S-ar putea să vă placă și

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionDe la EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionÎncă nu există evaluări

- Accounting-2009 Resit ExamDocument18 paginiAccounting-2009 Resit ExammasterURÎncă nu există evaluări

- Commercial & Industrial Equipment Repair & Maintenance Revenues World Summary: Market Values & Financials by CountryDe la EverandCommercial & Industrial Equipment Repair & Maintenance Revenues World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- Model Answers Series 2 2010Document17 paginiModel Answers Series 2 2010Jack Tsang100% (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionDe la EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionÎncă nu există evaluări

- 2010 LCCI Bookkeeping and Accounts Series 3Document8 pagini2010 LCCI Bookkeeping and Accounts Series 3Fung Hui Ying75% (4)

- Technical & Trade School Revenues World Summary: Market Values & Financials by CountryDe la EverandTechnical & Trade School Revenues World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- AC100 Exam 2012Document17 paginiAC100 Exam 2012Ruby TangÎncă nu există evaluări

- Int1 Accounting All 2014Document32 paginiInt1 Accounting All 2014Illharm SherrifÎncă nu există evaluări

- Economic Indicators for Eastern Asia: Input–Output TablesDe la EverandEconomic Indicators for Eastern Asia: Input–Output TablesÎncă nu există evaluări

- Code 2007 Accounting Level 2 2010 Series 4Document15 paginiCode 2007 Accounting Level 2 2010 Series 4apple_syih100% (1)

- Compendium of Supply and Use Tables for Selected Economies in Asia and the PacificDe la EverandCompendium of Supply and Use Tables for Selected Economies in Asia and the PacificÎncă nu există evaluări

- 6002 Source Booklet January 2011Document12 pagini6002 Source Booklet January 2011Sausan AliÎncă nu există evaluări

- Automotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryDe la EverandAutomotive Glass Replacement Shop Revenues World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- ABE Dip 1 - Financial Accounting JUNE 2005Document19 paginiABE Dip 1 - Financial Accounting JUNE 2005spinster40% (1)

- Cosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryDe la EverandCosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- AccountingDocument8 paginiAccountingHaniyaAngelÎncă nu există evaluări

- Outboard Motorboats World Summary: Market Sector Values & Financials by CountryDe la EverandOutboard Motorboats World Summary: Market Sector Values & Financials by CountryÎncă nu există evaluări

- Financial Accounting: Formation 2 Examination - April 2008Document11 paginiFinancial Accounting: Formation 2 Examination - April 2008Luke ShawÎncă nu există evaluări

- Wheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryDe la EverandWheels & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- Wef2012 Pilot MAFDocument9 paginiWef2012 Pilot MAFdileepank14Încă nu există evaluări

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionDe la EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionÎncă nu există evaluări

- Management Control SystemDocument11 paginiManagement Control SystemomkarsawantÎncă nu există evaluări

- AssigmentDocument8 paginiAssigmentnonolashari0% (1)

- Book Keeping and Accounts Past Paper Series 2 2011Document6 paginiBook Keeping and Accounts Past Paper Series 2 2011Aggelos Ispirli0% (1)

- 2009-Management Accounting Main EQP and CommentariesDocument53 pagini2009-Management Accounting Main EQP and CommentariesBryan Sing100% (1)

- 97 ZaDocument7 pagini97 ZaMeow Meow HuiÎncă nu există evaluări

- 2010 LCCI Level 3 Series 2 Question Paper (Code 3012)Document8 pagini2010 LCCI Level 3 Series 2 Question Paper (Code 3012)mappymappymappyÎncă nu există evaluări

- Ms 4Document2 paginiMs 4Dickie SangmaÎncă nu există evaluări

- Higher Level Paper 2 2010Document8 paginiHigher Level Paper 2 2010Mark MoloneyÎncă nu există evaluări

