S-ar putea să vă placă și

- Risk Navigation Strategies for Major Capital Projects: Beyond the Myth of PredictabilityDe la EverandRisk Navigation Strategies for Major Capital Projects: Beyond the Myth of PredictabilityÎncă nu există evaluări

- The Outsourcing Revolution (Review and Analysis of Corbett's Book)De la EverandThe Outsourcing Revolution (Review and Analysis of Corbett's Book)Încă nu există evaluări

- Putting Together The Pieces: The 2013 Guide To S&OP Technology SelectionDocument39 paginiPutting Together The Pieces: The 2013 Guide To S&OP Technology SelectionhedajareÎncă nu există evaluări

- 01 GenPact OverviewDocument9 pagini01 GenPact Overviewamitbharadwaj7Încă nu există evaluări

- 633676496954865000Document23 pagini633676496954865000shaheencmÎncă nu există evaluări

- Finance Department - CFODocument16 paginiFinance Department - CFOvarachartered283100% (1)

- Balanced Scorecard Usage Survey 2013: Summary of FindingsDocument10 paginiBalanced Scorecard Usage Survey 2013: Summary of FindingsanferrufoÎncă nu există evaluări

- TL Bulletin - Oil Gas Operating Mode TrendsDocument5 paginiTL Bulletin - Oil Gas Operating Mode TrendscaviarÎncă nu există evaluări

- Article-Us Consulting Mo Manufacturing Strategy and Operations 111910Document2 paginiArticle-Us Consulting Mo Manufacturing Strategy and Operations 111910sanits591Încă nu există evaluări

- Wipro Annual Report 2011-12Document244 paginiWipro Annual Report 2011-12rah98Încă nu există evaluări

- Wipro Annual Report 2011 12Document244 paginiWipro Annual Report 2011 12Hariharasudan HariÎncă nu există evaluări

- How Organizations Approach and Adapt Their Technology Strategy For GRCDocument83 paginiHow Organizations Approach and Adapt Their Technology Strategy For GRCShanmugavelSankaranÎncă nu există evaluări

- Product Lifecycle Management Research PapersDocument7 paginiProduct Lifecycle Management Research Papersb0siw1h1tab2100% (1)

- 1 - End To End Process Management Implications For Theory and PracticeDocument20 pagini1 - End To End Process Management Implications For Theory and PracticeRoberta BrandaoÎncă nu există evaluări

- Blue Wolf State of Outsourcing 2013Document15 paginiBlue Wolf State of Outsourcing 2013angelgmv9492Încă nu există evaluări

- Thesis KpiDocument6 paginiThesis Kpidnqj27m0100% (2)

- Embracing Cloud KPMGDocument52 paginiEmbracing Cloud KPMGcertman4uÎncă nu există evaluări

- TCS BpoDocument14 paginiTCS Bpoaruncool2009Încă nu există evaluări

- Summary Report: Vertical Industry Strategies For Shared Services and Outsourcing SurveyDocument52 paginiSummary Report: Vertical Industry Strategies For Shared Services and Outsourcing SurveyRahulÎncă nu există evaluări

- 2013 Enterprise Cloud Adoption SurveyDocument0 pagini2013 Enterprise Cloud Adoption SurveyConstanza Carcamo AsemÎncă nu există evaluări

- Opex 2019 The Drive Towards Operational Excellence in Oil and Gas Oil and Gas iqRNIFb0AhUSeZzZ1Z9WwJIZAWN3fSM6XmxOQCtOiG PDFDocument10 paginiOpex 2019 The Drive Towards Operational Excellence in Oil and Gas Oil and Gas iqRNIFb0AhUSeZzZ1Z9WwJIZAWN3fSM6XmxOQCtOiG PDFnaveenÎncă nu există evaluări

- CorporatePpt Q2 2014Document9 paginiCorporatePpt Q2 2014Ankit BhatnagarÎncă nu există evaluări

- Operational Efficiency & Process Improvement in It Industry: Business Research ProjectDocument3 paginiOperational Efficiency & Process Improvement in It Industry: Business Research Projectjith4uÎncă nu există evaluări

