S-ar putea să vă placă și

- Global Market Update - 04 09 2015 PDFDocument6 paginiGlobal Market Update - 04 09 2015 PDFRandora LkÎncă nu există evaluări

- ICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCDocument3 paginiICRA Lanka Assigns (SL) BBB-rating With Positive Outlook To Sanasa Development Bank PLCRandora LkÎncă nu există evaluări

- Weekly Foreign Holding & Block Trade Update: Net Buying Net SellingDocument4 paginiWeekly Foreign Holding & Block Trade Update: Net Buying Net SellingRandora LkÎncă nu există evaluări

- 03 September 2015 PDFDocument9 pagini03 September 2015 PDFRandora LkÎncă nu există evaluări

- Press 20150831ebDocument2 paginiPress 20150831ebRandora LkÎncă nu există evaluări

- Daily - 23 04 2015 PDFDocument4 paginiDaily - 23 04 2015 PDFRandora LkÎncă nu există evaluări

- Dividend Hunter - Apr 2015 PDFDocument7 paginiDividend Hunter - Apr 2015 PDFRandora LkÎncă nu există evaluări

- Press Release: Communications DepartmentDocument3 paginiPress Release: Communications DepartmentRandora LkÎncă nu există evaluări

- Janashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFDocument9 paginiJanashakthi Insurance Company PLC - (JINS) - Q4 FY 14 - SELL PDFRandora LkÎncă nu există evaluări

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Document5 paginiN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkÎncă nu există evaluări

- Weekly Foreign Holding & Block Trade Update - 02 04 2015 PDFDocument4 paginiWeekly Foreign Holding & Block Trade Update - 02 04 2015 PDFRandora LkÎncă nu există evaluări

- Wei 20150402 PDFDocument18 paginiWei 20150402 PDFRandora LkÎncă nu există evaluări

- N D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Document5 paginiN D B Securities (PVT) LTD, 5 Floor, # 40, NDB Building, Nawam Mawatha, Colombo 02. Tel: +94 11 2131000 Fax: +9411 2314180Randora LkÎncă nu există evaluări

- Daily Stock Watch: ThursdayDocument9 paginiDaily Stock Watch: ThursdayRandora LkÎncă nu există evaluări

- Press 20150227e PDFDocument1 paginăPress 20150227e PDFRandora LkÎncă nu există evaluări

- CBSL Organizational Structure - (10.02.2015) PDFDocument1 paginăCBSL Organizational Structure - (10.02.2015) PDFRandora LkÎncă nu există evaluări

- Trader's Daily Digest - 12.02.2015 PDFDocument6 paginiTrader's Daily Digest - 12.02.2015 PDFRandora LkÎncă nu există evaluări

- Daily Stock Watch: ThursdayDocument9 paginiDaily Stock Watch: ThursdayRandora LkÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Statement of Axis Account No:923010024537354 For The Period (From: 15-05-2023 To: 16-06-2023)Document2 paginiStatement of Axis Account No:923010024537354 For The Period (From: 15-05-2023 To: 16-06-2023)PRAMOD KUMARÎncă nu există evaluări

- State Bank of India Corporate Centre, MumbaiDocument15 paginiState Bank of India Corporate Centre, MumbaiSHREYAS MAHAPATRAÎncă nu există evaluări

- منافذ الصيرفة الإلكترونية في الجزائر -حالة بنك التنمية المحلية BDLDocument18 paginiمنافذ الصيرفة الإلكترونية في الجزائر -حالة بنك التنمية المحلية BDLRADOUANE ALLOUÎncă nu există evaluări

- Chapter 10: Money and Banking OpenerDocument55 paginiChapter 10: Money and Banking OpenerDwi NurjanahÎncă nu există evaluări

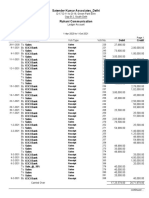

- Satender Kumar Associates - DelhiDocument7 paginiSatender Kumar Associates - DelhiAVS & AssociatesÎncă nu există evaluări