- P1 - Corporate Reporting August 10Document18 paginiP1 - Corporate Reporting August 10IrfanÎncă nu există evaluări

- Accounting A2 Jan 2005Document11 paginiAccounting A2 Jan 2005Orbind B. ShaikatÎncă nu există evaluări

- CPA IRELAND Accounting Framework April 07Document14 paginiCPA IRELAND Accounting Framework April 07Luke ShawÎncă nu există evaluări

- Lcci Level3 Solution Past Paper Series 3-10Document14 paginiLcci Level3 Solution Past Paper Series 3-10tracyduckk67% (3)

- 2010-Principles of Accounting Main EQP and Commentaries 2010-Principles of Accounting Main EQP and CommentariesDocument59 pagini2010-Principles of Accounting Main EQP and Commentaries 2010-Principles of Accounting Main EQP and Commentaries전민건Încă nu există evaluări

- Financial Accounting Fundamentals May 2011Document6 paginiFinancial Accounting Fundamentals May 2011Kofi EwoenamÎncă nu există evaluări

- Technician Pilot Papers PDFDocument133 paginiTechnician Pilot Papers PDFCasius Mubamba100% (4)

- Management Accounting 12Document4 paginiManagement Accounting 12subba1995333333Încă nu există evaluări

- Section 1Document3 paginiSection 1Ketan PatelÎncă nu există evaluări

- 6002 (1) - AccountingDocument16 pagini6002 (1) - AccountingDaphne RenÎncă nu există evaluări

- Principles of AccountingDocument6 paginiPrinciples of AccountingGian Karlo PagariganÎncă nu există evaluări

- Final Economy 2010 SolutionDocument6 paginiFinal Economy 2010 SolutionValadez28Încă nu există evaluări

- Accounting/Series 2 2007 (Code3001)Document16 paginiAccounting/Series 2 2007 (Code3001)Hein Linn Kyaw100% (3)

- AccountingDocument4 paginiAccountingNaiya JoshiÎncă nu există evaluări

- ACC4182010 BDocument10 paginiACC4182010 Bashra16605Încă nu există evaluări

- Lcci 3012Document21 paginiLcci 3012alee200Încă nu există evaluări

- Solution Past Paper Higher-Series4-08hkDocument16 paginiSolution Past Paper Higher-Series4-08hkJoyce LimÎncă nu există evaluări

- DU B.com (H) First Year (Financial Acc.) - Q Paper 2010Document7 paginiDU B.com (H) First Year (Financial Acc.) - Q Paper 2010mouryastudypointÎncă nu există evaluări

- Cash Flow StatementDocument5 paginiCash Flow StatementSai Phanindra Kumar MuddamÎncă nu există evaluări

- Financial Accounting December 2009 Exam PaperDocument10 paginiFinancial Accounting December 2009 Exam Paperkarlr9Încă nu există evaluări

- ABC L3 Past Paper Series 3 2013Document7 paginiABC L3 Past Paper Series 3 2013b3nzyÎncă nu există evaluări

- F7uk 2010 Jun QDocument9 paginiF7uk 2010 Jun QKathleen HenryÎncă nu există evaluări

- 2009-Financial Reporting Main EQP and CommentariesDocument46 pagini2009-Financial Reporting Main EQP and CommentariesBryan SingÎncă nu există evaluări

- Test Papers: FoundationDocument23 paginiTest Papers: FoundationUmesh TurankarÎncă nu există evaluări

- Question Paper1 2005 AccountsDocument12 paginiQuestion Paper1 2005 Accountspankhaniahirensv150Încă nu există evaluări

- D15 Hybrid F5 QPDocument7 paginiD15 Hybrid F5 QPadad9988Încă nu există evaluări

- Assignment 3 - QuestionDocument4 paginiAssignment 3 - QuestionkennethselaeloÎncă nu există evaluări

- Management Accounting Assignment Question I & IIDocument3 paginiManagement Accounting Assignment Question I & IIAbdul LathifÎncă nu există evaluări