- Roland Berger Corporate Headquarters Short Version 20130502 PDFDocument27 paginiRoland Berger Corporate Headquarters Short Version 20130502 PDFEdin GlibićÎncă nu există evaluări

- Strategic Outsourcing Increasing Shareholder Value Through Transformational OutsourcingDocument42 paginiStrategic Outsourcing Increasing Shareholder Value Through Transformational OutsourcingKoventhan RaviÎncă nu există evaluări

- Master Track GDMDocument10 paginiMaster Track GDMSridhar IyerÎncă nu există evaluări

- Dells Supply Chain JourneyDocument17 paginiDells Supply Chain JourneyRADHA120Încă nu există evaluări

- PWC - SCM - NEXT GENDocument19 paginiPWC - SCM - NEXT GENPartha Patim GiriÎncă nu există evaluări

- WhitePaper BenchmarkStudy 2013Document19 paginiWhitePaper BenchmarkStudy 2013ExactCPAÎncă nu există evaluări

- PWC Global Supply Chain Survey 2013Document19 paginiPWC Global Supply Chain Survey 2013mushtaque61Încă nu există evaluări

- Accenture IIFT DeckDocument11 paginiAccenture IIFT DeckviveknadimintiÎncă nu există evaluări

- Extending The Lean Enterprise: February 2008Document21 paginiExtending The Lean Enterprise: February 2008Tiotet33Încă nu există evaluări

- Six Sigma PHD ThesisDocument5 paginiSix Sigma PHD Thesiscarolelmonte100% (2)

- Sourcing Contingent Workforce - Rise of MSP Model - Service Provider LandscapeDocument11 paginiSourcing Contingent Workforce - Rise of MSP Model - Service Provider LandscapeeverestgrpÎncă nu există evaluări

- BPC Tricks, TipsDocument134 paginiBPC Tricks, TipsTrivikram As100% (5)

- 2 PDFDocument13 pagini2 PDFRegine Erika LaydiaÎncă nu există evaluări

- 6733 F Insights Wipro REPORTDocument28 pagini6733 F Insights Wipro REPORTmanishjangid9869Încă nu există evaluări

- A SWOT Analysis On Six SigmaDocument10 paginiA SWOT Analysis On Six SigmasmuÎncă nu există evaluări

- Timesaver FromDocument115 paginiTimesaver FromSundar Seetharam100% (1)

- Northgate AR13 WebDocument50 paginiNorthgate AR13 WebJohn HenryÎncă nu există evaluări

- KPMG Blackline BrochureDocument2 paginiKPMG Blackline Brochurean2204Încă nu există evaluări

- Llamasoft Gartner Issue1 PDFDocument22 paginiLlamasoft Gartner Issue1 PDFDarshan HDÎncă nu există evaluări

- Energy Saving With Six SigmaDocument12 paginiEnergy Saving With Six SigmadcyleeÎncă nu există evaluări

- BPO Whitepaper Business Process Transformation 0512-1Document8 paginiBPO Whitepaper Business Process Transformation 0512-1Ganesh BabuÎncă nu există evaluări

- WiproDocument16 paginiWiproImraan KhanÎncă nu există evaluări

- Global OutsourcingDocument39 paginiGlobal OutsourcingKaran GuptaÎncă nu există evaluări

- Research Paper On Outsourcing ServicesDocument4 paginiResearch Paper On Outsourcing Servicespuzolunyzyg2100% (1)

- A Framework To Speed Manufacturing's Digital Business TransformationDocument17 paginiA Framework To Speed Manufacturing's Digital Business TransformationCognizant100% (1)

- Bhupesh Negi (OM Articles)Document6 paginiBhupesh Negi (OM Articles)Bhupesh NegiÎncă nu există evaluări

- Global Delivery ModelDocument14 paginiGlobal Delivery ModelAnika VarkeyÎncă nu există evaluări

