S-ar putea să vă placă și

- List of Profitable Business Ideas in Electrical and Electronics Products Manufacturing Industries and Power Projects.-51597 PDFDocument78 paginiList of Profitable Business Ideas in Electrical and Electronics Products Manufacturing Industries and Power Projects.-51597 PDFrajavinugmailcomÎncă nu există evaluări

- Cable Operating SystemDocument21 paginiCable Operating SystemBarry AllenÎncă nu există evaluări

- Semiconductor Industry in India - Future of Semiconductor Industry in IndiaDocument10 paginiSemiconductor Industry in India - Future of Semiconductor Industry in IndiaThe United IndianÎncă nu există evaluări

- Cable IndustryDocument41 paginiCable IndustryRishav Jain100% (1)

- NASSCOM Talent Supply and Demand AnalysisDocument90 paginiNASSCOM Talent Supply and Demand AnalysisAmitÎncă nu există evaluări

- NASSCOM Talent Supply and Demand AnalysisDocument90 paginiNASSCOM Talent Supply and Demand AnalysisAmitÎncă nu există evaluări

- RAN Market Tracker 1Q23Document20 paginiRAN Market Tracker 1Q23Hoang LongÎncă nu există evaluări

- Liberalisation and Industrial PolicyDocument22 paginiLiberalisation and Industrial PolicyShivam GuptaÎncă nu există evaluări

- Indus TowersDocument10 paginiIndus TowersHitesh Himanshu0% (1)

- The NGN Carrier Ethernet SystemDocument52 paginiThe NGN Carrier Ethernet SystemjuharieÎncă nu există evaluări

- Instrumental Methods of Analysis Part1Document34 paginiInstrumental Methods of Analysis Part1nofacejackÎncă nu există evaluări

- RituDocument21 paginiRituDevendra KumarÎncă nu există evaluări

- Sps0660en Red BinsDocument4 paginiSps0660en Red Binspatima_sv4875Încă nu există evaluări

- Kuesioner Core Self Evaluation ScalesDocument2 paginiKuesioner Core Self Evaluation ScalesBandar Wira PutraÎncă nu există evaluări

- Rise and Fall of Nokia (2014)Document14 paginiRise and Fall of Nokia (2014)Amit71% (7)

- Indian Telco + Tower CompaniesDocument4 paginiIndian Telco + Tower CompaniesHimal VaghelaÎncă nu există evaluări

- India Warehousing Report - Knight Frank PDFDocument59 paginiIndia Warehousing Report - Knight Frank PDFdeepakmukhiÎncă nu există evaluări

- Rural Sector in IndiaDocument33 paginiRural Sector in Indiarajat_singlaÎncă nu există evaluări

- Indo China PPT 25Document42 paginiIndo China PPT 25khubhiÎncă nu există evaluări

- Cable TV MGMT SystemDocument10 paginiCable TV MGMT SystemManoj Kumar100% (1)

- Zee News Project ReportDocument8 paginiZee News Project ReportSanjukta Das RoyÎncă nu există evaluări

- List of Narendra Modi SchemesDocument22 paginiList of Narendra Modi SchemesnrscÎncă nu există evaluări

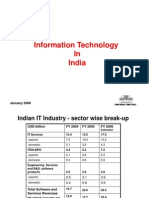

- Information Technology in India: January 2006Document18 paginiInformation Technology in India: January 2006richdev009_106456088100% (1)

- Strategic Analysis of The Indian It Industry With Focus On Its Big Three FirmsDocument31 paginiStrategic Analysis of The Indian It Industry With Focus On Its Big Three Firmsneha mundraÎncă nu există evaluări

- Solar DocsDocument268 paginiSolar DocsSumit MishraÎncă nu există evaluări

- Telangana Data Centres PolicyDocument28 paginiTelangana Data Centres PolicyNaveen Lawrence100% (1)