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument8 paginiUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelSherjeel AhmedÎncă nu există evaluări

- Ac1025 Excza 11Document18 paginiAc1025 Excza 11gurpreet_mÎncă nu există evaluări

- Edexcel A-LEVEL BIO5 June 2005 QPDocument24 paginiEdexcel A-LEVEL BIO5 June 2005 QPapi-3726022100% (1)

- Predictor Coef SE Coef Test StatisticDocument2 paginiPredictor Coef SE Coef Test Statisticgurpreet_mÎncă nu există evaluări

- Biology Edexcel Unit 5 SN June 2008Document12 paginiBiology Edexcel Unit 5 SN June 2008Nav NÎncă nu există evaluări

- Revision Guide For Statistics GCSEDocument89 paginiRevision Guide For Statistics GCSESanah KhanÎncă nu există evaluări

- As Chemistry AnswersDocument10 paginiAs Chemistry Answersrajbegum62Încă nu există evaluări

- 3 Working Capital and Current Assets ManagementDocument8 pagini3 Working Capital and Current Assets ManagementJamaica DavidÎncă nu există evaluări

- Modul AKLII-2 - Investor Acc MethodDocument31 paginiModul AKLII-2 - Investor Acc MethodLisa SilviÎncă nu există evaluări

- 05 ALCAR ApproachDocument25 pagini05 ALCAR ApproachVaidyanathan Ravichandran100% (2)

- Peter Goa - English Exercise Unit 4Document14 paginiPeter Goa - English Exercise Unit 4Ronaldo Stevent SitohangÎncă nu există evaluări

- Final Exam f02Document13 paginiFinal Exam f02Omar Ahmed ElkhalilÎncă nu există evaluări

- Funds FlowDocument5 paginiFunds FlowSubha KalyanÎncă nu există evaluări

- Accounting For DepreciationDocument16 paginiAccounting For DepreciationKrishna100% (2)

- Forex Gains and Losses Notes 2020Document46 paginiForex Gains and Losses Notes 2020chelasimunyolaÎncă nu există evaluări

- Valuation of Goodwilles - (Problems - SolutionDocument39 paginiValuation of Goodwilles - (Problems - SolutionJazz Raj50% (2)

- Finmar Chapter 7 Group 4 Bsacc 2 2 RevisedDocument17 paginiFinmar Chapter 7 Group 4 Bsacc 2 2 RevisedApril Joyce OaperinaÎncă nu există evaluări

- Australian Hospital Patient Costing Standards - Version 4.0 - Part 2 - Business RulesDocument76 paginiAustralian Hospital Patient Costing Standards - Version 4.0 - Part 2 - Business RulesHonors GroupÎncă nu există evaluări

- Ey Good Company Fta India PDFDocument164 paginiEy Good Company Fta India PDFyasinÎncă nu există evaluări

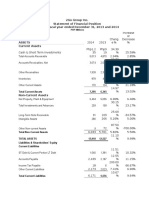

- 2go Group IncDocument7 pagini2go Group IncSheenah FerolinoÎncă nu există evaluări

- ACC Chapter 8 QuestionsDocument12 paginiACC Chapter 8 Questionsmasud.mily06Încă nu există evaluări

- FABM 2 Financial AnalysisDocument67 paginiFABM 2 Financial Analysismary rose aragonÎncă nu există evaluări

- Accounting:Text and Cases 2-1 & 2-3Document3 paginiAccounting:Text and Cases 2-1 & 2-3Mon Louie Ferrer100% (5)

- CFS Company Has The Following Details For Two-Year Period, 2019 and 2018Document7 paginiCFS Company Has The Following Details For Two-Year Period, 2019 and 2018MiconÎncă nu există evaluări

