S-ar putea să vă placă și

- Tactical Portfolios: Strategies and Tactics for Investing in Hedge Funds and Liquid AlternativesDe la EverandTactical Portfolios: Strategies and Tactics for Investing in Hedge Funds and Liquid AlternativesÎncă nu există evaluări

- Artemis Q1 2011 - Is Volatility Broken? Normalcy Bias and Abnormal VarianceDocument10 paginiArtemis Q1 2011 - Is Volatility Broken? Normalcy Bias and Abnormal VarianceRazvan ArionÎncă nu există evaluări

- Artemis - Meeting+of+the+Waters - March2016Document5 paginiArtemis - Meeting+of+the+Waters - March2016jacekÎncă nu există evaluări

- CLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketDe la EverandCLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketÎncă nu există evaluări

- Artemis Capital Q12012 Volatility at Worlds End1Document18 paginiArtemis Capital Q12012 Volatility at Worlds End1Sean GreelyÎncă nu există evaluări

- Inside the Yield Book: The Classic That Created the Science of Bond AnalysisDe la EverandInside the Yield Book: The Classic That Created the Science of Bond AnalysisEvaluare: 3 din 5 stele3/5 (1)

- ACM - The Great Vega ShortDocument10 paginiACM - The Great Vega ShortThorHollisÎncă nu există evaluări

- Electronic Trading Masters: Secrets from the Pros!De la EverandElectronic Trading Masters: Secrets from the Pros!Încă nu există evaluări

- ACM - Vol, Correlation, Unified Risk Theory - 092010Document8 paginiACM - Vol, Correlation, Unified Risk Theory - 092010ThorHollisÎncă nu există evaluări

- Life Settlements and Longevity Structures: Pricing and Risk ManagementDe la EverandLife Settlements and Longevity Structures: Pricing and Risk ManagementÎncă nu există evaluări

- Ambrus Capital - Volatility and The Changing Market Structure Driving U.S. EquitiesDocument18 paginiAmbrus Capital - Volatility and The Changing Market Structure Driving U.S. EquitiespiwipebaÎncă nu există evaluări

- CLO Investing: With an Emphasis on CLO Equity & BB NotesDe la EverandCLO Investing: With an Emphasis on CLO Equity & BB NotesÎncă nu există evaluări

- Art em Is Capital Currency NoteDocument35 paginiArt em Is Capital Currency NoteBen SchwartzÎncă nu există evaluări

- Energy Budgets at Risk (EBaR): A Risk Management Approach to Energy Purchase and Efficiency ChoicesDe la EverandEnergy Budgets at Risk (EBaR): A Risk Management Approach to Energy Purchase and Efficiency ChoicesÎncă nu există evaluări

- Artemis+Research - Dennis+Rodman+and+Portfolio+Optimization - April2016Document7 paginiArtemis+Research - Dennis+Rodman+and+Portfolio+Optimization - April2016jacekÎncă nu există evaluări

- Artemis+Letter+to+Investors What+is+Water July2018 2 PDFDocument11 paginiArtemis+Letter+to+Investors What+is+Water July2018 2 PDFmdorneanuÎncă nu există evaluări

- Easy Volatility Investing AbstractDocument33 paginiEasy Volatility Investing AbstractcttfsdaveÎncă nu există evaluări

- 2020-WB-3458 Cboe Volatility TradeableAssetClassVIXIndexFundamentalsDocument40 pagini2020-WB-3458 Cboe Volatility TradeableAssetClassVIXIndexFundamentalsqwexrdsoheqnxcbxmrÎncă nu există evaluări

- 10 Handy Facts About VolDocument1 pagină10 Handy Facts About VolRahul SheorainÎncă nu există evaluări

- (Columbia University, Derman) Trading Volatility As An Asset ClassDocument37 pagini(Columbia University, Derman) Trading Volatility As An Asset ClassLevi StraussÎncă nu există evaluări

- Artemis - The Great Vega Short - Volatility, Tail Risk, and Sleeping ElephantsDocument10 paginiArtemis - The Great Vega Short - Volatility, Tail Risk, and Sleeping ElephantsRazvan Arion100% (2)