- Industry AnalysisDocument9 paginiIndustry AnalysisNitesh Kr SinghÎncă nu există evaluări

- Indian Processed Foods Industry and The Ready To Eat MarketDocument64 paginiIndian Processed Foods Industry and The Ready To Eat MarketKartik MuppirisettyÎncă nu există evaluări

- Buddhist Circuit Tourism Strategy FinalDocument72 paginiBuddhist Circuit Tourism Strategy Finalwph referenceÎncă nu există evaluări

- India Warehousing and Logistics Report 2326Document80 paginiIndia Warehousing and Logistics Report 2326Surendra SwamiÎncă nu există evaluări

- Project Report For Supermarket - Sharda AssociatesDocument4 paginiProject Report For Supermarket - Sharda AssociatesChidanand TerdalÎncă nu există evaluări

- Yes Bank Approaches To AgribusinessDocument22 paginiYes Bank Approaches To AgribusinessMAJU70Încă nu există evaluări

- FMCG Report July 2018Document32 paginiFMCG Report July 2018Anshuman UpadhyayÎncă nu există evaluări

- Part 1Document576 paginiPart 1ManivannanÎncă nu există evaluări

- Rack Pruebas HitachiDocument4 paginiRack Pruebas HitachijesusÎncă nu există evaluări

- Milk Dairy Management System: Submitted ToDocument29 paginiMilk Dairy Management System: Submitted ToDipali KantaleÎncă nu există evaluări

- Team PowerBank WP8000 EDM enDocument4 paginiTeam PowerBank WP8000 EDM enSofiane ChenÎncă nu există evaluări

- Accelerating Innovation With Indian EngineeringDocument12 paginiAccelerating Innovation With Indian Engineeringrahulkanwar267856Încă nu există evaluări

- TV Set-Top Box ReportDocument10 paginiTV Set-Top Box ReportneelofarÎncă nu există evaluări

- Electronics Systems Design and Manufacturing Eco System: Manufacturing Eco System: Next Big Leap in IndiaDocument17 paginiElectronics Systems Design and Manufacturing Eco System: Manufacturing Eco System: Next Big Leap in Indiaghatakp2069Încă nu există evaluări

- Idea Cellular StrategyDocument34 paginiIdea Cellular Strategysdrkmau50% (2)

- Big Data and Its Impact On Power SectorDocument23 paginiBig Data and Its Impact On Power SectorJoel Pothen JojiÎncă nu există evaluări

- KSFC ProjectDocument26 paginiKSFC ProjectsrinÎncă nu există evaluări

- Finecab Information DocumentDocument37 paginiFinecab Information DocumentAnirudhÎncă nu există evaluări

- Ms High Tensile Nuts and BoltsDocument11 paginiMs High Tensile Nuts and Boltsmax_ashi100% (1)

- Final ReportDocument28 paginiFinal ReportBishwo Kiran Bhattarai100% (1)

- NABARD Dairy Farming Project - PDF - Agriculture - Loans PDFDocument7 paginiNABARD Dairy Farming Project - PDF - Agriculture - Loans PDFshiba prasad panjaÎncă nu există evaluări

- "Recharge" The First Indonesia Power Bank Rental AppDocument3 pagini"Recharge" The First Indonesia Power Bank Rental Appgak jadiÎncă nu există evaluări

- Global Datacenter Locations Talent NeuronDocument15 paginiGlobal Datacenter Locations Talent NeuronTalent NeuronÎncă nu există evaluări

- Industry Analysis of ItDocument6 paginiIndustry Analysis of ItDurgesh KumarÎncă nu există evaluări

- Broadcasting & Network AutomationDocument34 paginiBroadcasting & Network AutomationShrish JoshiÎncă nu există evaluări

- Amar Complete REPORTDocument66 paginiAmar Complete REPORTsection iÎncă nu există evaluări

- SeminarDocument7 paginiSeminarTolera Tamiru100% (1)