- Sixsigma PDFDocument5 paginiSixsigma PDFdeliciousfood96Încă nu există evaluări

- Driving Global Adoption of Procurement Technology, A Cargill ApproachDocument27 paginiDriving Global Adoption of Procurement Technology, A Cargill ApproachZycusInc100% (2)

- RoI in DCIMDocument28 paginiRoI in DCIMJulioCesarÎncă nu există evaluări

- Lean Manufacturing Research Paper PDFDocument5 paginiLean Manufacturing Research Paper PDFafmcuvkjz100% (1)

- How Do Enterprise Mobility Strategy Makers Choose Their Suppliers in 2012?Document1 paginăHow Do Enterprise Mobility Strategy Makers Choose Their Suppliers in 2012?api-167982264Încă nu există evaluări

- Operations Management in Automotive Industries: From Industrial Strategies to Production Resources Management, Through the Industrialization Process and Supply Chain to Pursue Value CreationDe la EverandOperations Management in Automotive Industries: From Industrial Strategies to Production Resources Management, Through the Industrialization Process and Supply Chain to Pursue Value CreationÎncă nu există evaluări

- Guide to Supply Chain Management: An End to End PerspectiveDe la EverandGuide to Supply Chain Management: An End to End PerspectiveÎncă nu există evaluări

- Project Control Methods and Best Practices: Achieving Project SuccessDe la EverandProject Control Methods and Best Practices: Achieving Project SuccessÎncă nu există evaluări

- Straight from the Client: Consulting Experiences and Observed TrendsDe la EverandStraight from the Client: Consulting Experiences and Observed TrendsÎncă nu există evaluări

- A Study of the Supply Chain and Financial Parameters of a Small BusinessDe la EverandA Study of the Supply Chain and Financial Parameters of a Small BusinessÎncă nu există evaluări

- 10 Capital StructureDocument5 pagini10 Capital StructureshenjicodoÎncă nu există evaluări

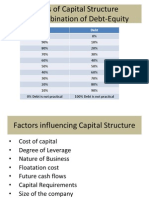

- Forms of Capital Structure Combination of Debt-EquityDocument4 paginiForms of Capital Structure Combination of Debt-EquityshenjicodoÎncă nu există evaluări

- 9 Capital Budgeting - Traditional ToolsDocument27 pagini9 Capital Budgeting - Traditional ToolsshenjicodoÎncă nu există evaluări

- Office 365Document1 paginăOffice 365shenjicodo67% (3)

- Singapore+Malysia ItineraryDocument2 paginiSingapore+Malysia ItineraryshenjicodoÎncă nu există evaluări

- AccentureDocument46 paginiAccenturekapil_nandu9322Încă nu există evaluări

- PoolVac CaseDocument4 paginiPoolVac Caseshenjicodo0% (2)

- Wipro Annual Report 2013 14Document236 paginiWipro Annual Report 2013 14Sudhanshu TyagiÎncă nu există evaluări

- IXP20 Poster A12010Document1 paginăIXP20 Poster A12010mycornerstoneÎncă nu există evaluări

- Googleearth Xy Coordinate InstructionsDocument2 paginiGoogleearth Xy Coordinate Instructionsapi-245872444Încă nu există evaluări

- IT&BusinessDocument26 paginiIT&BusinessshenjicodoÎncă nu există evaluări

- BM006-3-2 Creativity and Innovation (VC1) 1 April 2018 OBEDocument2 paginiBM006-3-2 Creativity and Innovation (VC1) 1 April 2018 OBEDiana RoseÎncă nu există evaluări

- Activity 2 PacketDocument16 paginiActivity 2 PacketFrancez Anne GuanzonÎncă nu există evaluări

- 2023 GEC MMW SyllabusDocument9 pagini2023 GEC MMW Syllabusdanbejagan20Încă nu există evaluări

- MoD DGQA Initiatives Towards EODBDocument59 paginiMoD DGQA Initiatives Towards EODBSanjay Kumar DashÎncă nu există evaluări

