S-ar putea să vă placă și

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Capital Asset Pricing ModelDocument34 paginiCapital Asset Pricing ModelasifanisÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Andrew Cardwell - Using The RSIDocument5 paginiAndrew Cardwell - Using The RSISudarsan P100% (3)

- Guide To Accounting Standards For Private Enterprises Chapter 45 Financial Instruments July 2016Document74 paginiGuide To Accounting Standards For Private Enterprises Chapter 45 Financial Instruments July 2016Shariful HoqueÎncă nu există evaluări

- Theoretical Frame Work 1Document2 paginiTheoretical Frame Work 1Lourd Amethyst OmanaÎncă nu există evaluări

- CompanyAnalysis Club MahindraDocument20 paginiCompanyAnalysis Club MahindrapavandomalÎncă nu există evaluări

- CompanyAnalysis Club MahindraDocument20 paginiCompanyAnalysis Club MahindrapavandomalÎncă nu există evaluări

- ENTREPRENEURSHIPDocument46 paginiENTREPRENEURSHIPMontebon CrislynÎncă nu există evaluări

- Barter System History - The Past and PresentDocument13 paginiBarter System History - The Past and PresentJohn TurnerÎncă nu există evaluări

- Java SwingDocument21 paginiJava SwingpavandomalÎncă nu există evaluări

- Java ContainersDocument3 paginiJava ContainerspavandomalÎncă nu există evaluări

- University of Mumbai MFM III Entrepreneurship MGT QuestionsDocument3 paginiUniversity of Mumbai MFM III Entrepreneurship MGT QuestionspavandomalÎncă nu există evaluări

- Mumbai University MFM - III Paper Questions Strategic ManagementDocument4 paginiMumbai University MFM - III Paper Questions Strategic ManagementpavandomalÎncă nu există evaluări

- Entrepreneurship ManagementDocument10 paginiEntrepreneurship ManagementpavandomalÎncă nu există evaluări

- DCF ModellDocument7 paginiDCF ModellVishal BhanushaliÎncă nu există evaluări

- Purchase ManagementDocument19 paginiPurchase ManagementUmair SaeedÎncă nu există evaluări

- HDB Resale Transactions - Jan 09Document4 paginiHDB Resale Transactions - Jan 09pinkcoralÎncă nu există evaluări

- BF Reviewer Q2 Module (1-2,4-5)Document3 paginiBF Reviewer Q2 Module (1-2,4-5)Catherine SalasÎncă nu există evaluări

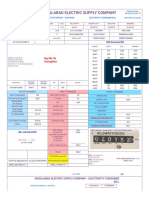

- Fesco Online BillDocument2 paginiFesco Online BillSaqLain AliÎncă nu există evaluări

- Case Study Omena HotelDocument4 paginiCase Study Omena HotelKrystal Yee100% (1)

- TAX Invoice: Scheme Discount DetailsDocument36 paginiTAX Invoice: Scheme Discount DetailsSadaf RazzaqueÎncă nu există evaluări

- Resumen Precios Diarios B.M.L. Cobre Grado "A": DAY Spot FUTURE (3) (2) Spot FUTUREDocument1 paginăResumen Precios Diarios B.M.L. Cobre Grado "A": DAY Spot FUTURE (3) (2) Spot FUTUREMaria Ellen AcevedoÎncă nu există evaluări

- KajalDocument10 paginiKajalKajal RawatÎncă nu există evaluări

- DSEpp - Competition and Market StructureDocument4 paginiDSEpp - Competition and Market Structurepeter wongÎncă nu există evaluări

- Draft Invoice - Zuba CafeDocument1 paginăDraft Invoice - Zuba Cafechandanprakash30Încă nu există evaluări

- Cost Volume Profit AnalysisDocument22 paginiCost Volume Profit Analysisd14764Încă nu există evaluări

- Payment Options: Online Banking - Highly RecommendedDocument1 paginăPayment Options: Online Banking - Highly RecommendedMEET SHAHÎncă nu există evaluări

- BIBM Academic 2011Document113 paginiBIBM Academic 2011PaulÎncă nu există evaluări

- English 3 Answer Key PDFDocument26 paginiEnglish 3 Answer Key PDFThu Nguyệt PhạmÎncă nu există evaluări

- The Ask Method PhenomenonDocument11 paginiThe Ask Method PhenomenonRickie AmánÎncă nu există evaluări

- Submitted To: Shailee Parmar: Nikita Punera Student Id:Iuu19Bba061Document15 paginiSubmitted To: Shailee Parmar: Nikita Punera Student Id:Iuu19Bba061nikitaÎncă nu există evaluări

- Strategic MGTDocument23 paginiStrategic MGTAhdel GirlisonfireÎncă nu există evaluări

- Companies: Foundation OperatorDocument3 paginiCompanies: Foundation OperatorJesu JesuÎncă nu există evaluări

- Getting Started With Edgerater: Chris White Founder and Ceo, Edgerater LLC December 2013Document26 paginiGetting Started With Edgerater: Chris White Founder and Ceo, Edgerater LLC December 2013satyaseelanÎncă nu există evaluări

- Financial Management Presentation Part I - Summer Class 2017Document44 paginiFinancial Management Presentation Part I - Summer Class 2017Juan Sebastian Leyton ZabaletaÎncă nu există evaluări

- Any Questions From Last Class?Document15 paginiAny Questions From Last Class?chdx21479Încă nu există evaluări

- Business Plan-Food Truck - Bhavya, Neha B, PoojaDocument13 paginiBusiness Plan-Food Truck - Bhavya, Neha B, PoojaAshutosh SharmaÎncă nu există evaluări

- CASE STUDY - Titan Industries LTD PDFDocument2 paginiCASE STUDY - Titan Industries LTD PDFSaurabh SethÎncă nu există evaluări