S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- HBP FinanceDocument20 paginiHBP FinancePrerna Goel56% (9)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- ACCA F6 - Trading Profit AdjustmentDocument2 paginiACCA F6 - Trading Profit AdjustmentIftekhar Ifte100% (1)

- Coursebook Answers: Business in ContextDocument5 paginiCoursebook Answers: Business in ContextImran AliÎncă nu există evaluări

- Resume Mohd Salim June 2014Document3 paginiResume Mohd Salim June 2014aamirÎncă nu există evaluări

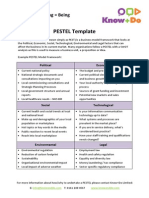

- PESTEL Template: Knowing + Doing BeingDocument2 paginiPESTEL Template: Knowing + Doing Beingaamir100% (1)

- p4 j13 FormulaeDocument5 paginip4 j13 FormulaeaamirÎncă nu există evaluări

- Financial Formulas - Ratios (Sheet)Document3 paginiFinancial Formulas - Ratios (Sheet)carmo-netoÎncă nu există evaluări

- CMA Real Essay QuestionsDocument6 paginiCMA Real Essay Questionsaamir100% (1)

- Tisa Co Is Considering An Opportunity To Produce An Innovative Component WhichDocument2 paginiTisa Co Is Considering An Opportunity To Produce An Innovative Component WhichaamirÎncă nu există evaluări

- Corporate Governance in IndonesiaDocument7 paginiCorporate Governance in IndonesiaElis ShofiyatinÎncă nu există evaluări

- Eng166 RevisionDocument17 paginiEng166 Revisionmangkieuoanh2004Încă nu există evaluări

- Report On IDLCDocument35 paginiReport On IDLCRakib Rahman100% (1)

- KARUNANITHI SRINIVASAN1647319871895-credit-reportDocument26 paginiKARUNANITHI SRINIVASAN1647319871895-credit-reportHaritUchilÎncă nu există evaluări

- Chap 013 Financial Accounting (Statement of Cash Flow)Document39 paginiChap 013 Financial Accounting (Statement of Cash Flow)salman saeed100% (2)

- FN107-1342 - Footnotes Levin-Coburn Report.Document1.037 paginiFN107-1342 - Footnotes Levin-Coburn Report.Rick ThomaÎncă nu există evaluări

- The Failure of EnronDocument2 paginiThe Failure of EnronPrincess GonzalesÎncă nu există evaluări

- AB Memory Based IBPS PO PRE Quantitative Aptitude - 3rd Oct 2020Document24 paginiAB Memory Based IBPS PO PRE Quantitative Aptitude - 3rd Oct 2020shankarinadarÎncă nu există evaluări

- Investment Portfolio Management - 02 - GitmanDocument36 paginiInvestment Portfolio Management - 02 - GitmanNurul Izzah50% (2)

- Loan-Amortization CalculatorDocument14 paginiLoan-Amortization CalculatorVijayakanthÎncă nu există evaluări

- REITSDocument68 paginiREITSsamathagondiÎncă nu există evaluări

- Macro Economics KLE Law College NotesDocument193 paginiMacro Economics KLE Law College Noteslakshmipriyats1532Încă nu există evaluări

- Works of Defence Act 1903 1Document21 paginiWorks of Defence Act 1903 1Eighteenth JulyÎncă nu există evaluări

- Time Value of MoneyDocument8 paginiTime Value of MoneyChethan KumarÎncă nu există evaluări

- TDS Defaults & Procedures Under Traces For Online Correction by Taxguru Consultancy & Online Publication LLPDocument98 paginiTDS Defaults & Procedures Under Traces For Online Correction by Taxguru Consultancy & Online Publication LLPAvantika SharmaÎncă nu există evaluări

- A. Basic Liquidity Ratio 3-6 Month: 1. Based On The Financial Statements, Compute June'sDocument13 paginiA. Basic Liquidity Ratio 3-6 Month: 1. Based On The Financial Statements, Compute June's1 KohÎncă nu există evaluări

- Gepsuct PDFDocument16 paginiGepsuct PDFMario RanceÎncă nu există evaluări

- Refinitiv WebinarDocument16 paginiRefinitiv WebinarOthman SouÎncă nu există evaluări

- Research TitleDocument4 paginiResearch Titlejason repaldaÎncă nu există evaluări

- Intro To Green FinanceDocument8 paginiIntro To Green Financesofttouchd9825Încă nu există evaluări

- Islamic vs. Conventional BankingDocument32 paginiIslamic vs. Conventional BankingNuwan Tharanga LiyanageÎncă nu există evaluări

- Assignment 1711948030Document3 paginiAssignment 1711948030Robin Rahman 1711948030Încă nu există evaluări

- TurkeyDocument3 paginiTurkeyBảo Hiền Nguyễn VõÎncă nu există evaluări

- Republic v. SorianoDocument5 paginiRepublic v. SorianoErika Mariz CunananÎncă nu există evaluări

- Assignment No.9Document5 paginiAssignment No.9rheÎncă nu există evaluări

- Barandino, Abigail T. SET-1 PDFDocument19 paginiBarandino, Abigail T. SET-1 PDFAbigail Talosig BarandinoÎncă nu există evaluări

- GenMath Week 5 6Document24 paginiGenMath Week 5 6Luke JessieMhar LumberioÎncă nu există evaluări