- Partnership Changes: 1 Compiled by T T Herbert (0773 038 651 / 0712 560 772)Document4 paginiPartnership Changes: 1 Compiled by T T Herbert (0773 038 651 / 0712 560 772)Tawanda Tatenda HerbertÎncă nu există evaluări

- Module No 4 - Capital Gains TaxDocument8 paginiModule No 4 - Capital Gains TaxBetty SantiagoÎncă nu există evaluări

- PERMATA ILTIZAM SDN BHD-SME ScoreDocument8 paginiPERMATA ILTIZAM SDN BHD-SME ScoreFazlisha ShaharizanÎncă nu există evaluări

- Accounting Yellow BookDocument466 paginiAccounting Yellow BookTshireletso100% (2)

- Property Plant Tutorials Number OneDocument46 paginiProperty Plant Tutorials Number OneNatalie SerranoÎncă nu există evaluări

- Bumi Serpong Damai TBK.: Company Report: January 2019 As of 31 January 2019Document3 paginiBumi Serpong Damai TBK.: Company Report: January 2019 As of 31 January 2019NurulÎncă nu există evaluări

- Saim MCQDocument9 paginiSaim MCQAmanVatsÎncă nu există evaluări

- Palmerstown Company Established A Subsidiary in A Foreign Country OnDocument1 paginăPalmerstown Company Established A Subsidiary in A Foreign Country OnFreelance WorkerÎncă nu există evaluări

- Tugas 5 - InventoryDocument11 paginiTugas 5 - InventoryMuhammad RochimÎncă nu există evaluări

- (Financial Accounting and Auditing Collection) Bettner, Mark S - 2015 PDFDocument152 pagini(Financial Accounting and Auditing Collection) Bettner, Mark S - 2015 PDFJorge Ysrael Velez Murillo50% (2)

- Finance FunctionDocument25 paginiFinance FunctionKane0% (1)

- Limitations of Ratio AnalysisDocument2 paginiLimitations of Ratio AnalysisJahanzeb Hussain QureshiÎncă nu există evaluări

- Lory'S Dried Fish Store: Business Plan ProposalDocument17 paginiLory'S Dried Fish Store: Business Plan ProposalAnn Kempher Viernes NovalÎncă nu există evaluări

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDe la EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsEvaluare: 5 din 5 stele5/5 (1)

- Getting to Yes: How to Negotiate Agreement Without Giving InDe la EverandGetting to Yes: How to Negotiate Agreement Without Giving InEvaluare: 4 din 5 stele4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De la EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Evaluare: 4.5 din 5 stele4.5/5 (13)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe la EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindEvaluare: 5 din 5 stele5/5 (231)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe la EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItEvaluare: 5 din 5 stele5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDe la EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineÎncă nu există evaluări

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)De la EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Evaluare: 4 din 5 stele4/5 (33)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!De la EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Evaluare: 4.5 din 5 stele4.5/5 (14)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDe la EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyEvaluare: 5 din 5 stele5/5 (1)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)De la EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDe la EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsEvaluare: 4 din 5 stele4/5 (7)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyDe la EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyEvaluare: 4.5 din 5 stele4.5/5 (37)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDe la EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsÎncă nu există evaluări

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe la EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesÎncă nu există evaluări

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditDe la EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditEvaluare: 5 din 5 stele5/5 (1)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDe la EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetÎncă nu există evaluări

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessDe la EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessEvaluare: 4.5 din 5 stele4.5/5 (28)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageDe la EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageEvaluare: 4.5 din 5 stele4.5/5 (109)

- Controllership: The Work of the Managerial AccountantDe la EverandControllership: The Work of the Managerial AccountantÎncă nu există evaluări

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)De la EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Evaluare: 4.5 din 5 stele4.5/5 (24)

- Financial Accounting For Dummies: 2nd EditionDe la EverandFinancial Accounting For Dummies: 2nd EditionEvaluare: 5 din 5 stele5/5 (10)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookDe la EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookEvaluare: 5 din 5 stele5/5 (4)