- Class 11 Cbse Business Studies Syllabus 2011-12Document4 paginiClass 11 Cbse Business Studies Syllabus 2011-12Sunaina RawatÎncă nu există evaluări

- Sample Qualified Written Request 2Document5 paginiSample Qualified Written Request 2james j jorissenÎncă nu există evaluări

- Loan EMI CalculatorDocument6 paginiLoan EMI Calculatorjiguparmar1516Încă nu există evaluări

- Indias Leading BFSI Companies 2017Document244 paginiIndias Leading BFSI Companies 2017rohit sharma100% (1)

- SAP Final ProjectDocument10 paginiSAP Final Projecthannan SulemanÎncă nu există evaluări

- Chapter 1 Regulators of Banks and Financial InstitutionsDocument4 paginiChapter 1 Regulators of Banks and Financial InstitutionsAbhijit KonwarÎncă nu există evaluări

- Personal Financing Products PDFDocument10 paginiPersonal Financing Products PDFNurulhikmah RoslanÎncă nu există evaluări

- HDFC ProjectDocument122 paginiHDFC Projectmanbesh50% (2)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument12 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceVARIKUTI RAJASEKHARÎncă nu există evaluări

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceanupsharma2522_98756Încă nu există evaluări

- Chapter - 1 Reserve Bank of India Act, 1934Document13 paginiChapter - 1 Reserve Bank of India Act, 1934arushiÎncă nu există evaluări

- Deposit Product Basic Savings Account-I Savings Account-I Yippie-I Imteen-I Premier Account-I Maybank2u Savers-I Personal Saver-I Flexi Saver-IDocument2 paginiDeposit Product Basic Savings Account-I Savings Account-I Yippie-I Imteen-I Premier Account-I Maybank2u Savers-I Personal Saver-I Flexi Saver-IFakri OthmanÎncă nu există evaluări

- International Financial Management 11 Edition: by Jeff MaduraDocument47 paginiInternational Financial Management 11 Edition: by Jeff MaduraChourp SophalÎncă nu există evaluări

- HSBC London Corporate Refund Undertaking LetterDocument1 paginăHSBC London Corporate Refund Undertaking LetterHelge Sandoy100% (3)

- Monetary Policy: The Economic ProblemDocument23 paginiMonetary Policy: The Economic ProblemDOODGE CHIDHAKWAÎncă nu există evaluări

- Generic ATM Interface User Guide PDFDocument90 paginiGeneric ATM Interface User Guide PDFBIDC Email100% (1)

- Severina P. Velos Receipt PDFDocument5 paginiSeverina P. Velos Receipt PDFJohnry DayupayÎncă nu există evaluări

- STPM MATHEMATICS M Coursework/Kerja Kursus (Semester 1)Document11 paginiSTPM MATHEMATICS M Coursework/Kerja Kursus (Semester 1)jq75% (4)

- Regulatory Framework For Business Transactions: Atty. Kenneth B. Fabila, CPADocument95 paginiRegulatory Framework For Business Transactions: Atty. Kenneth B. Fabila, CPAKris Van HalenÎncă nu există evaluări

- Chapter 5 - Time Value of MoneyDocument7 paginiChapter 5 - Time Value of MoneyParth GargÎncă nu există evaluări

- Environment Scanning of Kotak Mahindra BankDocument17 paginiEnvironment Scanning of Kotak Mahindra Bankmba globalÎncă nu există evaluări

- What Is Imputed Interest?Document3 paginiWhat Is Imputed Interest?1abhishek1Încă nu există evaluări

- Quizzer 2 Pdic SBD Ub Week 14 Set BDocument7 paginiQuizzer 2 Pdic SBD Ub Week 14 Set Bmariesteinsher0Încă nu există evaluări

- Comparative Financial Performance of MBL, KBL, LBL & SBLDocument50 paginiComparative Financial Performance of MBL, KBL, LBL & SBLmahen07100% (2)

- The Bank For International Settlements (BIS)Document1 paginăThe Bank For International Settlements (BIS)Rey DavidÎncă nu există evaluări