- Volatility Exchange-Traded Notes - Curse or CureDocument25 paginiVolatility Exchange-Traded Notes - Curse or CurelastkraftwagenfahrerÎncă nu există evaluări

- Volatility Radar: Profit From Low Vol and High SkewDocument14 paginiVolatility Radar: Profit From Low Vol and High SkewTze ShaoÎncă nu există evaluări

- FE-Seminar 10 15 2012Document38 paginiFE-Seminar 10 15 2012yerytÎncă nu există evaluări

- VelocityShares Etn Final Pricing Supplement VixlongDocument196 paginiVelocityShares Etn Final Pricing Supplement VixlongtgokoneÎncă nu există evaluări

- (AXA Investment) Why The Implied Correlation of Dispersion Has To Be Higher Than The Correlation Swap StrikeDocument4 pagini(AXA Investment) Why The Implied Correlation of Dispersion Has To Be Higher Than The Correlation Swap StrikeShikhar SharmaÎncă nu există evaluări

- Asia Risk QIS Special Report 2019 PDFDocument16 paginiAsia Risk QIS Special Report 2019 PDFStephane MysonaÎncă nu există evaluări

- The+Incredible+Shrinking+Stock+Market - Dec2015Document8 paginiThe+Incredible+Shrinking+Stock+Market - Dec2015jacekÎncă nu există evaluări

- VIXOptions Strategy Reverse CollarDocument2 paginiVIXOptions Strategy Reverse CollarYvan JestinÎncă nu există evaluări

- Variance Swaps - An IntroductionDocument5 paginiVariance Swaps - An IntroductionAngelo TorresÎncă nu există evaluări

- JPM Fixed inDocument236 paginiJPM Fixed inMikhail ValkoÎncă nu există evaluări

- Dispersion Trading: An Empirical Analysis On The S&P 100 OptionsDocument12 paginiDispersion Trading: An Empirical Analysis On The S&P 100 OptionsTataÎncă nu există evaluări

- Barclays Equity Gilt Study 2011Document144 paginiBarclays Equity Gilt Study 2011parthacfaÎncă nu există evaluări

- Lecture2 PDFDocument16 paginiLecture2 PDFjeanturqÎncă nu există evaluări

- Demystifying Equity Risk-Based StrategiesDocument20 paginiDemystifying Equity Risk-Based Strategiesxy053333Încă nu există evaluări

- Askin CapitalDocument1 paginăAskin CapitalPoorvaÎncă nu există evaluări

- Hans Buehler DissDocument164 paginiHans Buehler DissAgatha MurgociÎncă nu există evaluări

- CBOT-Understanding BasisDocument26 paginiCBOT-Understanding BasisIshan SaneÎncă nu există evaluări

- ACM The Great Vega ShortDocument10 paginiACM The Great Vega ShortwarrenprosserÎncă nu există evaluări

- Towers Watson Tail Risk Management Strategies Oct2015Document14 paginiTowers Watson Tail Risk Management Strategies Oct2015Gennady NeymanÎncă nu există evaluări

- 2014 Volatility Outlook FinalDocument42 pagini2014 Volatility Outlook FinalOmair SiddiqiÎncă nu există evaluări

- Practical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingDocument23 paginiPractical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingArtur SilvaÎncă nu există evaluări

- 2011 Equity Derivatives OutlookDocument70 pagini2011 Equity Derivatives OutlookleetÎncă nu există evaluări

- Structured Products OverviewDocument7 paginiStructured Products OverviewAnkit GoelÎncă nu există evaluări

- Quant Congress - BarCapDocument40 paginiQuant Congress - BarCapperry__mason100% (1)

- 2013 Nov 26 - Conditional Curve Trades e PDFDocument13 pagini2013 Nov 26 - Conditional Curve Trades e PDFkiza66Încă nu există evaluări

- 7 Myths of Structured ProductsDocument18 pagini7 Myths of Structured Productsrohanghalla6052Încă nu există evaluări

