S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- CambuzaDocument45 paginiCambuzaMia Marin Pâslaru100% (2)

- Moody DiagramDocument18 paginiMoody DiagramWilson JustinoÎncă nu există evaluări

- On-Farm Composting Methods 2003 BOOKDocument51 paginiOn-Farm Composting Methods 2003 BOOKlalibÎncă nu există evaluări

- Stainless Steel: Presented By, Dr. Pragati Jain 1 YearDocument68 paginiStainless Steel: Presented By, Dr. Pragati Jain 1 YearSneha JoshiÎncă nu există evaluări

- Suzuki B-King Indicator Mod CompleteDocument9 paginiSuzuki B-King Indicator Mod Completehookuspookus1Încă nu există evaluări

- Technical Owner Manual Nfinity v6Document116 paginiTechnical Owner Manual Nfinity v6Tom MondjollianÎncă nu există evaluări

- GFF (T) ... MenglischNANNI (DMG-39 25.11.05) PDFDocument38 paginiGFF (T) ... MenglischNANNI (DMG-39 25.11.05) PDFjuricic2100% (2)

- SECTION 1213, 1214, 1215: Report By: Elibado T. MaureenDocument19 paginiSECTION 1213, 1214, 1215: Report By: Elibado T. MaureenJohnFred CativoÎncă nu există evaluări

- Excel 2016: Large Data 1 : Sorting and FilteringDocument19 paginiExcel 2016: Large Data 1 : Sorting and FilteringSapna JoshiÎncă nu există evaluări

- Wri Method FigDocument15 paginiWri Method Figsoumyadeep19478425Încă nu există evaluări

- To Dmaic or Not To DmaicDocument1 paginăTo Dmaic or Not To Dmaicritch99Încă nu există evaluări

- Quality Risk ManagementDocument29 paginiQuality Risk ManagementmmmmmÎncă nu există evaluări

- Surveying Civil Engineering Pictorial Booklet 15 English MediumDocument125 paginiSurveying Civil Engineering Pictorial Booklet 15 English MediumtnstcnpalanisamyÎncă nu există evaluări

- Construction of Rajive Gandhi Urja Bhawan, Ongc Energy Center & Corporate OfficeDocument23 paginiConstruction of Rajive Gandhi Urja Bhawan, Ongc Energy Center & Corporate OfficeDevendra SharmaÎncă nu există evaluări

- Final App - FlsDocument9 paginiFinal App - Flsjunebug172100% (1)

- 5 6176700143207711706Document198 pagini5 6176700143207711706abc defÎncă nu există evaluări

- Programmable Safety Systems PSS-Range: Service Tool PSS SW QLD, From Version 4.2 Operating Manual Item No. 19 461Document18 paginiProgrammable Safety Systems PSS-Range: Service Tool PSS SW QLD, From Version 4.2 Operating Manual Item No. 19 461MAICK_ITSÎncă nu există evaluări

- REE Copy PDFDocument9 paginiREE Copy PDFJake ZozobradoÎncă nu există evaluări

- Error Number Mentor GraphicsDocument30 paginiError Number Mentor GraphicsMendesÎncă nu există evaluări

- Wireshark Protocol Help Product PreviewDocument6 paginiWireshark Protocol Help Product Previewsunil1978Încă nu există evaluări

- FINAL ITP 2024 CompressedDocument388 paginiFINAL ITP 2024 Compressedhamidjumat77Încă nu există evaluări

- Omron ManualDocument44 paginiOmron ManualHaroDavidÎncă nu există evaluări

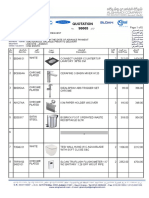

- Quotation 98665Document5 paginiQuotation 98665Reda IsmailÎncă nu există evaluări

- Bell Desk-2Document96 paginiBell Desk-2Arrow PrasadÎncă nu există evaluări

- Review of C++ Programming: Sheng-Fang HuangDocument49 paginiReview of C++ Programming: Sheng-Fang HuangIfat NixÎncă nu există evaluări

- MCB 12V-8A MCB 24V-5A Battery ChargerDocument2 paginiMCB 12V-8A MCB 24V-5A Battery ChargerJosé Wilton AlvesÎncă nu există evaluări

- Adequate Bearing Material and Heat TreatmentDocument20 paginiAdequate Bearing Material and Heat TreatmentdavideÎncă nu există evaluări

- Lifting Plan For CranesDocument9 paginiLifting Plan For CranesBibin JohnÎncă nu există evaluări

- 96 Tacoma SpecsDocument10 pagini96 Tacoma SpecsFerran AlfonsoÎncă nu există evaluări

- Data Structure Algorithm Using C PresentationDocument245 paginiData Structure Algorithm Using C PresentationdhruvwÎncă nu există evaluări