- Module 1Document14 paginiModule 1Nathan Shankar100% (1)

- Cma Indian Bank Format LatestDocument38 paginiCma Indian Bank Format Latestsanket1892Încă nu există evaluări

- Cold Chain Industry in India A ReportDocument5 paginiCold Chain Industry in India A ReportANKUSHSINGH2690Încă nu există evaluări

- Request For Proposal NSDC StarDocument30 paginiRequest For Proposal NSDC StarakumaraoÎncă nu există evaluări

- Precision Turned Products World Summary: Market Values & Financials by CountryDe la EverandPrecision Turned Products World Summary: Market Values & Financials by CountryÎncă nu există evaluări

- Working Paper 398Document57 paginiWorking Paper 398madhav shankarÎncă nu există evaluări

- OECD IoT Measurement ApplicationsDocument67 paginiOECD IoT Measurement ApplicationsNitaÎncă nu există evaluări

- Study Paper AI and Big Data For TelecomDocument17 paginiStudy Paper AI and Big Data For TelecomchufamoashenafiÎncă nu există evaluări

- India Build and InteriorsDocument36 paginiIndia Build and Interiorsdevendra_abcdÎncă nu există evaluări

- Iso/Iec JTC 1: Internet of ThingsDocument17 paginiIso/Iec JTC 1: Internet of ThingsChristen CastilloÎncă nu există evaluări

- ESG ISSA Research Report Life of Cybersecurity Professionals Jul 2021Document39 paginiESG ISSA Research Report Life of Cybersecurity Professionals Jul 2021Elena VaciagoÎncă nu există evaluări

- Engman Ciricular-Labour MigrationDocument67 paginiEngman Ciricular-Labour MigrationGaurav AgrawalÎncă nu există evaluări

- IT Sector Final Report and Stock PitchDocument31 paginiIT Sector Final Report and Stock PitchJosh Bloom100% (1)

- Internet Aspiring Executive Summary v2Document32 paginiInternet Aspiring Executive Summary v2AmitÎncă nu există evaluări

- Cruical ConversationsDocument1 paginăCruical ConversationsAmitÎncă nu există evaluări

- CIBC ReportDocument4 paginiCIBC ReportAmitÎncă nu există evaluări

- Economy CanadaDocument16 paginiEconomy CanadaAmitÎncă nu există evaluări

- IMF Staff Report CanadaDocument70 paginiIMF Staff Report CanadaAmitÎncă nu există evaluări

- Economy CanadaDocument16 paginiEconomy CanadaAmitÎncă nu există evaluări

- 8 Minute MeditationDocument188 pagini8 Minute Meditationanon_475797984100% (2)

- WMP 2010 13 BrochureDocument2 paginiWMP 2010 13 BrochureAmitÎncă nu există evaluări

- KaprekarDocument4 paginiKaprekarAmitÎncă nu există evaluări

- 50 Green Eggs and Ham - Dr. Seuss PDFDocument33 pagini50 Green Eggs and Ham - Dr. Seuss PDFAfonso André Rocha100% (3)

- This Content Downloaded From 36.81.137.101 On Tue, 22 Dec 2020 06:45:10 UTCDocument13 paginiThis Content Downloaded From 36.81.137.101 On Tue, 22 Dec 2020 06:45:10 UTCGrasiawainÎncă nu există evaluări

- Surveying 1 Laboratory Elementary and Higher Surveying: Reciprocal LevelingDocument5 paginiSurveying 1 Laboratory Elementary and Higher Surveying: Reciprocal LevelingCarlo Miguel MagalitÎncă nu există evaluări

- Identification of OOTDocument6 paginiIdentification of OOTHans LeupoldÎncă nu există evaluări