- Morgan Stanley 1 Final Portable AlphaDocument12 paginiMorgan Stanley 1 Final Portable AlphadavrobÎncă nu există evaluări

- Introduction & Research: Factor InvestingDocument44 paginiIntroduction & Research: Factor InvestingMohamed HussienÎncă nu există evaluări

- Qis - Insights - Qis Insights Style InvestingDocument21 paginiQis - Insights - Qis Insights Style Investingpderby1Încă nu există evaluări

- Volatility - A New Return Driver PDFDocument16 paginiVolatility - A New Return Driver PDFrlprisÎncă nu există evaluări

- Bloomberg Svi 2013Document57 paginiBloomberg Svi 2013mshchetkÎncă nu există evaluări

- Chris ColeDocument16 paginiChris ColeSultan Fehaid100% (1)

- Trend-Following Primer - January 2021Document8 paginiTrend-Following Primer - January 2021piyush losalkaÎncă nu există evaluări

- VIX SPX AnalysisDocument2 paginiVIX SPX Analysisberrypatch268096Încă nu există evaluări

- Lecture 4 2016 ALMDocument70 paginiLecture 4 2016 ALMEmilioÎncă nu există evaluări

- DynamicVIXFuturesVersion2Rev1 PDFDocument19 paginiDynamicVIXFuturesVersion2Rev1 PDFsamuelcwlsonÎncă nu există evaluări

- Carry TraderDocument62 paginiCarry TraderJuarez CandidoÎncă nu există evaluări

- Butterfly EconomicsDocument5 paginiButterfly EconomicsLameuneÎncă nu există evaluări

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDocument1 paginăA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneÎncă nu există evaluări

- Brief Therapy - A Problem Solving Model of ChangeDocument4 paginiBrief Therapy - A Problem Solving Model of ChangeLameuneÎncă nu există evaluări

- Dispersion TradesDocument41 paginiDispersion TradesLameune100% (1)

- Eyde LandDocument54 paginiEyde LandLameuneÎncă nu există evaluări

- Network of Options For International Coal & Freight BusinessesDocument20 paginiNetwork of Options For International Coal & Freight BusinessesLameuneÎncă nu există evaluări

- Commodity Hybrids Trading: James Groves, Barclays CapitalDocument21 paginiCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneÎncă nu există evaluări

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDocument32 paginiPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneÎncă nu există evaluări

- Andrea RoncoroniDocument27 paginiAndrea RoncoroniLameuneÎncă nu există evaluări

- Tristam ScottDocument24 paginiTristam ScottLameuneÎncă nu există evaluări

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 paginiReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneÎncă nu există evaluări

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDocument25 paginiValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneÎncă nu există evaluări

- Jacob BeharallDocument19 paginiJacob BeharallLameuneÎncă nu există evaluări

- Prmia 20111103 NyholmDocument24 paginiPrmia 20111103 NyholmLameuneÎncă nu există evaluări

- Day3 Session2B StoneDocument11 paginiDay3 Session2B StoneLameuneÎncă nu există evaluări

- Marcel ProkopczukDocument28 paginiMarcel ProkopczukLameuneÎncă nu există evaluări

- Tristam ScottDocument24 paginiTristam ScottLameuneÎncă nu există evaluări

- Day3 Session 2APaulDocument11 paginiDay3 Session 2APaulLameuneÎncă nu există evaluări

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDocument44 paginiReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneÎncă nu există evaluări

- Emmanuel GincbergDocument37 paginiEmmanuel GincbergLameuneÎncă nu există evaluări

- Day3 Session 1BSternberg PresentationforWebDocument11 paginiDay3 Session 1BSternberg PresentationforWebLameuneÎncă nu există evaluări

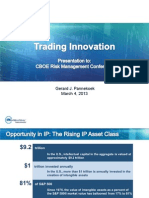

- Gerard J. Pannekoek March 4, 2013Document12 paginiGerard J. Pannekoek March 4, 2013LameuneÎncă nu există evaluări

- Equity Research Report On Mundra Port SEZDocument73 paginiEquity Research Report On Mundra Port SEZRitesh100% (11)