- Towards A New Project Management' Movement? An International Development PerspectiveDocument12 paginiTowards A New Project Management' Movement? An International Development PerspectiveMiguel diazÎncă nu există evaluări

- Globalisation and Its Effects On The WorkplaceDocument11 paginiGlobalisation and Its Effects On The WorkplaceTimothyYeoÎncă nu există evaluări

- (AMA) MED EDU Innovation ChallangeDocument46 pagini(AMA) MED EDU Innovation ChallangerezautamaÎncă nu există evaluări

- The Framework of Contemporary BusinessDocument19 paginiThe Framework of Contemporary BusinessLivingstone CaesarÎncă nu există evaluări

- Nano-Tera 2016 State of The ArtDocument71 paginiNano-Tera 2016 State of The ArtnanoteraCHÎncă nu există evaluări

- Case Study Week 01Document3 paginiCase Study Week 01Steven WijayaÎncă nu există evaluări

- Essential Business Skills and Their Application in The Business WorldDocument3 paginiEssential Business Skills and Their Application in The Business Worldaran valeroÎncă nu există evaluări

- InterserveDocument3 paginiInterserveAla Eldin YassenÎncă nu există evaluări

- Systems of Innovation Theory and Policy For The Demand SideDocument17 paginiSystems of Innovation Theory and Policy For The Demand Sideapi-3851548Încă nu există evaluări

- Student Research Group: - Towards Students Research Capacity andDocument13 paginiStudent Research Group: - Towards Students Research Capacity andCyizere EricÎncă nu există evaluări

- Bgu Placement BrochureDocument42 paginiBgu Placement BrochureIgit Sarang Placement CellÎncă nu există evaluări

- Apple Inc. Organizational ChangeDocument7 paginiApple Inc. Organizational Changejavaid IqbalÎncă nu există evaluări

- Underarmour Case AnalysisDocument31 paginiUnderarmour Case AnalysisArsyadNurulHakim100% (1)

- Aspects of The Research RoadmapDocument40 paginiAspects of The Research Roadmapmario_fernando_acosta9760Încă nu există evaluări

- E Types-Strategy ImplementationDocument3 paginiE Types-Strategy ImplementationSravan Sridhar100% (1)

- Sem-2 MBA Strategic Management All PPTs PDFDocument220 paginiSem-2 MBA Strategic Management All PPTs PDFDixit NellithayÎncă nu există evaluări

- Benefits of Value EngineeringDocument13 paginiBenefits of Value EngineeringrubydelacruzÎncă nu există evaluări

- Managing Digital Innovation A Knowledge Perspectiv... - (1 The Changing Context of Work Implications For Knowledge and Innovati... )Document20 paginiManaging Digital Innovation A Knowledge Perspectiv... - (1 The Changing Context of Work Implications For Knowledge and Innovati... )Joseph Justeen LavarinthanÎncă nu există evaluări

- Solution Manual For Strategic Management of Technological Innovation 6th Edition Melissa SchillingDocument37 paginiSolution Manual For Strategic Management of Technological Innovation 6th Edition Melissa Schillingbowerybismarea2blrr100% (12)

- Report - ResilDocument46 paginiReport - ResilNamrata NagarajÎncă nu există evaluări

- Chandu SvitDocument85 paginiChandu SvitkhayyumÎncă nu există evaluări

- Pricing Model at A BPODocument17 paginiPricing Model at A BPORyan Scott100% (2)

- Master of Business Administration - MBA Semester 2 MB0044-Production & Operations ManagementDocument47 paginiMaster of Business Administration - MBA Semester 2 MB0044-Production & Operations ManagementASR07Încă nu există evaluări

- Journal of Administrative Management, Education and Training (JAMET)Document15 paginiJournal of Administrative Management, Education and Training (JAMET)ThuraMinSweÎncă nu există evaluări

- Feasibility About Aloe Vera OilDocument61 paginiFeasibility About Aloe Vera Oilgabbacvillacorta100% (2)

- 20200205-National CI Strategy 2020 2022Document20 pagini20200205-National CI Strategy 2020 2022Matt Thomas100% (1)