- Revitalization and Synthesis of Factors Associated With The Purchase of Local Fast Moving Consumer Goods The Zambian PerspectiveDocument7 paginiRevitalization and Synthesis of Factors Associated With The Purchase of Local Fast Moving Consumer Goods The Zambian PerspectiveInternational Journal of Innovative Science and Research TechnologyÎncă nu există evaluări

- Mitesd 934s10 Lec 14bDocument17 paginiMitesd 934s10 Lec 14bSoumya DasÎncă nu există evaluări

- Vol 1704 3Document11 paginiVol 1704 3Zara RamisÎncă nu există evaluări

- Csir Net Exam 2024Document3 paginiCsir Net Exam 2024as1655647Încă nu există evaluări

- Management Information System: - by Group IDocument15 paginiManagement Information System: - by Group Iashwinishanbhag1987Încă nu există evaluări

- Summer Project Report: Gujarat Technological UniversityDocument8 paginiSummer Project Report: Gujarat Technological UniversityRahulpaghdalÎncă nu există evaluări

- Doxxing: A Scoping Review and TypologyDocument22 paginiDoxxing: A Scoping Review and TypologyholdencÎncă nu există evaluări

- UGTechOnline Proposal - 15.04.21Document8 paginiUGTechOnline Proposal - 15.04.21DxmplesÎncă nu există evaluări

- HHS Public Access: Association of Cervical Effacement With The Rate of Cervical Change in Labor Among Nulliparous WomenDocument12 paginiHHS Public Access: Association of Cervical Effacement With The Rate of Cervical Change in Labor Among Nulliparous WomenM Iqbal EffendiÎncă nu există evaluări

- Of Social Sciences SSU1013: BasicsDocument38 paginiOf Social Sciences SSU1013: Basicstahmid nafyÎncă nu există evaluări

- Entrepreneurial Characteristics and Business PerformanceDocument76 paginiEntrepreneurial Characteristics and Business PerformanceKyaw Moe HeinÎncă nu există evaluări

- 7 - WH QuestionsDocument4 pagini7 - WH QuestionsNhi PhamÎncă nu există evaluări

- Research1 - Module 2 - EleccionDocument8 paginiResearch1 - Module 2 - EleccionEcho Siason EleccionÎncă nu există evaluări

- Is Planning Theory Really Open For Planning PracticeDocument6 paginiIs Planning Theory Really Open For Planning PracticeLu PoÎncă nu există evaluări

- Problem IdentificationDocument14 paginiProblem IdentificationSyedÎncă nu există evaluări

- Literature Review On Public Procurement ProcessDocument6 paginiLiterature Review On Public Procurement Processc5qz47sm100% (1)

- Cannibalism & Gang Involvement in The Cinematic Lives of Asian Gangsters (Int. Journal of Criminology & Sociology, 2012)Document15 paginiCannibalism & Gang Involvement in The Cinematic Lives of Asian Gangsters (Int. Journal of Criminology & Sociology, 2012)ruediediÎncă nu există evaluări

- Applications of Lexical Cohesion PDFDocument276 paginiApplications of Lexical Cohesion PDFSajadAbdaliÎncă nu există evaluări

- Kenworth MotorDocument2 paginiKenworth MotorRizky WinandaÎncă nu există evaluări

- Characteristics, Strengths, Weaknesses, Kinds ofDocument15 paginiCharacteristics, Strengths, Weaknesses, Kinds ofAljon Domingo TabuadaÎncă nu există evaluări

- Evaluation of Automated Web Testing ToolsDocument4 paginiEvaluation of Automated Web Testing ToolsATSÎncă nu există evaluări

- Research PDFDocument20 paginiResearch PDFZayn MendesÎncă nu există evaluări

- GIS-based Landslide Hazard Assessment - An OverviewDocument21 paginiGIS-based Landslide Hazard Assessment - An OverviewIchsan Ridwan0% (1)

- EDT - Math Lesson Plan (Time)Document3 paginiEDT - Math Lesson Plan (Time)KristaÎncă nu există evaluări