- 1 What Is A Difference Between A Forward Contract and A Future ContractDocument6 pagini1 What Is A Difference Between A Forward Contract and A Future ContractAlok SinghÎncă nu există evaluări

- The Balance Sheet of LifeDocument2 paginiThe Balance Sheet of LifeKashifÎncă nu există evaluări

- Current Account DeficitDocument16 paginiCurrent Account Deficitjainudit212Încă nu există evaluări

- Reporting and Analyzing Intercorporate InvestmentsDocument33 paginiReporting and Analyzing Intercorporate Investmentsoqab18Încă nu există evaluări

- Syllabus of Theory of AccountsDocument4 paginiSyllabus of Theory of AccountsAries SiasonÎncă nu există evaluări

- Sample Essay Writing Topics For SBI PO Mains 2019 - The Bane of NPAs in The Country - 1Document2 paginiSample Essay Writing Topics For SBI PO Mains 2019 - The Bane of NPAs in The Country - 1swarn3675Încă nu există evaluări

- Greatest InvestorsDocument48 paginiGreatest InvestorsIeshita DeyÎncă nu există evaluări

- FIN535 Assignment 4Document8 paginiFIN535 Assignment 4G Ruggy JonesÎncă nu există evaluări

- Merger of HDFC Bank and Centurion Bank of PunjabDocument9 paginiMerger of HDFC Bank and Centurion Bank of PunjabJacob BrewerÎncă nu există evaluări

- Caltex Vs Commission On AuditDocument2 paginiCaltex Vs Commission On AuditHonorio Bartholomew ChanÎncă nu există evaluări

- Al Safi PlatformDocument15 paginiAl Safi PlatformbadrishÎncă nu există evaluări

- Final Exam f02Document13 paginiFinal Exam f02Omar Ahmed ElkhalilÎncă nu există evaluări

- 12 Hitesh MMS A 2018 - 2020 SIP ReportDocument18 pagini12 Hitesh MMS A 2018 - 2020 SIP ReportLalit BaraiÎncă nu există evaluări

- Class 12 Accountancy Solved Sample Paper 1 - 2012Document34 paginiClass 12 Accountancy Solved Sample Paper 1 - 2012cbsestudymaterialsÎncă nu există evaluări

- HDFC Small Cap Fund KIM June 2018Document62 paginiHDFC Small Cap Fund KIM June 2018viadjbvdÎncă nu există evaluări

- Exposure NormsDocument30 paginiExposure Normspadam_09Încă nu există evaluări

- Investment BankingDocument37 paginiInvestment BankingAnkush Kharate67% (3)

- AbcdeDocument5 paginiAbcdeDivyany PandeyÎncă nu există evaluări

- LOREAL Document de Reference 2011Document446 paginiLOREAL Document de Reference 2011Sankeitha SinhaÎncă nu există evaluări

- Videocon - Working CapitalDocument68 paginiVideocon - Working Capitalswati_arora100% (1)

- World05 03 17Document40 paginiWorld05 03 17The WorldÎncă nu există evaluări

- Parmalat Dairy (Bankruptcy)Document26 paginiParmalat Dairy (Bankruptcy)tarunshukla20130% (1)

- 9706 w05 QP 4Document8 pagini9706 w05 QP 4Jean EmanuelÎncă nu există evaluări

- FAC About Loans PDFDocument5 paginiFAC About Loans PDFDenzel BrownÎncă nu există evaluări

- Discussion ProblemsDocument23 paginiDiscussion ProblemsJemÎncă nu există evaluări

- Non Profit GAAPDocument266 paginiNon Profit GAAPshrikantsubsÎncă nu există evaluări

- Project FinanceDocument4 paginiProject FinanceanjuÎncă nu există evaluări

- Chap002 RWJ PrintedDocument46 paginiChap002 RWJ PrintedmohamedÎncă nu există evaluări

- Project Cash Flow Statement Analysis of AXIS BankDocument44 paginiProject Cash Flow Statement Analysis of AXIS BankShubashPoojari100% (1)