-Million Inc: (BAMM)Document1 paginăBooks-A-Million Inc: (BAMM)Old School ValueÎncă nu există evaluări

- Anil Rana ProjectDocument34 paginiAnil Rana Projectanil ranaÎncă nu există evaluări

- Chapter 8Document7 paginiChapter 8Yenelyn Apistar CambarijanÎncă nu există evaluări

- Spring Exam 1 KeyDocument10 paginiSpring Exam 1 KeysufyanjeewaÎncă nu există evaluări

- In Search of The "Buffett Premium" - Free SampleDocument22 paginiIn Search of The "Buffett Premium" - Free SampleRationalWalkÎncă nu există evaluări

- Business Combination Q4Document2 paginiBusiness Combination Q4Sweet EmmeÎncă nu există evaluări

- Alternative InvestmentDocument7 paginiAlternative InvestmentAbhi Jayakumar100% (1)